Water-Soluble Fertilizers Market: Addressing Global Food Security Challenges

Other |

2026-05-08 07:57:30

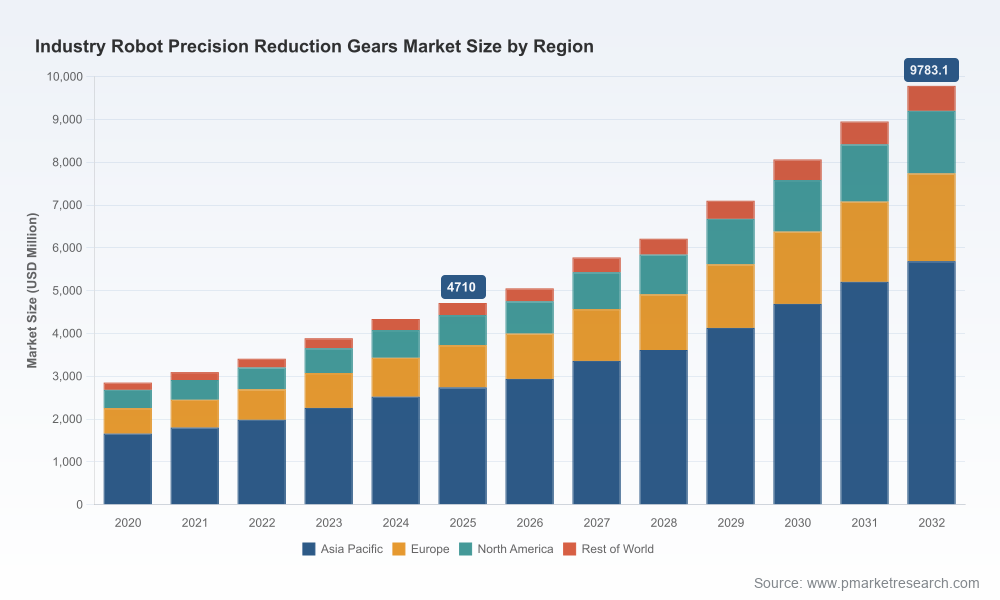

PW Consulting’s latest market study on the Worldwide Industry Robot Precision Reduction Gears market (base year 2025; forecast period 2026–2032) synthesizes macro trajectory, supply-chain stress points, technology roadmaps, competitive moves, and actionable scenarios that matter for boardrooms and operating teams in 2026. The market has moved from a modest post‑2019 recovery into a sustained expansion phase: total industry revenues rose from roughly USD 2.85 billion in 2020 to about USD 4.71 billion in 2025 and are projected to nearly double over the forecast window to reach approximately USD 9.78 billion by 2032, reflecting a compound annual growth rate of around 11.0%.

Worldwide Industry Robot Precision Reduction Gears Market

This preview article highlights the strategic value of the full report for executives who must prioritize investments, sourcing strategies, product planning, and M&A activity in 2026. It demonstrates the depth of our analysis while intentionally omitting granular subsegment tables and region/application breakdowns—those revenue-by-segment details and modeled permutations are available in the full report.

Worldwide Industry Robot Precision Reduction Gears Market

Robotics is shifting from isolated automation islands toward pervasive, precision-dependent tasks across automotive, electronics, consumer goods, and emerging humanoid applications. Reduction gears (cycloidal, strain wave/harmonic, planetary and hybrid forms) are central to joint-level performance—torque density, zero/backlash behavior, rigidity and lifetime drive robot accuracy and total cost of ownership.

Worldwide Industry Robot Precision Reduction Gears Market

Industry 4.0 adoption and higher-speed, high-mix manufacturing intensify demand for compact, high‑efficiency gearheads integrated with sensors and mechatronics. These technical requirements translate into premium pricing and distinct supplier advantages that the market is beginning to capture.

On the supply side, raw material and equipment shifts (notably alloy steel pricing and advanced hobbing/cutting machinery) are changing cost structures and domestic manufacturing economics—critical inputs to sourcing and localization decisions in 2026.

The full PW Consulting report is structured for immediate operational use. Key deliverables include:

Top‑down and bottom‑up market sizing and forecast models (2020–2032) with scenario layers for slower/faster recovery, component commoditization, and technology substitution.

Value‑chain maps and a granular cost build for typical precision reducer production (materials, processing, labor, testing, and aftermarket), with sensitivity analyses tied to alloy steel and energy price paths.

Technology roadmaps and product taxonomy, including performance benchmarks for cycloidal, harmonic (strain wave), planetary and hybrid reducer families and their most relevant engineering trade-offs.

Commercial playbooks: go‑to‑market segmentation, aftermarket strategies, pricing elasticity tests, and bundled service offers (mechatronic modules, lubricants, predictive maintenance contracts).

Risk register and mitigation playbooks addressing supply disruption, intellectual property hotspots, tariff and localization pressures, and transition plans for OEMs and tier suppliers.

Deal pipeline and M&A screening matrices keyed to capability, regional footprint, and margin accretion potential for 10+ target archetypes.

The industry is materially consolidated. A small set of incumbent suppliers account for the dominant share of high‑torque, high‑rigidity applications, while a broader second tier competes vigorously on price, local service, and niche form factors. For decision-makers this means:

Pricing power is concentrated at the technology leaders; new entrants must either innovate at the component level or compete on speed-to-localization and aftermarket responsiveness.

Strategic partnerships, licensing, or distribution agreements are often more effective and less capital‑intensive than attempting a full‑scale production greenfield in the short term.

PW Consulting’s industry mapping tracks established leaders and high‑velocity challengers. Highlights:

Nabtesco remains the benchmark for high‑torque cycloidal reductions in larger industrial robots, with a strong emphasis on rigidity, low backlash and integrated mechatronics. Recent actions point to a pivot that combines product refinement with sustainability and service expansion—an intentional move to protect margins while enabling OEMs to meet lifecycle and environmental goals (notably a portfolio refresh and renewed emphasis on specialized lubricants and mechatronic systems announced in early 2026).

Harmonic Drive (global network spanning the US, Europe and Japan) continues to define the precision end of the market through strain wave technology—compact form factors with exceptionally low backlash. Their product positioning favors high-precision, compact joint actuation where size and positional fidelity are premium attributes.

Sumitomo (Sumitomo Drive Technologies) and other cycloidal specialists continue to optimize for high-speed, long-life applications, combining manufacturing know‑how with reliability claims that are attractive to high‑duty cycle OEMs.

European precision houses (e.g., SPINEA, Neugart, WITTENSTEIN) emphasize engineering proximity, rapid customization and short lead‑times for delta and parallel kinematic robots, positioning themselves as preferred suppliers to regional OEMs and high-mix manufacturers.

Tier challengers and Asian scale players (including specialist harmonic and actuator manufacturers) are expanding capacity and IP portfolios to close the performance gap while leveraging scale advantages—an evolution that keeps competitive pressure on pricing and product bundling.

Nabtesco’s 2026 portfolio overhaul emphasizes mechatronics and sustainability initiatives, signaling a strategic shift to lock in long‑term OEM relationships through services and system integration offers.

Nabtesco’s SPS 2025 product introductions included a new short‑form gearbox leveraging strain‑wave technologies to raise power density in compact packages—an example of incumbents hybridizing platforms.

Nidec’s equipment investments (new hobbing machine launches in mid‑2025) illustrate how suppliers are automating gear production to reduce labor intensity and improve consistency—an enabler for reshoring and capacity scaling.

Two inputs will influence supplier economics into 2026 and beyond:

Alloy steel—critical for gears that must withstand high stresses—remains a sizeable global commodity. Our report connects alloy steel market projections to gearbox cost models, showing how modest shifts in steel pricing propagate through margins and sourcing decisions. Planning for multi‑sourcing and longer hedging horizons for steel is prudent.

Global steel prices entered 2026 at a low point in the current cycle and, in our assessment, are unlikely to rebound aggressively that year due to structural overcapacity and demand dynamics. That creates a narrow window for buyers to lock favorable input costs—but also raises questions about longer‑term supply reliability.

Sourcing and supplier rationalization: Run a two‑track sourcing strategy—secure capacity with tier‑one incumbents for critical, validated reducer platforms while qualifying high‑volume Asian suppliers for commoditized subassemblies and actuation modules to optimize cost and lead time.

Product roadmaps and modularization: Prioritize modular gearbox families that enable platform commonality across robot classes; this reduces SKU proliferation, accelerates validation cycles, and increases aftermarket revenue potential.

Factory and equipment investment sequencing: Evaluate investments in advanced gearmaking equipment (e.g., multi‑operation hobbing lines) versus contract manufacturing. PW Consulting’s capex scenario module quantifies payback windows under varying volume ramps.

Aftermarket and services: Develop predictive maintenance and lubricant service bundles to extend lifetime revenue and improve OEM margins—the economics of service scale are compelling given precision gear lifecycle characteristics.

M&A and partnerships: Pursue capability-focused acquisitions (sensor integration, localized finishing, mechatronic controllers) rather than volume buys. Strategic partnerships with regional engineering houses can deliver immediate market access without full production investment.

The full PW Consulting report is designed as a decision support toolkit for 2026 planning cycles:

Boards: Use the risk register, concentration analysis and M&A screening for capital allocation and strategic scenario planning.

Supply‑chain leaders: Use the cost‑build and raw‑material sensitivity models to set procurement policy, inventory targets, and hedging strategies.

Product and R&D heads: Use the technology roadmaps and benchmark matrices to prioritize development investments and IP protection steps.

Commercial teams: Use the go‑to‑market playbooks and pricing elasticity tests to refine OEM contracts, service offers and channel strategies.

This article is a strategic trailer—designed to foreground the decision‑critical themes and to demonstrate the analytical framing that PW Consulting applies. The full report contains the detailed segment tables, proprietary forecast scenarios, granular supplier scorecards and executable playbooks that operational teams need to implement the priorities above. For teams planning budgets, capex, or M&A activity in 2026, that level of granularity will be essential.

Contact PW Consulting to obtain the full Worldwide Industry Robot Precision Reduction Gears Market report, access model licenses, or commission a tailored advisory session to translate findings into a 2026 action plan.

For detailed analysis of this topic, please visit the official page:Worldwide Industry Robot Precision Reduction Gears Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com