Expert Insights for Navigating the Thriving World of Online Casinos in Cambodia

Other |

2026-05-12 21:13:52

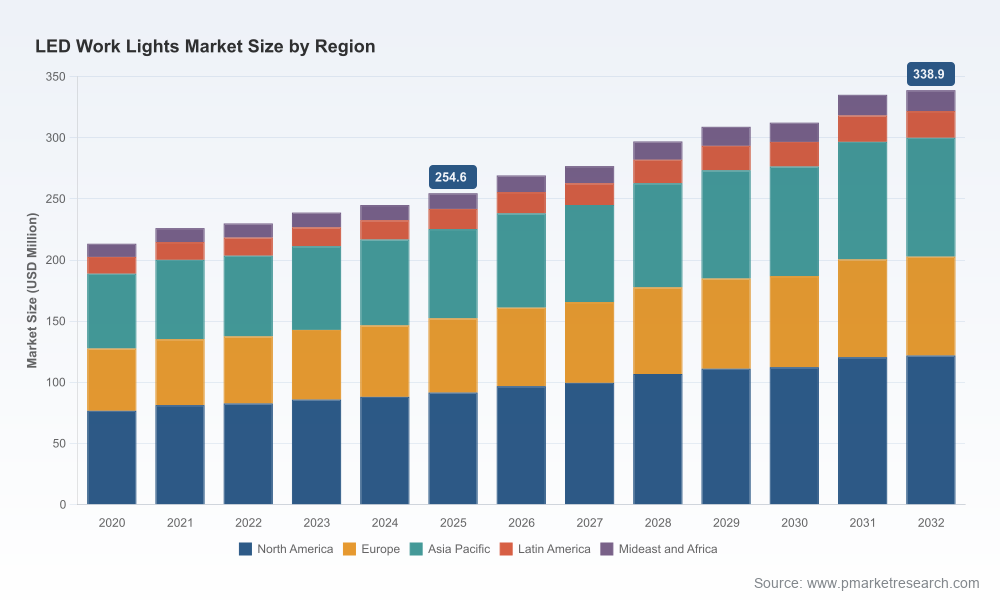

PW Consulting’s new LED Work Lights Market report (base year 2025, historical period 2020–2025, forecast 2026–2032) delivers a concise, decision-oriented view for executives planning capital, product, and go‑to‑market moves in 2026. The global LED work lights market has expanded steadily from USD 213.3 Million in 2020 to USD 254.6 Million in 2025. Our forecast horizon projects continued expansion at a compound annual growth rate (CAGR) of 4.1%, with the market reaching the mid‑to‑high hundreds of millions of USD by the end of the 2026–2032 forecast period.

LED Work Lights Market

This preview highlights the structural drivers shaping that growth, the competitive dynamics that matter for market share gains, and the practical priorities leadership teams should set now to capture the upside while protecting margins in an increasingly fragmented landscape (CR3 ~22.3%, CR5 ~28.5%). For those seeking the full segmentation tables, SKU‑level demand models, and our vendor scorecards, the complete report and downloadable financial models are available from PW Consulting’s report portal.

LED Work Lights Market

Stable base, targeted pockets of acceleration — The LED work lights segment is no longer a niche: steady year‑over‑year expansion and technology diffusion (battery platforms, high‑efficiency LEDs, ruggedization) mean that investments in product line optimization and channel expansion can be expected to compound over a multi‑year horizon rather than require a one‑time structural bet.

LED Work Lights Market

Platform economics and battery ecosystems — Cross‑selling opportunities tied to cordless battery ecosystems (proprietary & interoperable systems) are becoming a primary margin lever. A compact set of strategic moves in platform licensing, battery bundling, and aftermarket consumables can materially change lifetime value per commercial customer.

Fragmentation creates M&A and partnership windows — A relatively low concentration ratio indicates room for consolidation and bolt‑on acquisitions, particularly where specialized capabilities (explosion‑proof units, vehicle‑mounted lighting, advanced optics) and established channel relationships accelerate time to revenue.

Non‑price competition wins — Design for serviceability, battery safety certifications, lumens per watt optimization, and software‑enabled features (USB charging, beam control modes) are differentiators that buyers reward beyond initial price. OEMs that invest to raise perceived total cost of ownership will preserve margins as unit prices normalize.

Technology convergence: Higher‑efficiency LEDs, improved optics and lens control, and more energy‑dense rechargeable batteries are enabling lighter, higher‑output products that broaden addressable use cases (from confined‑space maintenance to mobile vehicle scene lighting).

Channel evolution: Traditional pro‑trade distributors remain important, but direct e‑commerce and fleet procurement portals are accelerating lead times and favor products with scalable aftermarket service and warranty programs.

Regulatory & safety drivers: Industry and workplace safety standards, plus certification requirements for hazardous environments, are creating a segmented premium tier where price sensitivity is lower but performance and compliance bar is higher.

Customer preference divergence: Professional trades and industrial buyers increasingly demand integrated systems (mounting, charging, multi‑voltage compatibility) while DIY and retail channels favor cost‑optimized plug‑and‑play solutions.

Proprietary market sizing model — end‑to‑end market size in USD (Million) by year, including a transparent methodology, sensitivity scenarios, and forecast drivers covering 2026–2032.

Scenario planning and downside buffers — three alternative growth trajectories with trigger conditions tied to raw material pricing, battery supply disruptions, and macro construction activity.

Product & price band analysis — SKU archetypes, implied margin bands, and profitability ladders that show where upgrades and cost takeouts move gross margin contribution.

Go‑to‑market playbooks — distributor vs. direct‑to‑fleet decision trees, digital channel KPIs, and a recommended 18‑month GTM sprint to test subscription and service models in pilot geographies.

Supply chain & sourcing playbook — risk maps for battery and LED component suppliers, alternative sourcing routes, and contract structures to stabilize costs without forfeiting flexibility.

Vendor scorecards & M&A shortlist — comparative performance benchmarking across engineering, channel reach, service infrastructure, and intellectual property; a prioritized list of bolt‑on acquisition candidates based on strategic fit.

Field case studies — three anonymized implementations showing realized payback timelines for fleet lighting upgrades, site safety retrofits, and rental model pilots.

Our analysis covers the incumbent professional tool brands, industrial lighting specialists, and newer entrants focused on rugged or vehicle‑mounted applications. A few strategic themes emerge from reviewing the leading players and recent product moves.

Platform incumbents (example: Milwaukee Tool, DeWalt, Makita) — These players leverage battery ecosystems and strong pro‑trade distribution to push higher‑price, higher‑margin cordless lighting solutions. Recent product introductions (e.g., Milwaukee’s M18 Service Area and Pivoting Area Lights with USB charging) illustrate the playbook: incremental product innovation that ties directly into a broader cordless tool ecosystem, increasing switching costs for professional buyers.

Generalist tool groups (example: Stanley Black & Decker) — Emphasize durability and system compatibility across multiple trades. Their strength is in account relationships and bundling opportunities in tool kits and rental channels.

Industrial & hazardous‑environment specialists (example: Larson Electronics, Banner Engineering) — Focus on performance and compliance (explosion‑proof, high‑lumen output, long runtime). Larson’s May 2025 release of an explosion‑proof LED drop light with a paint spray gun cover underlines how product differentiation tied to safety certifications unlocks access to specialized procurement budgets.

Lighting‑centric and niche innovators (example: Ledlenser, Streamlight, Baja Designs) — Typically drive innovation in optics, beam control, and ruggedization. These firms often serve as acquisition targets for tool platform owners seeking optical expertise and brand credibility in specialized segments.

Value players and China‑based manufacturers (example: Nilight) — Compete strongly on price and scale; attractive partners for white‑label or component supply, but require careful IP protection and quality assurance protocols if used for higher‑margin channel plays.

1. Optimize product portfolios around platform leverage: Prioritize SKUs that integrate with your battery and charging ecosystem. Where you lack a battery platform, evaluate strategic partnerships or licensing to accelerate market entry without a multi‑year battery R&D program.

2. Build a services overlay: Introduce extended warranties, swap/loaner programs for fleet customers, and bundled installation/maintenance services to turn transactional sales into recurring revenue.

3. Targeted premiumization: Invest selectively in certified and hazardous‑area offerings where procurement tolerates higher ASPs and margins. Certification competency (and associated documentation) is a barrier that commands price premium and protects against low‑cost encroachment.

4. Tighten supply chain resiliency: Lock in tier‑1 battery and LED suppliers with multi‑year agreements and volume discounts but retain optionality by qualifying secondary sources. Implement fast‑ramp clauses for high‑growth scenarios.

5. Pursue small, strategic acquisitions: Look for targets that add optical engineering, ruggedized enclosures, or certifications rather than large bolt‑ons—these accelerate capability rather than dilute focus. Our report includes a prioritized shortlist and acquisition valuation framework.

6. Pilot new commercial models: Test subscription and outcome‑based pricing in controlled customer segments (rental fleets, contractors with recurring site needs) to validate unit economics before scaling.

The public preview is intended to surface the most consequential strategic choices. The full report contains the granular evidence and tools you need to act immediately:

Complete regional and application segmentation tables and the underlying demand drivers (available only in the full report).

SKU‑level revenue and margin models in USD (Million), downloadable and editable for internal scenario testing.

Vendor and supplier due‑diligence templates, suggested integration roadmaps, and a playbook for three M&A archetypes (capability buy, channel buy, and supply buy).

Client‑ready slide sets and a one‑week executive workshop package to translate findings into a 100‑day plan.

The LED work lights market in 2026 will reward firms that combine product excellence with platform thinking, supply‑chain discipline, and commercially savvy service models. With a predictable, moderate growth rate and a business landscape defined by many capable players rather than a few dominant ones, the right mix of selective premiumization, partnership, and operational rigor can deliver outsized returns.

PW Consulting’s full market report gives procurement, product, and corporate development teams the models and playbooks to convert these strategic imperatives into measurable outcomes. For executives preparing capital allocation and M&A priorities for 2026, this is the tactical intelligence that shortens time to value.

For detailed analysis of this topic, please visit the official page:LED Work Lights Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com