Industrial Pump Control Panels: Strategic Imperatives for 2026 — A PW Consulting Preview

As companies finalize budgets and strategic roadmaps for 2026, the industrial pump control panels market is quietly shifting from a component-centric supply conversation to a systems-and-services battleground. PW Consulting’s latest market study — anchored on a 2025 base year and spanning historical performance from 2020–2025 with forecasts through 2026–2032 — identifies the high-impact choices executives must make this year to preserve margin, reduce operational risk, and capture growing aftermarket value.

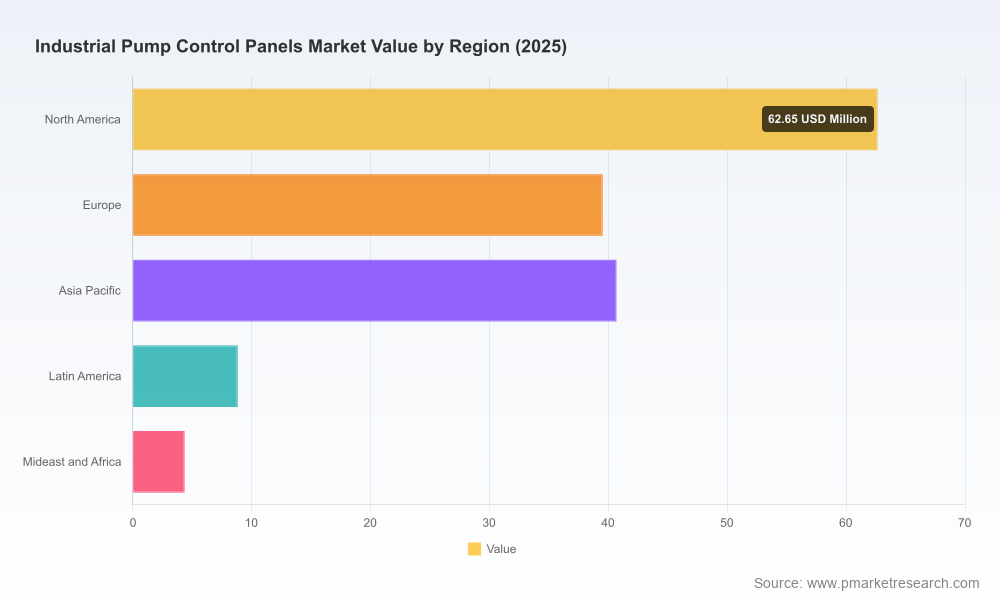

Industrial Pump Control Panels Market

Market at a Glance: Trajectory and What It Means for 2026 Decisions

The market for industrial pump control panels has grown steadily in recent years, expanding from USD 122.45 Million in 2020 to USD 156.05 Million in 2025. Our modeled outlook shows continued expansion at a compound annual growth rate (CAGR) of 5.21% across the 2026–2032 forecast horizon, reaching approximately USD 224.29 Million by 2032. In practical terms, this trajectory converts to steady demand for replacement, retrofit, and new-build control systems, with pockets of accelerated spending driven by digitalization and regulatory compliance.

Industrial Pump Control Panels Market

For procurement leaders, operations chiefs, and product strategists planning for 2026, the implication is clear: volume growth will not be uniform. Winning suppliers and OEMs will be those that combine reliability and regulatory compliance with higher-value capabilities — remote monitoring, smart-control logic, and service monetization — while insulating buyers from upstream commodity shocks.

Industrial Pump Control Panels Market

Why 2026 Is a Strategic Inflection Point

- Regulatory recalibration: The 2025 revision and re-affirmation of UL 508A as the active standard for industrial control panels have raised the bar for documentation, component selection, and factory acceptance testing. Buyers who move early to standardize procurement specifications around the updated UL 508A requirements will reduce retrofit risk and avoid costly field rework.

- Raw-material volatility: Prices for key inputs have proven volatile — copper experienced a notable spike in early 2026 before moderating, and steel prices remain elevated. These swings directly affect bill-of-material costs and supplier lead times; firms that establish hedging, alternative-spec options, or collaborative long-term agreements with vendors will maintain margin stability.

- Technology premium: Intelligent and networked control panels command a growing share of value, creating opportunities for suppliers to sell software-enabled maintenance contracts and analytics services that extend beyond hardware-only deals.

What Our Report Provides — Practical Tools for 2026 Execution

Our study is deliberately operational. It goes beyond market sizing to deliver instruments that procurement, engineering, and strategy teams can use in 2026:

- Supplier scorecards keyed to compliance, lead-time resilience, and integration capability.

- CapEx and Total Cost of Ownership templates that quantify the near-term premium for intelligent panels versus the lifecycle savings they deliver in downtime reduction and serviceability.

- Risk matrices that translate raw-material and regulatory exposures into procurement actions — e.g., index-linked contracts, dual-sourcing, and modular architecture choices that reduce rework if standards evolve.

- An adoption roadmap for digital retrofit programs that prioritizes locations by safety exposure, downtime cost, and connectivity readiness.

- M&A and partnership screening criteria for acquiring complementary control, telemetry, and service capabilities.

Competitive Landscape: Who Matters and What They Signal for Buyers

The supplier ecosystem remains relatively fragmented, with leading global electrification and automation players competing alongside specialized panel builders and OEM integrators. This diversity creates choice, but it also demands disciplined vendor selection. Key players to monitor in 2026 include:

- Schneider Electric — A leader with established pump-panel platforms for high-power applications and field-proven variants for irrigation and oil-field use. Schneider’s emphasis on packaged solutions with high horsepower ratings signals an orientation toward large-scale infrastructure and upstream users.

- Rockwell Automation — Through its Allen-Bradley lineup, Rockwell continues to serve customers who prioritize standardized motor-protection architectures and integration with proprietary control ecosystems. Their value proposition is strongest for users requiring deep PLC/HMI interoperability.

- Siemens — Siemens combines established NEMA-compliant panel families with broader industrial automation capabilities. Their approach benefits customers seeking integrated drive and control solutions across water, agriculture, and industrial segments.

- Eaton — Eaton’s emphasis on robust, weather-resistant enclosures and practical operator interfaces is tailored to irrigation and outdoor installations, where environmental durability is non-negotiable.

- ABB — ABB’s outdoor-rated full-voltage panels and protection packages address heavy-duty motor control needs typically found in municipal and industrial pumping stations.

- Specialized fabricators (See Water Inc., M-Tech Control, Metropolitan Industries, Optimum Controls, Xylem) — These firms differentiate on customization, UL-certified shop builds, and localized services. They are pivotal partners for municipalities, niche OEMs, and retrofit projects that demand tailored I/O, skid integration, or regulatory documentation.

For decision-makers, the competitive takeaway is twofold: (1) large global suppliers bring scale, product continuity, and cross-domain integration capabilities; (2) specialized builders provide speed, customization, and local-certification advantages. In 2026, hybrid sourcing models — combining a global platform with local customization and service agreements — will outperform single-source strategies in terms of total lifecycle cost and deployment speed.

Strategic Playbook for 2026 — Tactical Moves That Preserve Option Value

- Move from specs to outcomes: Write purchase orders around availability, mean-time-between-failure, and remote-diagnostic capability rather than purely on component make/models. This reduces vendor lock-in and aligns supplier incentives to uptime.

- Protect against commodity swings: Include material-escalation clauses and flexible BOM tolerances in contracts. Prioritize vendors willing to commit to phased pricing or inventory buffers for copper-intensive components.

- Modularize designs: Standardize mechanical and electrical modules to isolate future compliance or technology change to a replaceable sub-assembly, limiting system-level rework.

- Prioritize UL-ready documentation: Require UL 508A conformity packages at bid stage. Early verification avoids costly site acceptance delays and shortens commissioning cycles.

- Exploit service economics: Consider bundled hardware-plus-SaaS contracts where suppliers provide monitoring and analytics. These models can shift capital spend to predictable operating expense and unlock faster ROI from predictive maintenance.

- M&A and alliances: For suppliers and strategic buyers, 2026 is an attractive window to acquire integration shops and software stacks to leapfrog incumbent incumbents that focus on hardware only.

Scenario Planning: Two Plausible 2026 Paths

We recommend that executives stress-test plans against two near-term outcomes:

- Constrained-supply scenario: If metal prices rebound and lead times extend, expect margin compression for hardware-only suppliers and accelerated demand for retrofit services as operators prioritize uptime. Tactical response: dual-source critical components and lock in service agreements now.

- Digital-adoption acceleration: If infrastructure programs and utility funding push digital upgrades, intelligent panels and telemetry-enabled service packages will capture disproportionate share growth. Tactical response: prioritize pilot deployments in high-value assets and vendor partnerships that include analytics licensing.

KPIs and Procurement Triggers for 2026

Transform strategy into execution by monitoring a short list of actionable KPIs:

- Percentage of new purchases with UL 508A-conformant documentation required at PO issuance.

- Share of panel purchases bundled with remote monitoring or analytics services.

- Average supplier lead time for copper-intensive deliverables and the variance month over month.

- Total cost of ownership (TCO) differential between standard and intelligent panel options over an 8–10 year horizon.

Final Thought: Use 2026 to Lock in Optionality

As the market expands from USD 156.05 Million in 2025 toward our forecasted USD 224.29 Million by 2032 at a 5.21% CAGR, the strategic benefit in 2026 will accrue to organizations that balance near-term resiliency with long-term optionality. Those who treat control panels not as commoditized enclosures but as platforms for uptime, analytics, and service delivery will convert modest market growth into outsized margin and customer-locking revenue streams.

Learn More

PW Consulting’s full Industrial Pump Control Panels Market report contains the detailed segmentation, supplier scorecards, procurement templates, and scenario models referenced in this preview. For access to the complete dataset, supplier benchmarking tables, and downloadable tools to apply these insights directly to 2026 planning, visit our report page or contact your PW Consulting account lead.

For detailed analysis of this topic, please visit the official page:Industrial Pump Control Panels Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com