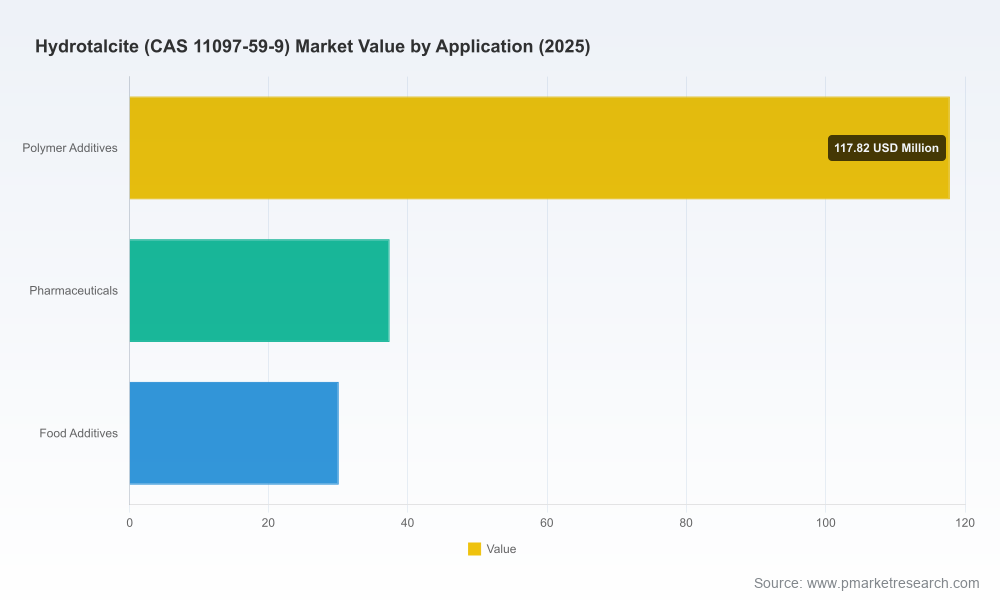

PW Consulting: Hydrotalcite (CAS 11097-59-9) Market Poised to Reach USD 273.72 Million by 2032, Fueled by PVC Stabilizers Demand

Other |

2026-06-29 17:30:46

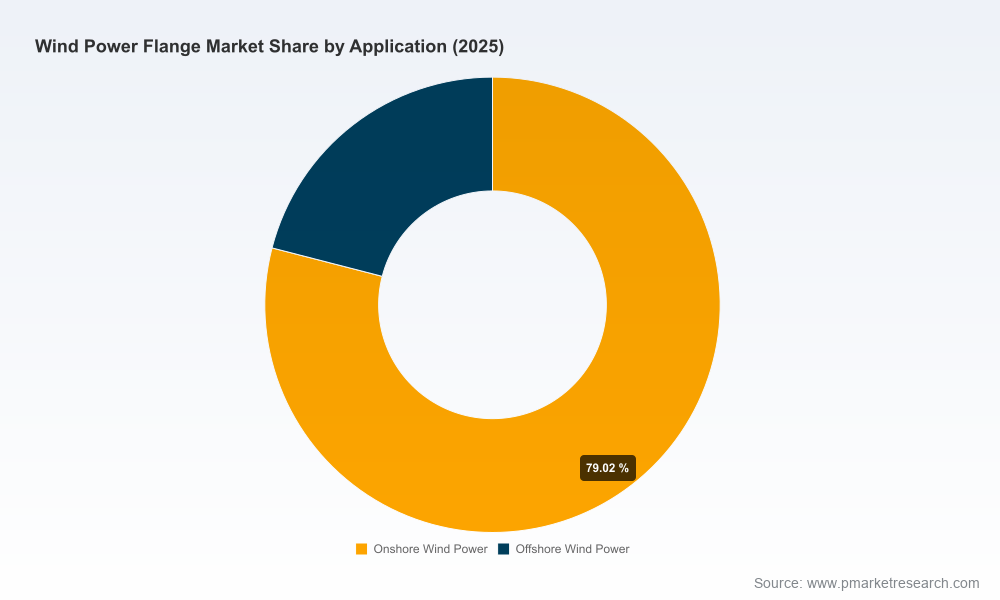

PW Consulting’s latest Wind Power Flange Market report (base year 2025; historical 2020–2025; forecast 2026–2032) crystallizes the near-term commercial landscape for a component class that is small in count but very large in system impact. The market reached approximately USD 703.1 Million in 2025 and — driven by turbine scaling, accelerating offshore projects, and standards-driven specification upgrades — is forecast to expand at a 7.35% CAGR to roughly USD 1,162.9 Million by 2032. For executive teams preparing 2026 capital allocation, procurement strategies, or M&A playbooks, this analysis distills the tactical implications that flow from those headline dynamics while preserving the detailed segment-level intelligence available in the full report.

Wind Power Flange Market

Flanges are structural and assembly-critical components in tower, blade, gearbox and generator interfaces. As turbines grow in scale — taller towers, longer blades, and deeper substructures for offshore applications — flange specifications shift from commoditized plates to engineered forgings and rolled rings that must meet fatigue, corrosion and welding standards. That evolution increases the technical and commercial value of flange suppliers, making them strategic vendors rather than simple parts vendors. The result is a market where material grade selection, fabrication method, and supplier certification directly affect project CAPEX, operational risk and delivery schedules.

Wind Power Flange Market

Structural growth trend: After steady expansion through 2020–2025, total market value and modeled demand elasticity indicate a multi-year growth runway. The CAGR through 2032 underscores predictable demand but also highlights pockets of rapid demand acceleration tied to offshore rollouts and replacement cycles.

Wind Power Flange Market

Supplier concentration: The market displays material concentration at the top end — the largest three players account for close to half of the market, while the top five approach three-quarters of market share. That degree of concentration creates bargaining asymmetries, but also clearer targets for strategic partnerships and portfolio investments.

Offshore growth and technical uplift: Offshore projects are imposing stricter fatigue, corrosion and welding requirements. Regulatory frameworks and buyer specifications are pushing greater use of specialty alloy steels and higher-grade fabrication processes.

Materials and process innovation: Seamless ring-rolling and large-scale forging presses reduce waste and deliver mechanical properties needed for large-diameter flanges. Our analysis indicates process choices materially affect cost-per-unit and yield — a competitive lever for suppliers that have invested in advanced rolling or high-tonnage forging capability.

Certification and compliance overhead: Procurement policies in several major markets now embed local-content and welding certification requirements. This raises the bar for supplier qualification and increases the value of certified regional partners for OEMs and developers.

Raw-material premium dynamics: Specialty alloys required for offshore exposure attract meaningful premiums relative to standard grades — a factor that should feed directly into contract structuring and indexation clauses in 2026 supply agreements.

We profile established forgings specialists, vertically integrated component suppliers, and regionally focused fabricators — each with distinct strategic postures that matter for partnership, procurement and M&A decisions.

Iraeta Energy Equipment Co., Ltd. — A manufacturer with multi-country footprint and growing offshore capability. Recent capacity investments include commissioning of a high-tonnage forging press to serve large-diameter offshore flanges, reflecting a strategic push into high-growth substructures.

Jiangyin Hengrun Ring Forging Co., Ltd. — A specialist in tower flanges and ring forgings for utility-scale turbines. Its scale and specialization make it a go-to for high-volume onshore programs.

Shanxi Tianbao Group Co., Ltd. — Focused on forged tower components, positioning on reliability and vertical integration.

Taewoong Co., Ltd. — A supplier of large-diameter flanges that has recently executed a strategic JV in Southeast Asia to capture regional onshore demand — a telling example of local-partner strategies to access lower-cost production and meet regional procurement rules.

Flanschenwerk Thal GmbH and Euskal Forging, S.A. — European makers with expertise in custom, non-standard and very large flanges; their capabilities map closely to offshore substructure requirements.

CHW Forge and CAB Worldwide — Regional players/partners offering capacity depth, local servicing and distribution channel access that matter to OEMs optimizing manufacturing footprints.

Collectively, the competitive set demonstrates two strategic realities: first, capability leadership (large presses, ring-rolling, certified welding) is becoming a primary differentiator; second, geographic and regulatory access — achieved through JVs, local investments or distributor networks — is an increasingly decisive factor in supplier selection.

Localized procurement rules are proliferating in key markets, adding certification and supplier-qualification requirements that affect lead times and vendor pools.

Offshore regulatory regimes in major jurisdictions are tightening quality standards for large-diameter components, making early supplier qualification and pre-certification a project-critical path item.

ISO and welding standards — including rising demand for ISO 3834 compliance in certain tenders — are shifting supplier selection from cost-only to capability-and-compliance assessments.

Recalibrate supplier scorecards to weight certification and process capability more heavily than unit price. Include ring-rolling experience, post-weld heat treatment capability, and proven fatigue testing among pass/fail criteria.

Use modular sourcing: split volumes between a certified premium supplier for high-spec units (e.g., large offshore flanges) and high-volume regional producers for standard onshore parts to balance cost and technical risk.

Embed material-price indexation and alloy-premium clauses in multi-year contracts to hedge volatility in specialty steels.

Pursue strategic JVs or capacity reservations in regions with local-content rules. Recent industry moves show faster market access and lower qualification friction when global suppliers partner with regional fabricators.

Accelerate supplier pre-qualification and audit programs now to avoid downstream schedule risk: compliance-driven lead times and capacity constraints are likely to bottleneck projects kicking off mid-2026 and beyond.

This report is designed as an operational playbook, not an academic exercise. Key deliverables that executives will find immediately actionable include:

Dynamic forecast models (2026–2032) with scenario toggles for offshore build-rate sensitivity, technology adoption curves, and material-price shocks — ready to drop into capital-planning workflows.

Supplier scorecards and a validated shortlist of strategic- and tactical-tier vendors, including capability matrices and audit checklists for welding and non-destructive testing qualifications.

Procurement playbooks: model RFP language, indexation templates for alloy premiums, and contract clauses designed to mitigate lead-time and quality risk.

Supply-chain risk maps identifying single-source exposures, capacity choke points, and regulatory compliance hotspots across major tendering jurisdictions.

M&A and partnership screening tools: quick filters that identify targets with desirable technical assets (e.g., ring-rolling lines, large-tonnage presses) and attractive margin profiles.

Capability investment: A supplier that invested in a higher-tonnage press and ring-rolling lines moved from a regional supplier role to a certified strategic partner for offshore substructures. The capability shift enabled premium pricing and longer-term offtake contracts.

Partnership to meet procurement rules: A mid-sized OEM materially shortened qualification timelines in Southeast Asia by executing a JV with a local forging partner — a repeatable model for firms seeking to scale quickly under local content regimes.

High-level figures and qualitative trends are necessary but not sufficient for precise procurement or investment commitments. The full PW Consulting report provides granular segment-level forecasts, region-by-region demand curves, application splits, and company-level share tables — all of which are necessary inputs for contract size decisions, plant-capacity timing, and M&A valuation work. To preserve the commercial value of that—and to respect clients who rely on PW Consulting for proprietary insight—we present here the strategic signal and the operational implications without reproducing detailed tables, percent shares or price curves. Those data tables and downloadable models are available in the full report package.

As the market scales, flange suppliers are transitioning from commodity vendors to strategic enablers of turbine reliability and project delivery. For 2026 planning cycles, prioritize capability and certification over lowest-cost offers, lock in alloy-price protection where feasible, and consider staged partnerships or capacity reservations in regulated or fast-growing regions. Use the period before mid-2026 to complete supplier requalification and to shore up sourcing strategies; projects that delay supplier certification now will face stretch on timelines and margin erosion later.

PW Consulting’s Wind Power Flange Market report includes the full segmented forecast, detailed company profiles, transaction-ready diligence templates, and the Excel models referenced in this brief. For procurement leaders, engineers and corporate strategists who require the complete dataset and executable tools, please visit the PW Consulting reports portal to request the complete report and supporting materials.

For detailed analysis of this topic, please visit the official page:Wind Power Flange Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com