Computed Tomography System Market 2026: Strategic Imperatives for Providers, OEMs and Investors

Executive snapshot

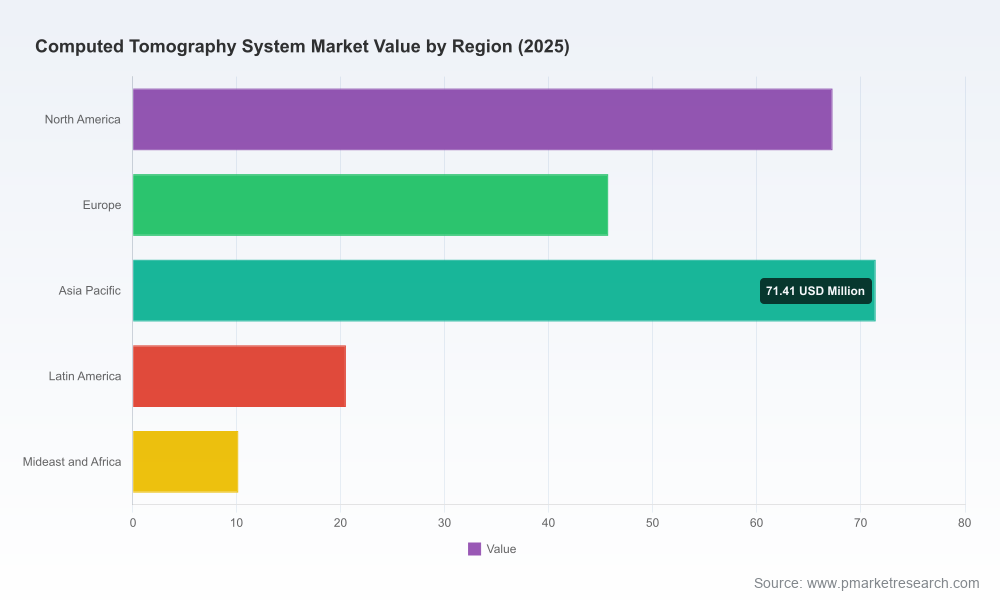

The global Computed Tomography (CT) systems market is at a decisive inflection point. Our PW Consulting market model (base year 2025, revenue unit: Million USD) shows steady expansion from the 2020 baseline to 2025 and projects continued growth through 2032, with a compound annual growth rate (CAGR) of approximately 6.98% across the 2026–2032 forecast window. Under our central scenario the market expands materially between 2025 and 2032, reflecting accelerating uptake of advanced hardware (photon-counting, spectral capabilities), widespread AI workflow adoption, and structural demand driven by ageing populations and rising chronic-disease diagnosis rates.

Computed Tomography System Market

Why this report matters for 2026 decision‑making

- Capital allocation and procurement cycles are compressing. Hospitals and imaging networks face new performance requirements and reimbursement signals that affect purchase timing, replacement strategies and service-contract design.

- Regulatory and standards shifts are creating new compliance and clinical-evidence requirements that will determine which platforms qualify for broader hospital adoption and preferred-provider lists.

- Technology bifurcation is intensifying: premium, high‑throughput systems compete alongside cost‑optimized units for emerging-market share. This creates margin pressure for incumbent OEMs and opens tailored entry points for challengers and regional players.

What the PW Consulting report delivers (practical, action‑ready content)

- Proprietary market-sizing model (historical 2020–2025; forecast 2026–2032) with scenario analysis and sensitivity levers for pricing, replacement cycles and reimbursement changes.

- Go‑to‑market playbooks for OEMs and distributors: product positioning, bundling (service + AI), and channel strategies by buyer segment (large health systems, outpatient networks, private clinics).

- Regulatory and reimbursement tracker: what to expect from standards bodies and payers, and how to sequence clinical validation to maximize uptake and coding opportunities.

- Competitive benchmarking and product-mapping (feature, clinical use-cases, installation footprint and service model) for major vendors and fast-emerging challengers.

- M&A and partnership roadmap: prioritized target archetypes, valuation benchmarks and integration playbooks for buyers seeking inorganic growth or technology infill.

- Operational playbooks for hospitals: procurement timing, TCO modeling, installation and staff-training plans that align with Joint Commission and payer expectations.

Market structure and competitive dynamics — strategic takeaways

The CT market exhibits a moderate-to-high concentration at the top while leaving meaningful room for mid-tier and regional players. The three largest OEMs collectively control a significant share of industry revenues, and the top five command an even larger portion — a structure that favors platform differentiation and ecosystem play.

Computed Tomography System Market

Leading vendors are pursuing divergent paths to capture next-wave value:

Computed Tomography System Market

- GE HealthCare: focused on workflow orchestration and clinical breadth, with platforms that emphasize one‑beat cardiac imaging and integrated AI pipelines to reduce exam times and operator variability.

- Siemens Healthineers: concentrated on premium throughput and novel detector technology, including photon‑counting capabilities that target cardiology, oncology and spectral imaging use‑cases.

- Philips: prioritizing spectral imaging and embedded intelligence, pairing hardware with software services to raise site-level diagnostic consistency and image‑quality guarantees.

- Canon Medical: advancing AI enhancements and matrix/dose innovations; recent regulatory clearances broaden clinical applicability of its flagship systems.

- United Imaging and other ambitious challengers: leveraging AI‑first optimization and mobile/configurable solutions to win in price-sensitive or capacity‑constrained environments, supported by recent regulatory milestones for mobile dual‑energy and other configurations.

- Regional manufacturers and value players: emphasizing accessibility, simplified maintenance and aggressive pricing to capture system volume in emerging markets and mid‑size private networks.

Recent regulatory and corporate developments — for example, expanded approvals for AI-enhanced imaging, facility investments by major OEMs, and FDA 510(k) clearances for mobile and dual‑energy configurations — accelerate the pace at which new capabilities reach clinical practice. At the same time, the effective January 2026 Joint Commission requirement for standardized diagnostic CT protocols elevates the bar for clinical evidence and protocol harmonization across purchasers.

Technology transitions shaping 2026 strategy

- Photon‑counting and spectral imaging: move from R&D to selective clinical adoption. These modalities promise better tissue characterization and potential dose reductions but require new clinical workflows and payer acceptance to generate material revenue uplifts.

- AI and workflow automation: now a baseline expectation for premium platforms. Success will be determined by validated clinical endpoints (time-to-diagnosis, repeat-scan reduction) rather than feature lists alone.

- Portable and mobile CT configurations: important for point-of-care expansion, trauma and ambulatory surgery center demand. Device modularity and ease of installation are differentiators.

- Service and software monetization: recurring revenue from AI subscriptions, cloud analytics and extended warranties is becoming as important as device margins in total portfolio economics.

Regulatory & reimbursement context — immediate implications

Two concurrent forces are reshaping near‑term commercial viability: stricter institutional standards for imaging protocols and an active reimbursement agenda seeking codes for novel CT technologies and AI‑integrated diagnostics. For decision‑makers in 2026 this means:

- Manufacturers must prioritize clinical studies designed to support protocol adoption and payer conversations early in the product lifecycle.

- Healthcare providers should re-evaluate procurement specs to ensure the chosen platform can both comply with updated clinical standards and capture incremental revenue opportunities from new CPT/DRG categorizations.

- Buyers and sellers who move to establish real‑world evidence partnerships today will command advantage in coverage negotiations and preferred vendor arrangements tomorrow.

Actionable strategic recommendations for 2026 (what executive teams should do now)

- Re-optimize portfolio roadmaps: prioritize upgrades that deliver measurable clinical and workflow outcomes tied to the Joint Commission protocols and payer metrics.

- Design evidence-first launch programs: allocate budget to multi-site pilots that generate RWE on dose, throughput and diagnostic yield — these datasets are critical for reimbursement discussions.

- Build channel flexibility: combine direct sales for large systems with distributor and leasing models for mid-market and emerging-market growth.

- Monetize software and services: develop subscription tiers (AI analytics, advanced reconstructions, training) to stabilize revenue over device replacement cycles.

- Target M&A selectively: seek targets that provide access to differentiated detectors, AI stacks, or high-frequency servicing networks to increase installed‑base retention.

- Invest in workforce enablement and remote service capabilities to reduce installation times and accelerate clinical ramp-up at customer sites.

- Engage payers and standards bodies early to co-design coding pathways and coverage policies for photon-counting and AI-enabled workflows.

How PW Consulting supports operationalizing these decisions

PW Consulting’s Computed Tomography System Market report is built as a decision-support toolkit. Beyond narrative analysis we provide:

- Customizable financial and market models (downloadable) so CFOs and strategy teams can stress-test investment scenarios against replacement rates, pricing sensitivity and reimbursement outcomes.

- Vendor selection frameworks and RFP templates to expedite procurement for large health systems and imaging networks.

- Clinical-evidence playbooks and trial designs to accelerate CPT/coverage conversations with payers and standards-setting bodies.

- M&A diligence bundles: vendor evaluations, integration checklists and synergies mapping calibrated to market concentration dynamics and product life cycles.

Next steps and where to find the full intelligence

This release highlights the strategic contours and 2026 imperatives that senior leaders must weigh. It intentionally omits the granular, gated segment-level tables, regional breakdowns and supplier-specific revenue figures that underpin our forecasting model — those datasets and the full vendor benchmarks are available in the complete PW Consulting Computed Tomography System Market report and companion data appendices. Decision-makers seeking a tailored briefing, scenario runs using their own assumptions, or a vendor short‑listing workshop can contact PW Consulting to schedule a strategy session.

Methodology note

The report uses a base year of 2025, covers historical performance from 2020–2025 and forecasts 2026–2032. All revenue figures are expressed in Million USD. Our central forecast reflects a 6.98% CAGR for the 2026–2032 period under the baseline economic scenario; alternate scenarios reflecting accelerated technology adoption and constrained reimbursement are provided within the full report.

For detailed analysis of this topic, please visit the official page:Computed Tomography System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com