Future Scope and Innovations in the Machine Vision System Market

Other |

2025-12-22 07:22:01

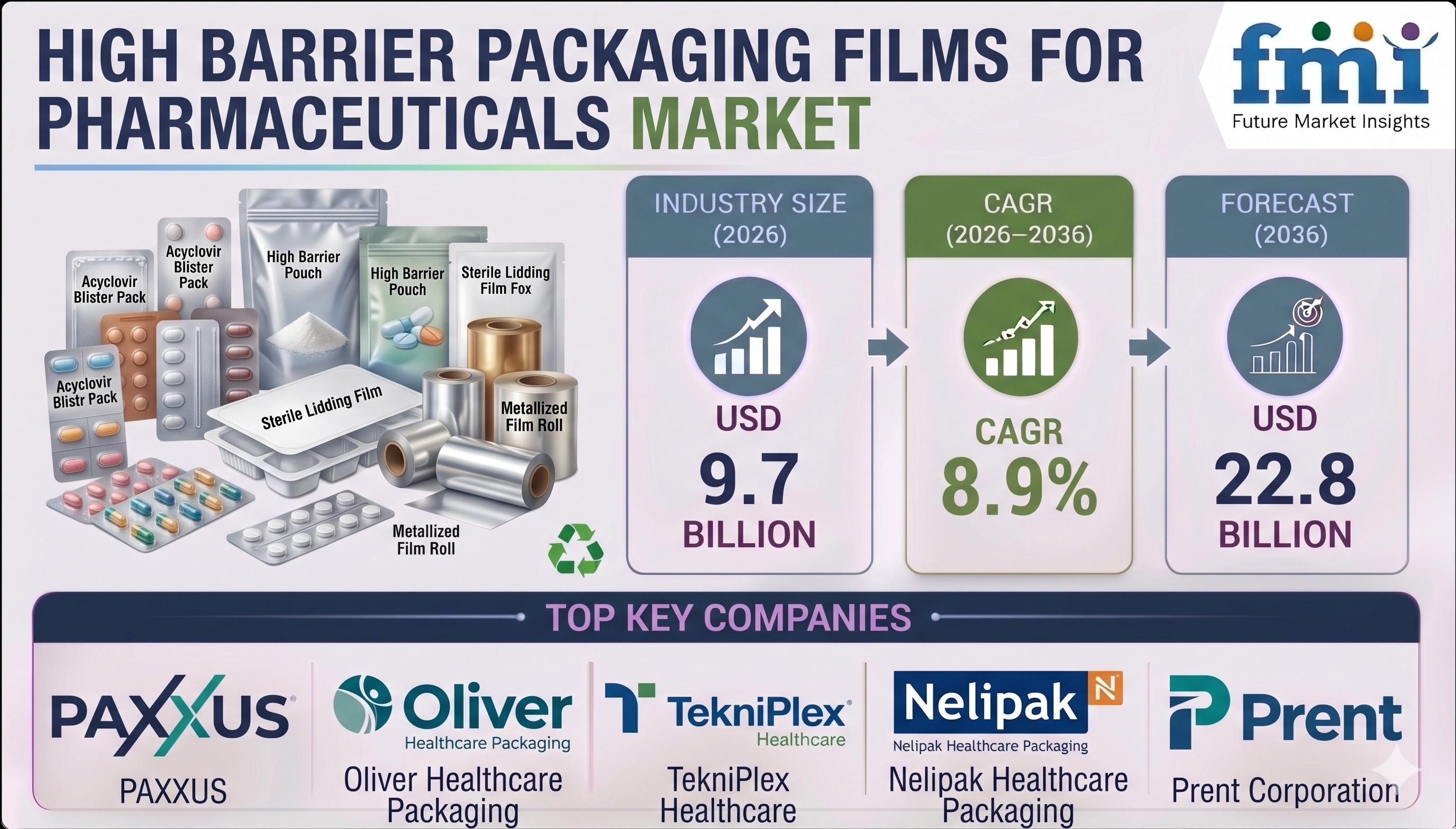

The high barrier packaging films for pharmaceuticals market is entering a decisive growth phase as drug manufacturers worldwide prioritize product safety, regulatory compliance, and extended shelf life. Valued at USD 9.7 billion in 2026, the market is forecast to reach USD 22.8 billion by 2036, expanding at a robust CAGR of 8.9%.

This momentum reflects the increasing complexity of pharmaceutical formulations and the rising need for packaging materials that can protect medicines against moisture, oxygen, light, and contamination across long and often climate-diverse supply chains. From generic tablets to high-value biologics, pharmaceutical companies are investing in advanced barrier films as a strategic layer of product protection.

Industry Meaning

High barrier pharmaceutical packaging films are specialized multilayer materials engineered to deliver controlled barrier performance. Their primary role is to preserve drug stability by limiting exposure to environmental factors that could degrade active pharmaceutical ingredients (APIs).

These films are widely used in blister packs, strip packs, sachets, and pouches, where sealing accuracy and material consistency are essential. Unlike conventional flexible films, pharmaceutical barrier films are designed for validated performance under strict regulatory frameworks, including stability testing, migration limits, and long-term storage conditions.

Material categories include metallized films, aluminum oxide coated films, silicon oxide coated films, and PVDC coated films, each offering specific advantages in clarity, barrier efficiency, and machinability.

Strategic Outlook

Strategically, high barrier films have become a critical infrastructure component for the pharmaceutical industry. As global drug distribution expands and regulatory scrutiny intensifies, packaging is no longer viewed as a secondary cost center but as a core quality assurance function.

Between 2026 and 2030, adoption will remain concentrated in oral solid dosage forms and vaccines. From 2030 onwards, growth will accelerate in biologics, biosimilars, and specialty therapies, where packaging failure carries significant financial and reputational risks.

Manufacturers capable of delivering validated multilayer films, along with regulatory documentation and technical support, are expected to capture long-term supply contracts with pharmaceutical giants and contract packaging organizations.

Request For Sample Report | Customize Report |purchase Full Report – Sample link

Market Evolution

Historically, pharmaceutical packaging relied on aluminum foil and rigid formats. However, the evolution of coating technology and vacuum metallization has enabled flexible films to achieve comparable or superior barrier performance with lower material usage.

The market has evolved across three major stages:

1. Basic barrier phase – aluminum foil and PVC-based blisters.

2. Advanced coating phase – metallized and oxide-coated films.

3. Smart barrier phase – lightweight multilayer films with traceability features.

Today’s market emphasizes performance consistency, sustainability, and digital integration, making high barrier films a foundational element of modern pharmaceutical packaging systems.

Growth Opportunities

Several growth pathways are shaping future demand:

These opportunities position high barrier films as mission-critical assets for pharmaceutical manufacturers seeking long-term compliance and operational resilience.

Demand Patterns

By material type, metallized films dominate with 43% market share, supported by cost efficiency, scalability, and reliable barrier performance. These films are widely adopted for tablets, capsules, and unit-dose medicines.

By application, blister packaging leads with 48% share, reflecting its unmatched ability to protect individual doses while supporting patient adherence and tamper resistance.

Regionally, demand is strongest in:

The demand pattern shows that high-volume generics and high-value biologics both rely on the same underlying barrier technology, reinforcing the universal importance of these films.

Technology Trends

Technological innovation is the backbone of this market. Key trends include:

Manufacturers are also integrating AI-driven quality inspection systems to detect micro-defects, ensuring barrier consistency across millions of blister units.

Competitive Landscape

The market is moderately consolidated and highly technology-driven. Global leaders maintain dominance through barrier expertise, regulatory compliance, and scale.

Amcor plc holds a strong position with its pharmaceutical blister films and recyclable barrier solutions. Its global manufacturing footprint enables consistent supply across regulated markets.

Klöckner Pentaplast Group specializes in thermoformable pharmaceutical films, widely used for cold-form and PVC replacement applications.

Tekni-Plex Inc. differentiates through high-performance laminates designed for oral solid dosages and diagnostic kits.

Constantia Flexibles and Wipak Group are advancing PVDC-free and recyclable barrier structures, aligning with sustainability requirements.

Asian manufacturers such as Uflex Ltd., Cosmo Films Limited, Toray Industries Inc., and Mitsubishi Chemical Corporation are expanding pharmaceutical film portfolios with oxide coatings and multilayer technologies.

Competition increasingly revolves around:

Emerging suppliers focusing on digital traceability and lightweight structures are gaining traction, particularly in Asia-Pacific.

Executive-Level Insights

Conclusion

High barrier packaging films have become indispensable enablers of pharmaceutical safety and compliance. As drug formulations become more complex and supply chains more global, the demand for reliable, validated, and intelligent barrier materials will continue to accelerate. Over the next decade, companies that combine advanced coating technologies, sustainable material innovation, and regulatory expertise will define the future of pharmaceutical packaging. High barrier films are no longer just protective layers they are strategic assets safeguarding the global healthcare ecosystem.

Why FMI: https://www.futuremarketinsights.com/why-fmi

About Future Market Insights (FMI)

Future Market Insights, Inc. (FMI) is an ESOMAR-certified, ISO 9001:2015 market research and consulting organization, trusted by Fortune 500 clients and global enterprises. With operations in the U.S., UK, India, and Dubai, FMI provides data-backed insights and strategic intelligence across 30+ industries and 1,200 markets worldwide.

Contact Us:

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware – 19713, USA

T: +1-347-918-3531

For Sales Enquiries: [email protected]