Deep Dive into Specific Applications and Dimmers Market Segment Analysis

Home |

2026-03-24 06:11:41

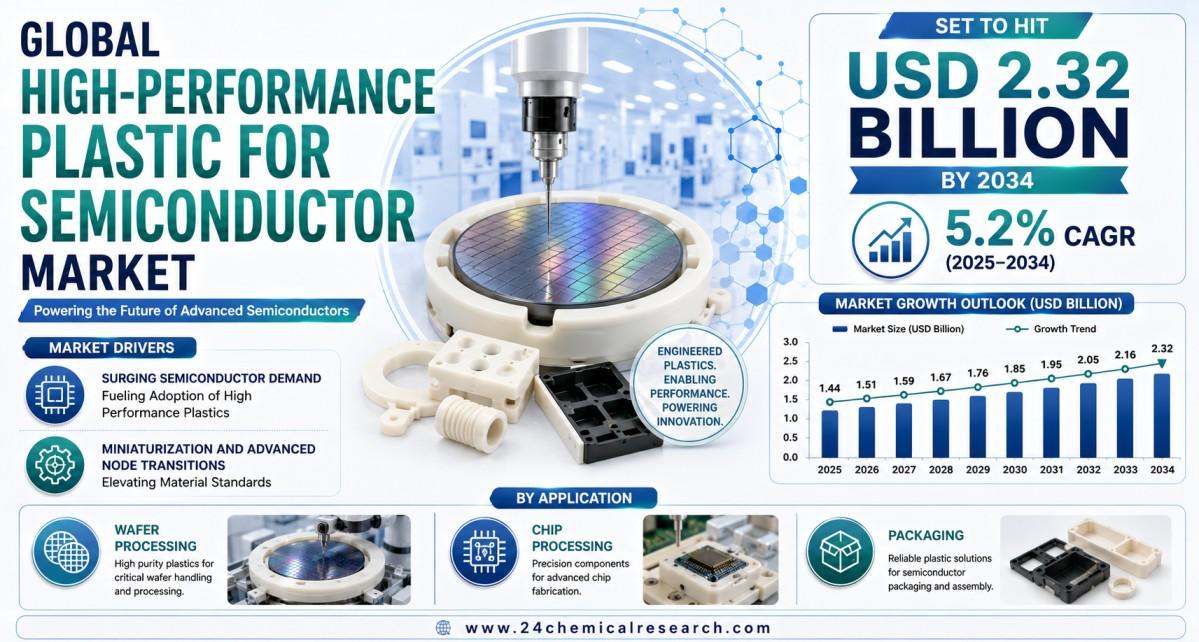

Global high performance plastic for semiconductor market size was valued at USD 1.45 billion in 2025 and is projected to grow from an estimated USD 1.55 billion in 2026 to USD 2.32 billion by 2034, exhibiting a compound annual growth rate (CAGR) of 5.2% during the forecast period.

High performance plastics are a class of polymeric materials engineered to withstand extreme conditions, including high temperatures, aggressive chemicals, and mechanical stress, which are prevalent in semiconductor manufacturing. These materials are crucial for components in wafer processing, chip processing, and packaging, where exceptional purity, dimensional stability, and resistance to plasma and corrosive etchants are non-negotiable. Key material types include Fluoropolymers (FEP, PTFE, PVDF), Polyether Ether Ketone (PEEK), Polyetherimide (PEI), and High-Density Polyethylene (HDPE).

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/306266/high-performance-plastic-for-semiconductor-market

Asia-Pacific stands as the undisputed leader in the High Performance Plastic for Semiconductor market, anchored by the world's most concentrated and advanced semiconductor manufacturing ecosystem. The region encompasses critical production hubs in Taiwan, South Korea, Japan, and China, which together host the majority of global semiconductor fabrication capacity. High-performance plastics such as PEEK, PTFE, and PVDF are in continuous and intense demand across these hubs, where they serve essential roles in wafer carriers, chemical delivery systems, wet benches, and chamber components. The region benefits from robust government-backed investments in new fabrication plant construction, as well as deep integration between plastic material suppliers and major foundries and integrated device manufacturers.

North America is shaped by a strong emphasis on research, development, and cutting-edge manufacturing. The United States serves as the primary demand center, hosting major semiconductor equipment manufacturers and prominent integrated device manufacturers whose facilities require materials meeting the most stringent purity and performance standards. Demand is particularly robust for high-temperature-resistant polymers such as PEEK and PEI, which are essential for components in advanced logic and memory chip production environments. Government-led initiatives focused on reshoring and expanding domestic semiconductor manufacturing capacity are expected to generate meaningful incremental demand for high-performance plastic components in the coming years.

The market thrives on several converging trends: surging semiconductor demand fueling adoption of high performance plastics with materials such as PEEK, polyimide, polyphenylene sulfide, and liquid crystal polymers becoming indispensable in wafer handling, chip packaging, and etch chambers, miniaturization and advanced node transitions elevating material standards with the push toward sub-7nm and sub-3nm process nodes demanding materials that can maintain dimensional stability and chemical purity at microscopic tolerances, and government-backed semiconductor reshoring initiatives across the United States, Europe, Japan, and South Korea accelerating the construction of new fabrication facilities. Emerging opportunities include advanced packaging growth opening new application frontiers for specialty polymers with polymer-based dielectric layers, low-loss substrate materials, and thermally conductive encapsulants increasingly required, semiconductor fab capacity expansion creating sustained long-term demand with announced fabrication capacity expansions across Taiwan, South Korea, the United States, Germany, Japan, and India, and material innovation and bio-based alternatives enabling differentiated market positioning with research programs targeting bio-derived precursors for high-temperature polymers.

While the outlook remains positive, the industry faces constraints including complex qualification processes and extended supplier approval timelines with qualification cycles spanning twelve to thirty-six months, raw material volatility and supply chain concentration with disruptions introducing significant price volatility and supply unpredictability, technical limitations at emerging process boundaries with some high performance plastics exhibiting marginal stability under prolonged EUV radiation exposure, high material costs limiting penetration in cost-sensitive segments with synthesis involving complex polymerization processes and stringent purity controls, and regulatory pressure and environmental compliance complexities with evolving restrictions on PFAS under frameworks being advanced in the European Union and the United States.

FEP

PEEK

PTFE

HDPE

PVDF

PEI

Others

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/306266/high-performance-plastic-for-semiconductor-market

Wafer Processing

Chip Processing

Packaging

Others

Solvay (Belgium)

Evonik (Germany)

Ensinger (Germany)

Saint-Gobain (France)

Mitsubishi Chemical (Japan)

TOHO KASEI (Japan)

Kingfa Science & Technology (China)

Boedeker Plastics (US)

This comprehensive report analyzes the global and regional markets for High Performance Plastic for Semiconductor, covering the period from 2026 to 2034. It includes detailed insights into the current market status and outlook across various regions and countries, with specific focus on:

Sales, sales volume, and revenue forecasts

Detailed segmentation by type and application

Additionally, the report offers in-depth profiles of key industry players, including:

Company profiles

Product specifications

Production capacity and sales

Revenue, pricing, gross margins

Sales performance

The competitive analysis section benchmarks key players against critical success factors while identifying emerging threats from new market entrants. Special attention is given to technological advancements in polymer formulations and emerging application areas.

Our research methodology included extensive interviews with industry executives, formulators, and raw material suppliers across the value chain. The study examined:

Changing formulation trends in high-performance polymer chemistry

Innovation pipelines of leading manufacturers

Regulatory developments impacting product adoption

Supply chain optimization strategies

Customer preferences and purchasing criteria

Get Full Report Here: https://www.24chemicalresearch.com/reports/306266/high-performance-plastic-for-semiconductor-market

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

Plant-level capacity tracking

Real-time price monitoring

Techno-economic feasibility studies

With a dedicated team of researchers possessing over a decade of experience, we focus on delivering actionable, timely, and high-quality reports to help clients achieve their strategic goals. Our mission is to be the most trusted resource for market insights in the chemical and materials industries.

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/

Follow us on LinkedIn: https://www.linkedin.com/company/24chemicalresearch