Ethanol in Beverage Market: Strategic Imperatives for 2026 — PW Consulting Industry Brief

PW Consulting’s latest market research report, authored by our Strategy & Industry Analysis practice, provides a forward-looking blueprint for executives, investors and category teams navigating the ethanol supply chain serving the beverage industry. Built from a detailed historical assessment (2020–2025) and a multi-scenario forecast (2026–2032), the study quantifies opportunity and risk across supply, demand and regulation — and translates those insights into executable actions for 2026 decision timetables.

Ethanol in Beverage Market

Executive snapshot

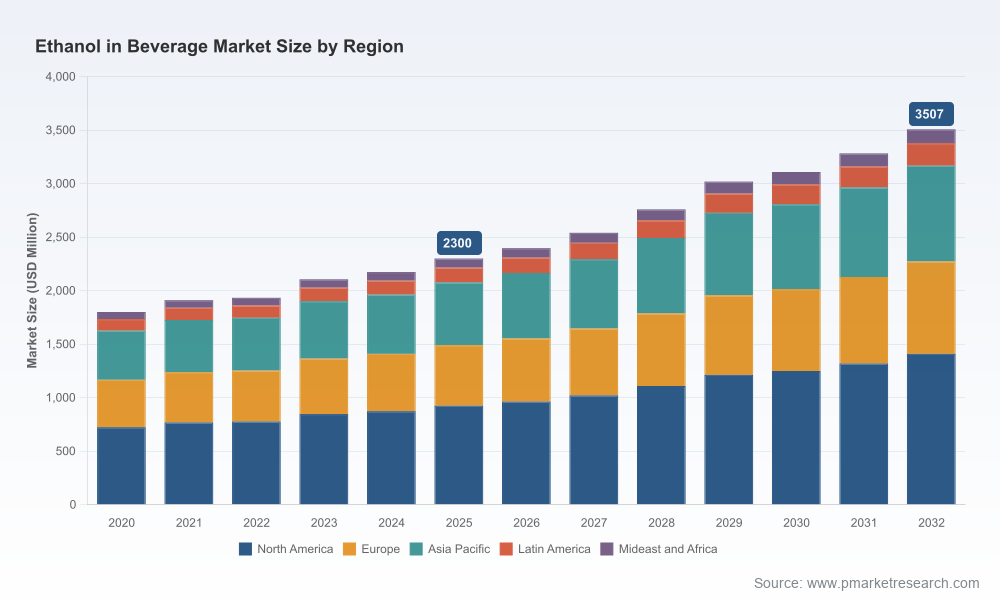

- Market trajectory: the global ethanol-in-beverage market expanded materially over 2020–2025 and reached a base-year size of USD 2,300 Million in 2025. Under our base-case modeling, the market is projected to grow through 2032, reaching approximately USD 3,507 Million by the end of the forecast horizon, driven by steady volume growth and product premiumization at a compound annual growth rate (CAGR) of 6.5% (2026–2032).

- Concentration and competition: the market displays a moderate degree of consolidation; our concentration metrics indicate the top three players account for roughly 35% of supply, and the top five about 42%, leaving meaningful room for regional specialists and new entrants with niche capabilities.

- Timing: 2026 is a strategic inflection year. Regulatory changes, feedstock price variability and capacity investments announced during 2024–2025 are converging to reshape sourcing, pricing and certification priorities for beverage producers and ingredient suppliers alike.

Why this report matters for 2026 planning

Executives must balance short-term continuity with medium-term positioning. The 6.5% CAGR we project through 2032 is attractive, but it is accompanied by concentrated supplier advantages, evolving trade rules and episodic raw-material cost shocks. Our report translates these macro signals into four concrete areas of action for 2026 decision cycles:

Ethanol in Beverage Market

- Supply security and contract design: with moderate market concentration and localized capacity expansions underway, companies must redesign supply agreements to incorporate flexible volumes, premium-quality clauses and contingency lanes for trade-disrupted periods.

- Regulatory compliance as a commercial differentiator: stricter excise and purity requirements are raising the bar for beverage-grade ethanol. Firms that invest now in validated testing, documentation and approved plant configurations will avoid margin erosion and gain faster time-to-market for new SKUs.

- Cost management through feedstock and input hedging: our scenarios show that modest moves in corn prices materially affect margins at beverage-grade purity targets. Pricing playbooks and financial hedges should be embedded into go-to-market planning in 2026.

- Capability-driven M&A and partnerships: targeted deals for dedicated beverage-grade capacity, or long-term offtake arrangements with specialists, create defensible advantage without the full CAPEX burden of greenfield builds.

Report contents — practical, transaction-ready analysis

PW Consulting’s report is deliberately practical. We combine proprietary data with primary interviews and supply-chain mapping to produce decision-ready deliverables that include:

Ethanol in Beverage Market

- Market sizing and growth scenarios (historical 2020–2025 baseline, plus detailed forecasts to 2032) with bottom-up and top-down validation.

- Segment and application analysis that isolates demand drivers for spirits, wine and beer formulations and maps them to supplier capabilities (note: the public summary omits granular segment tables; these are included in the full report).

- Supply-side assessment, including plant-by-plant capacity overlays, purity and certification matrices, and supplier scorecards for procurement prioritization.

- Regulatory compendium and compliance playbook: distilled practical steps for meeting TTB filing requirements, excise protocols and cross-border tariff management.

- Price sensitivity and raw-material scenarios that stress-test margins against corn price trajectories and tariff shocks, with recommended hedging and procurement strategies.

- Competitive landscape and M&A opportunity map: strategic profiles and valuation levers for potential targets or partners, plus our preferred transaction structures for 2026.

- Commercial playbooks and 100-day plans for beverage brands and ingredient suppliers focused on scaling, premiumization and export expansion.

Competitive dynamics — what the market structure means for players

The competitive field is a mix of dedicated beverage ethanol specialists, large integrated ethanol producers and distributors offering turnkey solutions. Representative players covered in the analysis include:

- Pristine Alcohol LLC (United States): positions itself on neutral, high-purity, food-grade ethanol tailored for spirits and ready-to-drink formulations. Their focus underscores the market premium for consistent sensory neutrality and traceable lots.

- Greenfield Global Inc. (Canada): a major producer and supplier with multi-faceted capabilities. Notably, Greenfield commenced construction of a dedicated facility on its Kentucky campus in September 2025 to address rising domestic demand for beverage-grade ethanol — a clear sign that scale owners are prioritizing beverage-specific assets.

- Ethimex Limited (United Kingdom): acts as a sourcing and distribution specialist, emphasizing bulk procurement and logistics solutions for beverage customers and flavor houses.

- Ultra Pure (United States): bulk supplier with a broad product slate and global reach, presenting an option for buyers prioritizing integrated logistics and catalogue breadth.

- Premier Innovations Group (United States): offers clean-ethanol supplies as part of turn-key solutions for beverage brands, combining ingredient supply with co-packing and formulation services.

These archetypes — pure-play quality specialists, large-scale producers building beverage-dedicated lines, and supply-chain integrators — define the strategic choices for any firm in 2026. Our report provides playbooks for competing in each position and a supplier due-diligence checklist to assess operational readiness and compliance performance.

Regulatory and feedstock dynamics shaping near-term choices

Several cross-cutting developments require immediate attention:

- Regulatory tightening: industry oversight and excise frameworks are intensifying. Distilled spirits producers must register with regulators for high-proof production and maintain approvals for nonstandard formulations; internal QA programs and validated lab partnerships are now table stakes.

- Tariff environment: additional tariffs on denatured ethanol introduced in late 2025 have reshaped import economics and created arbitrage for domestically certified beverage-grade streams. Procurement teams need tariff-aware routing strategies and scenario-based cost modeling.

- Feedstock price variability: USDA data show season-average and short-term corn-price movements that underscore the importance of sensitivity analysis. Even modest shifts in corn prices can change supplier economics and influence the viability of certain production modalities (e.g., grain- vs. molasses-based routes).

Strategic recommendations — a 2026 playbook

Based on our findings, PW Consulting recommends a structured approach for leaders making 2026 resource allocation decisions:

- Immediate (0–90 days): run a supplier continuity audit, update contract clauses for purity and certification, and execute short-term hedges for feedstock exposure where appropriate.

- Near term (90–270 days): prioritize investments in traceability and compliance (lab capacity, documentation), finalize contingency logistics lanes that bypass tariff bottlenecks, and formalize offtake agreements with beverage-dedicated producers.

- Medium term (270–540 days): evaluate strategic partnerships or bolt-on acquisitions to secure beverage-grade capacity; deploy premium product launches that leverage verified purity and sustainable sourcing stories.

- Board-level: incorporate scenario planning into capital allocation to capture upside from the projected 6.5% CAGR while stress-testing for regulatory and commodity shocks.

How to use this report in corporate workflows

For corporate strategy, the report functions as a decision support tool that can be directly integrated into procurement RFPs, investor presentations and M&A diligence packs. Practically, clients have used our models to:

- Quantify the value of exclusivity in supplier contracts;

- Calibrate capex for beverage-specific line conversions versus outsourcing;

- Prioritize markets and channels for premiumization investments; and

- Prepare regulatory filings and audit-ready documentation ahead of product launches.

Next steps and where to find the full intelligence

This release is a selective summary intended to highlight the report’s strategic value for 2026. The full PW Consulting Ethanol in Beverage Market report includes proprietary segment tables, supplier scorecards, confidential company benchmarks and downloadable financial models that underpin the conclusions summarized above. These detailed assets are accessible through PW Consulting’s report portal and are provided with consultation time to help teams convert insight into action.

To commission the full report, request a briefing, or discuss a tailored advisory engagement for your organization’s 2026 planning, please contact PW Consulting’s Strategy & Industry Analysis practice via our reports page.

For detailed analysis of this topic, please visit the official page:Ethanol in Beverage Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com