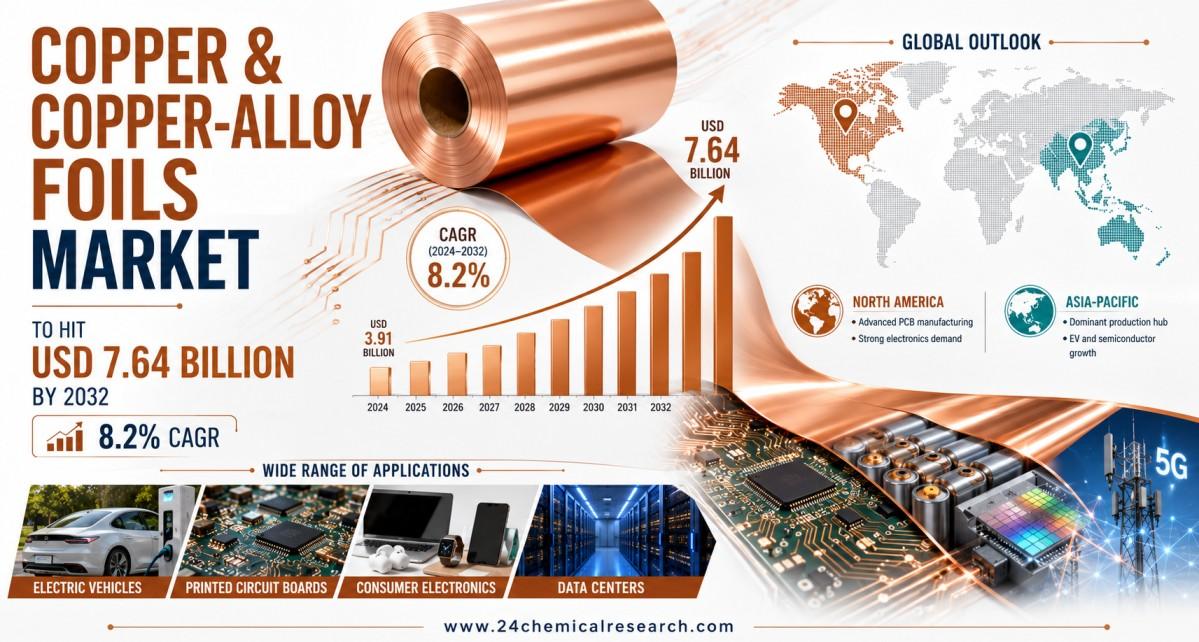

Copper & Copper-Alloy Foils Market to Hit USD 7.64 Billion by 2032 at 8.2% CAGR

Other |

2026-06-17 14:20:30

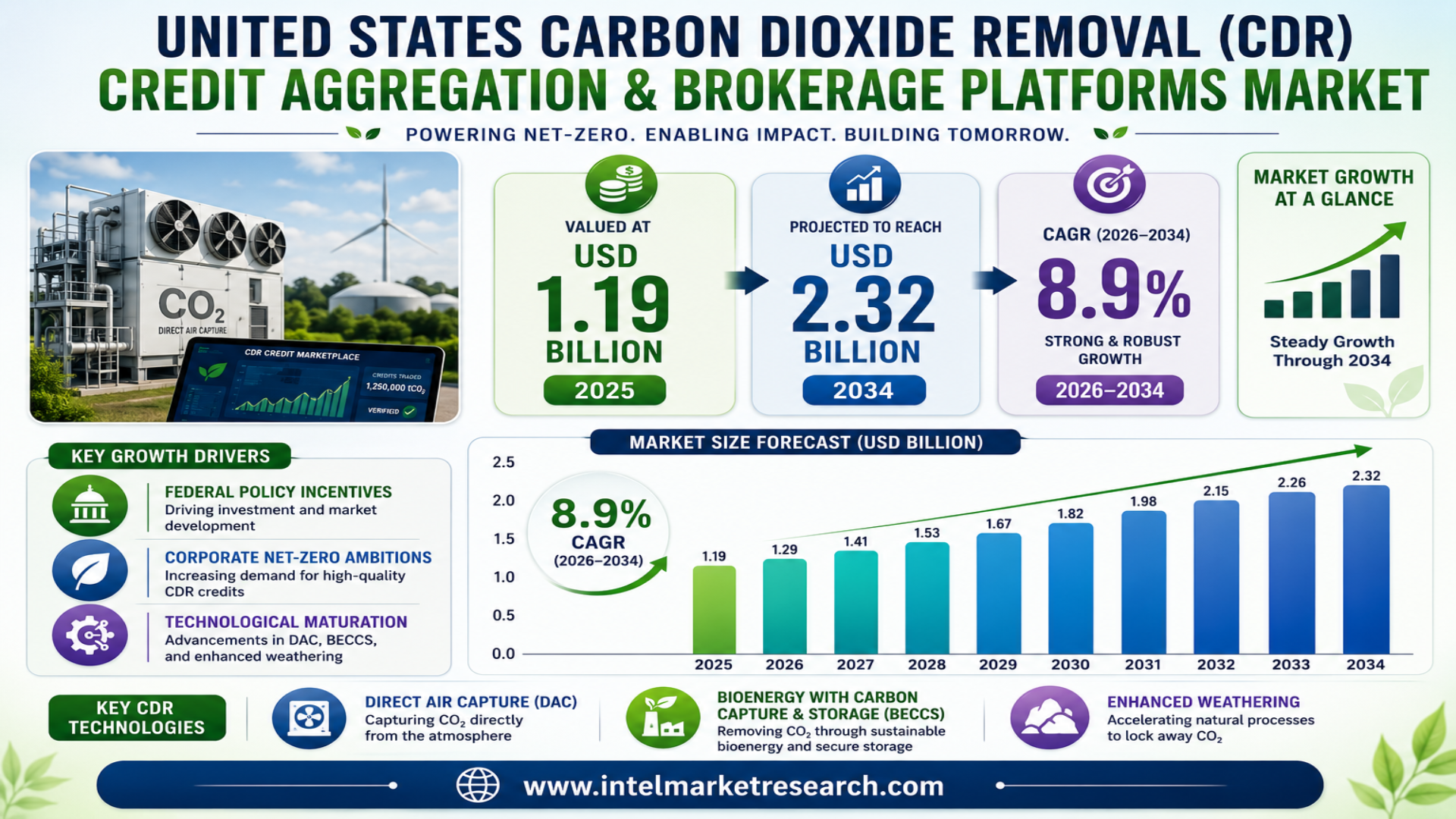

According to a new report from Intel Market Research, the United States Carbon Dioxide Removal (CDR) Credit Aggregation and Brokerage Platforms market was valued at USD 1.19 billion in 2025 and is projected to reach USD 2.32 billion by 2034, growing at a robust CAGR of 8.9 % during the forecast period (2026‑2034). This expansion is being driven by a confluence of federal policy incentives, accelerating corporate net‑zero ambitions, and rapid technological maturation across direct‑air‑capture, bio‑energy with carbon capture and storage, and enhanced weathering projects.

Carbon Dioxide Removal (CDR) credit aggregation platforms act as digital marketplaces that consolidate verified removal credits from a diverse portfolio of projects-ranging from large‑scale direct‑air‑capture plants to smaller bio‑char or mineralization initiatives-and broker them to corporate buyers seeking compliance or voluntary offsets. By providing standardized verification, transparent pricing, and streamlined transaction workflows, these platforms reduce friction between project developers and end‑users, creating a more liquid and trustworthy market for permanent CO₂ removal.

📥 Download FREE Sample Report:

United States Carbon Dioxide Removal (CDR) Credit Aggregation and Brokerage Platforms Market - View in Detailed Research Report

📘 Get Full Report Here:

https://www.intelmarketresearch.com/united-states-carbon-dioxide-removal-credit-aggregationbrokerage-platforms-market-50345

These platforms serve as intermediaries that perform three core functions: (1) aggregation – collecting verified removal credits from multiple projects into a single, audit‑ready pool; (2) verification – applying consistent, often third‑party, standards to ensure permanence, additionality, and avoidance of double counting; and (3) brokerage – matching pooled credits with demand from corporations, financial institutions, and government programs. The digital nature of these services enables real‑time monitoring, automated escrow, and API‑driven integration with corporate ESG reporting systems.

Policy Incentives and Carbon Pricing

The 2023 Inflation Reduction Act introduced a 45Q tax credit of up to $180 per metric ton of CO₂ permanently stored, creating a powerful financial incentive for project developers to generate verified removal credits. State‑level carbon pricing mechanisms in California, Washington, and the Midwest further amplify demand by rewarding verified CDR actions within regional cap‑and‑trade schemes.

Technological Maturation and Scale

Direct‑air‑capture (DAC) technology has seen unit‑cost reductions of roughly 15 % year‑on‑year due to advances in sorbent materials and modular plant designs. Similarly, bio‑energy with carbon capture and storage (BECCS) and enhanced weathering projects have achieved higher capture efficiencies, expanding the pipeline of eligible credits available for aggregation.

➤ “Aggregated credits provide the liquidity needed for large enterprises to meet net‑zero pledges without over‑paying for individual projects.”

Corporate Net‑Zero Commitments

Over 80 % of Fortune 500 companies have set net‑zero targets for 2050, translating into a multi‑billion‑dollar demand for high‑quality removal credits. Platforms that can bundle heterogeneous project types into a single, auditable offering are uniquely positioned to capture this corporate spend.

Regulatory Uncertainty and Market Fragmentation

While federal incentives are strong, the United States still lacks a unified definition of a “CDR credit.” Divergent state registries and varying verification methodologies increase compliance costs for brokers that must reconcile multiple standards before offering aggregated products.

Liquidity Constraints

Secondary‑market depth remains limited, especially for early‑stage or niche removal technologies. Smaller projects often experience delayed sales, leading to price volatility that can discourage developers from entering the aggregation ecosystem.

High Transaction Costs

Verification, escrow, and legal services can consume up to 12 % of the transaction value. These costs erode profit margins for brokerage firms and raise price ceilings for corporate buyers, slowing the rate at which new credits are bundled and sold.

Emerging Corporate Net‑Zero Commitments

With a growing proportion of the corporate sector committing to Science‑Based Targets (SBTi) and net‑zero pathways, there is a clear opportunity for platforms that integrate automated reporting dashboards, tokenized credit ownership, and real‑time verification. Such capabilities lower the barrier for mid‑size manufacturers and utilities that wish to offset hard‑to‑abate emissions.

Financing Innovation

Green‑bond issuances and climate‑focused loan facilities are increasingly using CDR credit aggregation platforms as conduits for capital deployment. By packaging credits into tranches, brokers can attract institutional investors seeking predictable cash flows, while developers obtain lower‑cost financing for scaling up removal projects.

Segment Analysis:

|

Segment Category |

Sub‑Segments |

Key Insights |

|

By Type |

|

Voluntary platforms dominate early activity, offering flexible purchasing options across multiple project developers.

|

|

By Application |

|

Corporate net‑zero offsetting is the primary driver, with platforms providing a single interface to source diverse removal methods, streamline ESG reporting, and support long‑term climate‑risk strategies. |

|

By End User |

|

Corporations lead demand, valuing platforms that can guarantee permanence, provide integrated dashboards, and offer long‑term supply contracts. |

|

By Technology |

|

Direct Air Capture attracts aggregators because its credits are easily quantifiable, highly traceable, and compatible with emerging verification standards. |

|

By Service Model |

|

Broker‑Driven Matching remains essential for large corporate buyers that require bespoke contract terms, risk‑adjusted pricing, and post‑transaction impact reporting. |

The United States continues to be the dominant market for CDR credit aggregation and brokerage platforms. Federal tax incentives, a sophisticated financial services sector, and a high concentration of both removal technology providers and corporate buyers create a virtuous cycle of supply and demand. State‑level carbon pricing programs in California, Oregon, and the Northeastern corridor further stimulate platform activity by providing additional revenue streams for verified credits.

Key growth drivers in the United States include:

Robust federal incentives such as the 45Q tax credit.

Broad corporate net‑zero commitments across energy, manufacturing, and technology sectors.

Advanced digital infrastructure enabling blockchain‑based registries and AI‑driven credit matching.

Active participation from institutional investors seeking climate‑aligned assets.

The market is characterized by a mix of established technology firms, specialized carbon‑market intermediaries, and fast‑growing startups. Leading platforms-Climeworks, Pachama, Carbon Direct, and Indigo Ag-operate end‑to‑end solutions that encompass project onboarding, verification, aggregation, and brokerage. Their scale and reputation help lower transaction costs, attract large corporate accounts, and set industry‑wide verification benchmarks.

Several niche players focus on particular segments of the CDR ecosystem, such as high‑durability DAC credits, nature‑based solutions, or emerging ocean‑based mineralization methods. Non‑profit registries and consortium initiatives also play a critical role in standardizing protocols, enhancing market liquidity, and providing third‑party assurance.

List of Key Carbon Dioxide Removal (CDR) Credit Aggregation and Brokerage Platforms Companies Profiled

Charm Industrial

Running Tide

Climeworks (via partnerships)

CarbonBetter

Carbonfund.org Foundation

South Pole (U.S. office)

Greenhouse by Closed Loop Partners

CarbonCure Technologies (via credits)

Nori

Planet FWD

Digital brokerage technologies are reshaping the competitive environment. Blockchain‑based registries now provide immutable credit provenance, while AI‑driven matching algorithms accelerate buyer‑seller pairing and price discovery. Standardized verification protocols-developed jointly by industry consortia and federal agencies-are reducing the time required to certify permanence and additionality.

API connectivity allows corporate ESG platforms to pull real‑time credit data directly into sustainability dashboards, eliminating manual data reconciliation and improving auditability. Tokenization of credits enables fractional ownership, opening the market to smaller investors and providing additional liquidity for early‑stage removal projects.

The United States market is expected to more than double in size by 2034, driven by the combined effect of expanding policy support, deeper corporate demand, and continued cost reductions in removal technologies. As platform operators mature, we anticipate a shift from purely transactional brokerage toward integrated service models that include portfolio advisory, impact reporting, and climate‑risk analytics.

In the longer term, the convergence of a unified federal definition for CDR credits, broader adoption of digital registries, and sustained private‑sector financing will likely erase many of the current market frictions, creating a highly liquid, transparent, and scalable market for permanent CO₂ removal.

Global and U.S. market size (historical and forecast) covering 2025‑2034.

Detailed segmentation by type, application, end‑user, technology, and service model.

Comprehensive competitive profiling of 15+ key platform providers.

In‑depth analysis of policy incentives, tax credits, and state‑level carbon pricing.

Technology roadmap highlighting AI, blockchain, and tokenization trends.

Strategic recommendations for investors, developers, and corporate sustainability officers.

The market is poised for strong growth, with a CAGR of 8.9 % through 2034.

Federal tax credits (45Q) and state carbon‑pricing schemes are the primary policy catalysts.

Corporate net‑zero commitments create a sizable, recurring demand pool.

Digital infrastructure (blockchain, AI, APIs) is reducing transaction costs and enhancing transparency.

Consolidation among platforms is expected as larger brokers acquire niche aggregators to achieve economies of scale.

Intel Market Research is a leading provider of strategic intelligence, offering actionable insights in biotechnology, pharmaceuticals, and healthcare infrastructure. Our research capabilities include:

Real-time competitive benchmarking

Global clinical trial pipeline monitoring

Country-specific regulatory and pricing analysis

Over 500+ healthcare reports annually

Trusted by Fortune 500 companies, our insights empower decision‑makers to drive innovation with confidence.

🌐 Website: https://www.intelmarketresearch.com

📞 Asia-Pacific: +91 9169164321

🔗 LinkedIn: Follow Us