Strategic Outlook 2026: Crude Sulfate Turpentine Market — PW Consulting Executive Brief

As the marketplace for renewable pine-derived feedstocks reshapes industrial value chains, PW Consulting’s latest Crude Sulfate Turpentine Market report offers a timely, decision-oriented perspective for executives planning through 2026 and beyond. Our independent analysis blends a granular assessment of supply dynamics, regulatory inflection points, and competitive positioning with a forward-looking demand model. The headline: the CST market entered 2026 from a position of steady expansion and is set to continue growing — but the nature of that growth will be defined by certification, pricing volatility, and strategic upstream-downstream alignment.

Crude Sulfate Turpentine Market

Why this matters for 2026 decision-makers

- Transitional opportunity: CST is no longer a marginal co-product; it is a strategic renewable feedstock in fragrance, adhesives, coatings, and industrial chemistries. Firms that treat it as a core raw material can capture premium positioning as buyers shift toward certified bio-based inputs.

- Regulatory gating: Emerging certification and chemical regulation regimes are already re-shaping market access — absent proactive compliance and traceability, suppliers and traders will face restricted entry to major European and North American markets.

- Price and supply risk: Short-term price shocks and contract repricing have become more frequent; procurement and commercial teams must recalibrate sourcing strategies to manage margin pressure and secure continuity.

Market trajectory at a glance

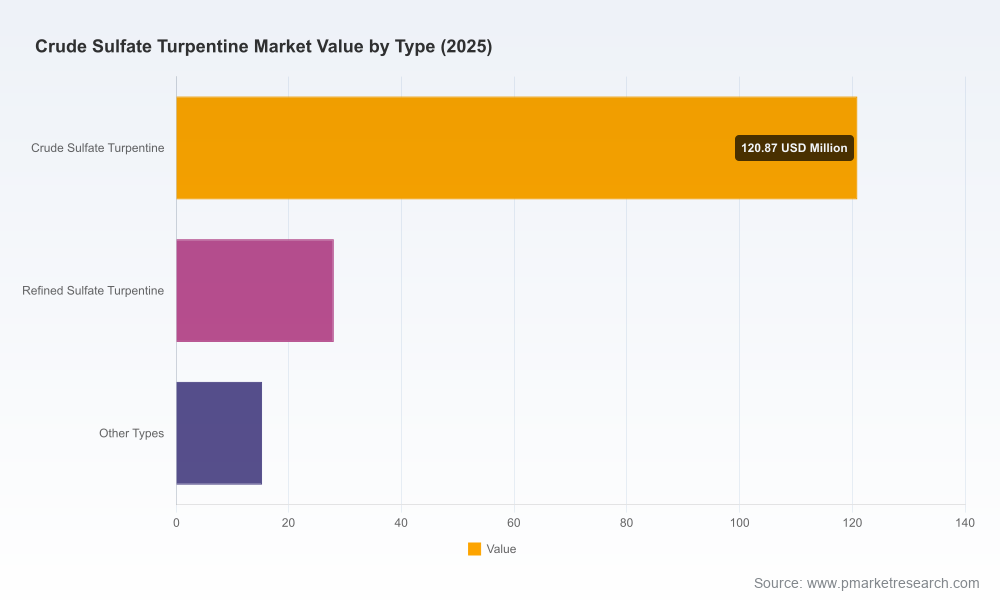

PW Consulting’s model reports the CST market expanding from a mid‑triple‑digit base in the early 2020s to a significantly larger market by the end of the decade. Between the historical window (2020–2025) and our forecast period (2026–2032), the market exhibits a compound annual growth drive consistent with a 5.65% CAGR across the forecast horizon. To put this into operational context: the market moved from its 2020 scale through steady annual gains into the 2025 base year, and our scenarios show sustained compound growth through 2032 under the central case. While these topline figures are directional and robust, the decisive differentiator for participants will be how growth segments by application and region evolve — detail that our full report preserves for subscribers and strategic partners.

Crude Sulfate Turpentine Market

Demand, supply and price dynamics

- Demand profiles are bifurcating. Traditional industrial uses (paper & pulp-related chemistries, industrial resins) continue to consume a meaningful share of available volumes, while higher-value segments (aroma chemicals, specialty terpene derivatives for flavors & fragrances, cosmetic intermediates, and bio-based adhesives/coatings) are absorbing incremental demand due to sustainability preferences.

- Supply remains closely linked to kraft pulp operations. Many leading pulp producers generate CST as a co-product; their operational decisions on pulp throughput, mill maintenance, and tall oil processing directly affect CST availability. This linkage creates a supply rhythm tied to pulp cycle economics rather than pure terpene market fundamentals.

- Price volatility is increasingly visible. Recent supplier actions in 2026 — including material price increases announced by major producers — underline the emergence of tighter pricing dynamics. Stakeholders must expect episodic re-pricing windows that can compress downstream margins absent contractual mechanisms like indexation, hedging, or longer-term offtake agreements.

- Sustainability and certification are becoming de facto price multipliers. Buyers paying a premium for certified bio-based feedstocks (and suppliers able to demonstrate chain-of-custody) will achieve advantaged access to premium applications and geographies.

Competitive landscape — what to watch

The industry features a mix of pulp-mill-integrated suppliers, specialty chemical houses, and global fragrance and flavor companies that convert CST-derived terpenes into higher-value products. Key strategic dynamics include integration versus specialization, certification-led differentiation, and the commercial responses of incumbent pulp suppliers to growing downstream demand.

Crude Sulfate Turpentine Market

- Kraton Corporation — An example of a specialty player that has moved to both capture value through branded terpene products and signal commercial pricing intent; recent public actions in 2026 (price increases and ISCC PLUS certification for a US facility) provide a clear playbook for combining price discipline with certified positioning.

- DRT and Pine Chemical Group — Longstanding resins and terpene specialists that leverage deep process know-how and established downstream customer relationships; they remain pivotal partners for fragrance and industrial buyers seeking traceable feedstocks.

- Symrise, IFF, Privi and other aroma houses — These global formulators represent demand pull for high‑purity terpene streams and increasingly expect suppliers to meet sustainability and regulatory requirements as a minimum commercial condition.

- Pulp and paper majors (e.g., large Nordic and North American producers) — Their decisions on refining, co-product allocation, and partnership models will determine available merchant volumes and long-term stability of supply.

- Specialty chemical suppliers and regional champions — Firms focused on adhesives, coatings, and industrial specialties can convert CST into differentiated products, though scaling requires capital investment and regulatory compliance investments.

Regulatory and sustainability inflection points

Regulatory trajectories are converging on favoring certified renewable feedstocks. The tightening of frameworks such as REACH and the European Green Deal’s procurement preferences, together with industry-level requirements that mirror ISCC PLUS certification, mean access to key markets will increasingly depend on verifiable sustainability credentials. Our analysis indicates that by 2028, certain European segments will treat certified sourcing not as a differentiator but as a prerequisite for commercial participation. The compliance costs — certification, traceability systems, and upgraded storage/handling — are real and must be budgeted into product economics.

Strategic playbook for 2026 — recommended actions

- For producers: accelerate certification and traceability programs now; prioritize long-term offtake contracts with tier‑one aroma houses; evaluate selective downstream integration to capture margin uplift in specialty terpenes.

- For buyers/formulators: build supplier scorecards that weight certification, traceability, and supply continuity; consider collaborative development agreements with producers to secure tailored terpene fractions and stable pricing mechanisms.

- For investors: target suppliers with certified supply chains, captive pulp integration, or differentiated downstream capabilities; stress-test investment cases against regulatory scenarios and episodic price shocks.

- For supply-chain and procurement teams: diversify counterparties across integrated suppliers, specialty refiners, and merchant traders; incorporate indexation or price collars in contracts; model scenario-based supply shocks in working capital planning.

- For policy & sustainability leaders: prioritize investments in chain-of-custody IT and near-term auditing to keep market access open, and quantify the incremental margin capture enabled by certified product streams.

What PW Consulting’s full report delivers

The published report is structured as a practical toolkit for strategic decisions in 2026 and beyond. Subscribers receive:

- A proprietary demand-supply model covering 2020–2025 historical performance and 2026–2032 forecasts, with scenario outputs under alternative regulatory and price assumptions.

- Competitive benchmarking and supplier scorecards with operational, commercial and sustainability metrics on leading firms.

- Commercial due diligence modules, including price-model templates, contract-structure recommendations, and a supplier risk matrix.

- Regulatory roadmap and certification playbook: step-by-step guidance on ISCC PLUS and equivalency pathways for supplier and buyer compliance.

- M&A and investment opportunities: prioritization framework and case studies for value capture through integration or specialization.

- Practical go-to-market templates for producers and distributors seeking to enter or expand in higher‑value aroma and specialty segments.

We intentionally withhold core sub-segment level figures and fine-grain regional splits in this public brief to preserve the report’s role as a strategic subscription asset. Clients who require the full dataset — including proprietary breakouts by application, region and type, plus downloadable model files — can access the complete intelligence package via PW Consulting’s report portal.

Concluding perspective — where to focus in 2026

The critical strategic insight for 2026 is straightforward: crude sulfate turpentine has entered a commercialization phase in which sustainability certification, supply alignment with pulp mill operations, and active commercial contracting will determine winners and losers. Top-line market growth (anchored to the 2025 base year and forecast across 2026–2032 at a mid-single-digit CAGR) creates room for expansion, but the value is concentrated in execution — converting renewable feedstock potential into reliably supplied, certified, and value‑added terpene products.

Next steps & access

Executives crafting 2026 strategies should reassess sourcing policies, accelerate certification timetables, and run scenario analyses against the regulatory pathways outlined above. For clients seeking immediate, operational-ready guidance, PW Consulting offers bespoke briefings, supplier due diligence engagements, and a full-access subscription to the Crude Sulfate Turpentine Market report, which contains the detailed subsegment data and downloadable models necessary to finalize procurement, investment, or M&A decisions.

Contact PW Consulting to schedule a strategic briefing and to obtain the complete report and model package for your team’s 2026 planning cycle.

For detailed analysis of this topic, please visit the official page:Crude Sulfate Turpentine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com