LTCC and HTCC Market Size, Growth Analysis, Industry Trends, and Forecast to 2033

Causes |

2026-04-06 13:36:39

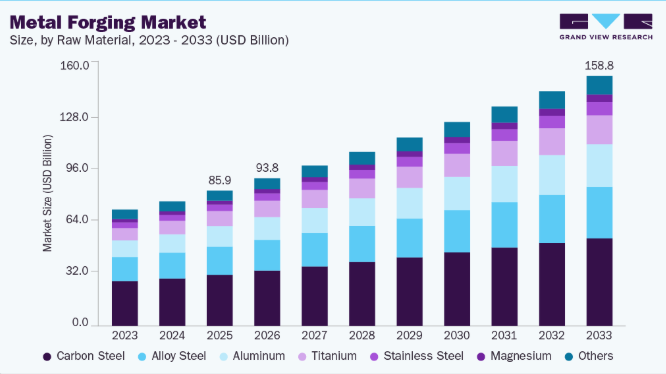

The global Metal Forging Market was valued at USD 85.9 billion in 2025 and is projected to grow from USD 93.8 billion in 2026 to USD 158.8 billion by 2033, registering a CAGR of 7.8% from 2026 to 2033. The market continues to expand due to the increasing demand for high-strength, precision-engineered, and durable metal components across industries such as automotive, aerospace, oil & gas, heavy machinery, construction, railways, and energy.

Metal forging remains one of the most reliable manufacturing processes for producing components capable of withstanding extreme mechanical loads and harsh operating environments. Unlike conventional manufacturing methods, forging improves grain flow, fatigue resistance, impact strength, and structural integrity, making forged components the preferred choice for safety-critical applications.

Rapid industrialization, expanding infrastructure investments, and the modernization of transportation and energy systems—particularly in emerging economies—continue to accelerate demand for forged products. Construction equipment, railway infrastructure, renewable energy installations, and industrial machinery increasingly rely on forged components to achieve superior operational reliability and extended service life.

The market is also benefiting from manufacturers' growing emphasis on product quality, lifecycle performance, and operational efficiency. These factors continue to strengthen the adoption of forged components over cast or fabricated alternatives across multiple industries.

Technological Advancements Driving Modern Metal Forging

The metal forging industry is undergoing significant transformation through automation, digital manufacturing, and advanced process optimization.

Manufacturers are increasingly integrating:

These technologies improve production accuracy, reduce material waste, shorten production cycles, and enhance overall manufacturing efficiency. At the same time, real-time monitoring systems enable better process control, helping manufacturers consistently produce high-performance forged components while minimizing operational costs.

Emerging Industry Trend: Lightweight and Sustainable Forging Materials

One of the most significant trends shaping the metal forging market is the growing adoption of lightweight metals such as aluminum and magnesium. Industries are increasingly seeking materials that reduce overall product weight without compromising structural strength. This trend aligns with global sustainability initiatives aimed at improving energy efficiency, reducing fuel consumption, and lowering carbon emissions across automotive, aerospace, and transportation sectors.

Key Market Trends & Insights

Carbon Steel Continues to Dominate Raw Material Demand

Automotive Industry Remains the Largest Application Segment

Looking for more specific insights? Customize this report to suite your business needs

Although the transition toward electric mobility reduces demand for certain internal combustion engine components, it simultaneously creates new growth opportunities for advanced forged structural and safety-critical parts.

Infrastructure and Industrial Expansion Strengthening Demand

Growing investments in transportation networks, renewable energy projects, industrial manufacturing, mining equipment, and urban infrastructure continue to generate strong demand for forged metal components.

Forged products are increasingly used in:

Their exceptional mechanical strength and long operational lifespan make them indispensable in applications where reliability and safety are essential.

Regional Highlights

Asia Pacific Leads the Global Market

China Remains the Largest Country Market

Market Size & Forecast

Competitive Landscape

The global metal forging market is highly competitive, with manufacturers focusing on capacity expansion, advanced forging technologies, precision engineering, and product diversification to strengthen their market position.

Key competitive strategies include:

Growing demand for customized, high-strength forged components is encouraging companies to invest in advanced manufacturing processes capable of meeting increasingly stringent performance and quality requirements.

Arconic Inc.

Arconic Inc. is a leading manufacturer of aluminum-based engineered products serving the aerospace, automotive, and construction industries. The company specializes in producing lightweight, high-performance structural components designed to improve efficiency and durability. Formerly known as Arconic Rolled Products Corporation, the company adopted the name Arconic Corporation in 2020 following corporate restructuring. Its focus on advanced aluminum technologies continues to support innovation across multiple end-use industries.

Bharat Forge Limited

Bharat Forge Limited, a flagship company of the Kalyani Group, is one of the world's largest forging manufacturers with operations spanning automotive, industrial, aerospace, defense, oil & gas, and railway sectors. The company offers an extensive portfolio that includes crankshafts, connecting rods, chassis systems, oil & gas forgings, and aerospace-grade components such as landing gear parts. Its vertically integrated manufacturing capabilities, global production footprint, and emphasis on precision engineering have established Bharat Forge as a leading supplier of high-performance forged products.

Key Metal Forging Companies

The following companies are among the leading participants in the global metal forging market:

Conclusion

The global metal forging market is positioned for robust growth, driven by increasing demand for high-strength, lightweight, and precision-engineered components across automotive, aerospace, energy, construction, and heavy industrial sectors. As manufacturers prioritize product durability, operational efficiency, and sustainability, forged components continue to outperform alternative manufacturing methods in critical applications.

The accelerating transition toward electric vehicles, expanding infrastructure development, and widespread adoption of advanced manufacturing technologies are creating new opportunities for industry participants. With Asia Pacific maintaining market leadership and innovation centered on automation, lightweight alloys, and digital forging technologies, the metal forging industry is expected to remain a vital contributor to global industrial and manufacturing growth throughout the forecast period.

Looking for a report customized to your requirements? Explore our Custom Research Offering

Grand View Research offers

And much more…