Thermal Infrared Imagers Market 2026: Strategic Imperatives from PW Consulting’s New Sector Report

PW Consulting today releases a forward-looking briefing drawn from our full Thermal Infrared Imagers Market report (base year 2025, forecast 2026–2032). The market that stood at approximately USD 7.98 Billion in 2025 has been steadily expanding from earlier in the decade and, driven by accelerating adoption across automotive safety, industrial automation, defence, and public safety, is forecast to continue growing at a double‑digit pace—an 11.11% CAGR across the 2026–2032 horizon that will push total industry revenues materially beyond current levels.

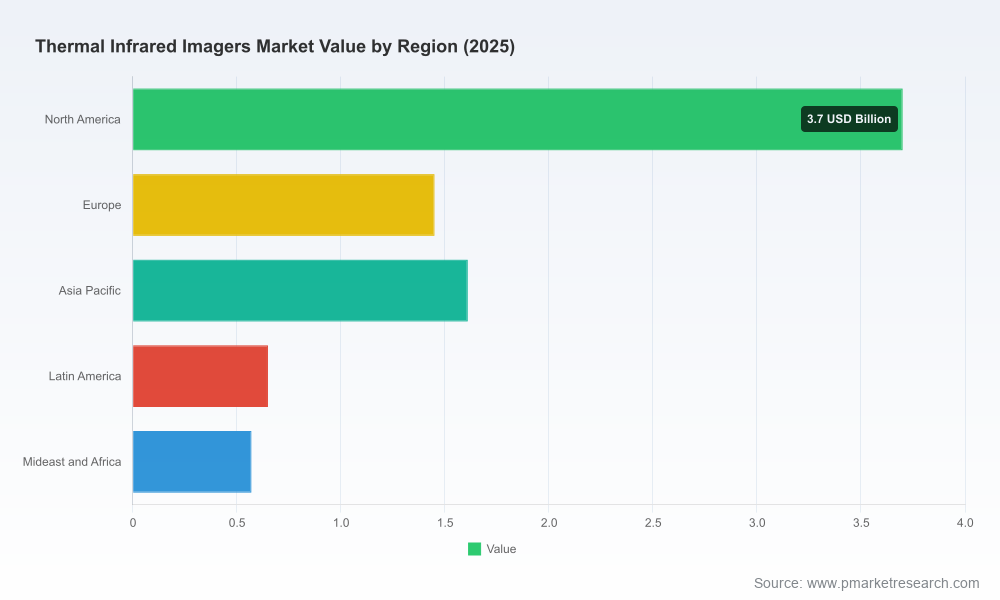

Thermal Infrared Imagers Market

Why this matters for enterprise decision-makers in 2026

Thermal imaging is no longer a niche instrumentation market. Over the past five years providers have moved from specialized professional instruments to integrated modules and sensors embedded in automotive, uncrewed systems, perimeter security, and industrial automation platforms. That transition forces a new set of choices for product leaders, procurement heads, and corporate strategists:

Thermal Infrared Imagers Market

- Supply strategy: componentized module supply chains and the emergence of integrated manufacturers change inventory, lead‑time, and qualification planning.

- Regulatory compliance and product safety: automotive‑grade functional safety standards and sector‑specific certifications increasingly determine addressable opportunities.

- Technology roadmap trade-offs: cooled vs. uncooled detectors, pixel resolution, and LWIR sensitivity are now intrinsic to value propositions rather than optional performance upgrades.

- M&A and partnership timing: consolidation is selective—market concentration remains moderate—which creates windows for targeted acquisitions and strategic alliances.

Our report is written for precisely these stakeholders, providing the analytical inputs and execution playbooks needed to convert market momentum into profitable, defensible positions.

Thermal Infrared Imagers Market

Market dynamics at a glance (strategic context, not a datapack)

From 2020 through 2025 the industry demonstrated resilient expansion as demand migrated from standalone instruments toward embedded modules and systems. The coming forecast period is dominated by three structural drivers:

- Module commoditization and platform integration: leading manufacturers are vertically integrating to deliver higher volumes and lower qualification friction for OEMs, shortening time-to-market for end-system integrators.

- Sectoral acceleration: safety‑critical automotive applications and persistent defense procurement activity are creating high-margin specialty segments alongside large-volume industrial and security markets.

- Technology convergence: advances in sensor resolution, LWIR detector performance and system‑level analytics are elevating thermal imaging from qualitative detection to quantitative sensing used in closed‑loop control and predictive maintenance.

These forces collectively explain why a market approaching USD 8 Billion in 2025 is set to compound at a double‑digit rate through the coming planning cycle. For strategy teams, the key implication is simple: timing and architecture choices made in 2026 will determine whether firms capture scalable share in the next growth phase.

Competitive landscape — focus areas and strategic postures

The competitive field is a mix of global platform leaders, specialist sensor makers, systems integrators, and industrial OEMs. Market concentration metrics show a market with several scale players but substantial opportunity for differentiated challengers: top firms account for meaningful share, yet fragmentation allows fast followers and niche specialists to prosper.

- Teledyne FLIR: Global scale and breadth. Teledyne FLIR leads with full‑stack capabilities—handheld cameras, cooled MWIR modules, automotive‑qualified modules and OEM system supply—and a vertically integrated approach that delivers large weekly volumes into automotive, defense, and professional markets. Their roadmap demonstrates how scale enables vertical integration as a competitive moat.

- Seek Thermal: Volume and cost engineering. Seek’s focus on compact, cost‑effective modules, and their move into next‑generation LWIR sensors, illustrate how component innovation enables new end markets (including price‑sensitive automotive and firefighting segments).

- InfraTec and Jenoptik: High‑performance and scientific markets. These suppliers concentrate on cooled arrays and high‑resolution thermography, addressing industrial NDT, scientific research, and automation use cases where resolution and stability are product differentiators.

- Exosens, Bullard, Dräger, 3M, Viper, Axis: Niche leadership and integration. These firms focus on long‑range counter‑drone systems, explosion‑proof firefighting cameras, industrial safety, process monitoring, and networked perimeter cameras respectively—each occupying domain‑specific value chains where integration, certification, and serviceability matter more than unit price.

Recent industry moves illustrate the strategic playbook in action: automotive qualification of thermal modules to functional safety standards, capacity expansions for cooled imagers to meet counter‑drone demand, and product introductions targeting system integrators. These moves are indicators of where competition will concentrate through 2026 and beyond.

Regulation, standards and procurement risk

Regulatory and standards compliance is an active determinant of procurement decisions. Automotive functional safety standards (e.g., ISO 26262) are already being applied to thermal modules intended for ADAS and automated vehicle systems. For buyers and specifiers this raises four tactical considerations:

- Qualification timelines: expecting automotive‑grade qualification to add months to supplier ramp plans.

- Supplier selection criteria: preferring vendors with documented safety processes and system‑level traceability.

- Warranty and liability frameworks: revising contractual terms to reflect higher assurance requirements for safety‑critical applications.

- Price vs. compliance tradeoffs: recognizing that higher compliance creates cost floors that affect margin modeling.

Additionally, public sector procurement studies demonstrate a broad range of product offerings for mission‑critical applications—underscoring variability in feature sets, ruggedization, and support models across the market.

Technology and supply‑chain signals to watch in 2026

Sensor architecture choices (cooled photon detectors vs. advanced uncooled arrays), pixel density, LWIR sensitivity, and onboard computing for analytic augmentation are where competitive differentiation will be built. Notable signals we track include:

- Detector resolution ceilings: manufacturers are shipping cameras with substantially higher pixel counts for thermography and automation applications—capabilities that enable new, quantitative use cases.

- Production capacity expansions: recent announcements of doubled output for cooled imagers are a leading indicator of where shortages can abate and where price pressure might emerge.

- Vertical integration: firms that control mechanical, optical and sensor subsystems can accelerate qualification cycles for OEMs, creating a procurement preference for integrated suppliers.

For supply‑chain teams, the immediate task is to map supplier capability to internal roadmaps—prioritizing partners that align on volume, qualification speed, and roadmap transparency.

What PW Consulting’s report delivers (practical contents)

Our full report is constructed as an operational toolkit for executives who must convert macro growth into executable plans. Key contents include:

- Comprehensive market sizing and validated demand models (historical 2020–2025 and firm forecasts 2026–2032), with scenario analysis to stress‑test investment cases.

- Supply‑chain mapping, supplier capability matrices, and critical‑path analyses for qualification and ramp.

- Technology deep dives—comparative performance of cooled vs uncooled architectures, LWIR advances, and system‑level integration considerations.

- Regulatory and standards playbooks (including automotive functional safety implications) and procurement‑grade checklists.

- Competitive benchmarking and deal‑flow watchlists with strategic assessments of leading suppliers.

- Commercial playbooks—go‑to‑market, channel strategies, pricing frameworks, and OEM integration templates.

- M&A and partnership frameworks identifying roll‑up vs bolt‑on archetypes and valuation sensitivities.

- Case studies and recommended 90/180/360 day implementation plans for R&D, sourcing, and sales teams.

Because our audience uses the report as an operational instrument, proprietary segmentation tables and granular revenue splits are retained in the full deliverable rather than summarized here; this intentional withholding ensures competitive confidentiality and allows subscribers to deploy the models directly within their corporate planning systems.

Actionable recommendations for 2026 (top five)

- Prioritize supplier audits for automotive and safety‑critical modules early in 2026 to secure qualification windows before next‑cycle program freezes.

- Adopt a two‑track sourcing strategy: a strategic anchor supplier with vertical integration plus a nimble secondary supplier for innovation risk and price competition.

- Invest in system‑level analytics and edge processing to extract differentiated value from thermal data, rather than competing solely on sensor price or resolution.

- Evaluate targeted M&A for niche cooled‑detector specialists or system integrators that accelerate route‑to‑market in defense and counter‑uncrewed domains.

- Design procurement contracts that include capacity and lead‑time protections given recent capacity expansions and the possibility of episodic demand spikes.

Where PW Consulting can help

Our advisory engagements combine the market models in the full report with hands‑on delivery: supplier due diligence, qualification acceleration programs, and M&A advisory specific to thermal imaging technologies and adjacent sensing stacks. Clients use our scenario models to stress test product roadmaps and to quantify value capture under alternate adoption curves.

To access the detailed segmentations, vendor scorecards, and the full financial models that underpin our conclusions, visit the PW Consulting report page. The public brief you are reading now is a strategic preview; the complete report contains the granular intelligence necessary to execute with confidence in 2026.

For briefings, enterprise licensing, or to commission a custom strategic module aligned to your product roadmap, contact PW Consulting’s Thermal Imaging practice. Our team is available to walk through the models and convert market momentum into concrete execution plans.

For detailed analysis of this topic, please visit the official page:Thermal Infrared Imagers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com