Why Businesses Are Investing in SAP SuccessFactors Services in India

Technology |

2026-06-23 09:12:56

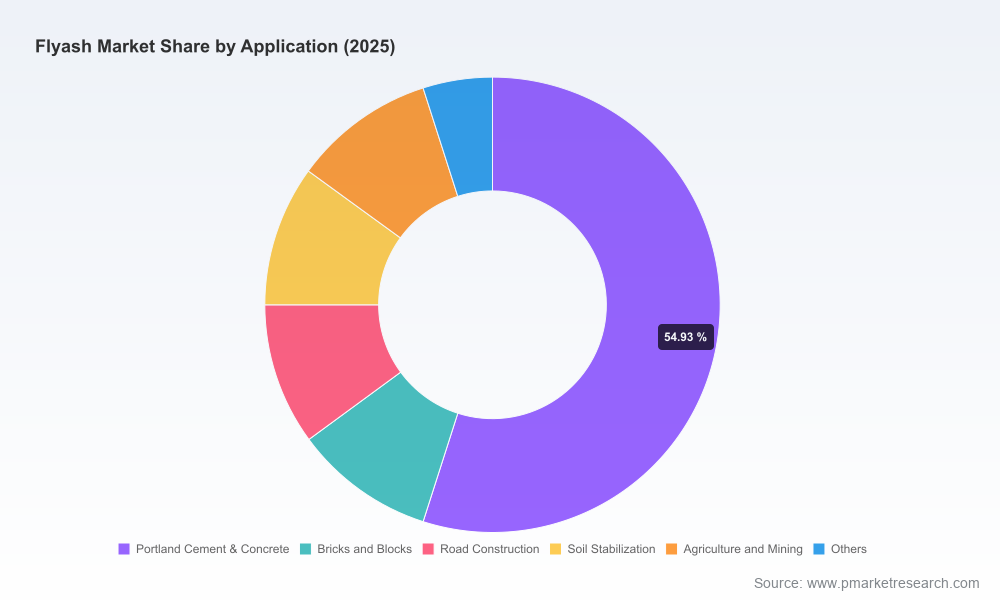

PW Consulting’s latest Flyash Market report (base year 2025) delivers a pragmatic, decision-ready assessment tailored for executives, procurement leads, and strategic investors facing a fast-evolving supply-and-demand landscape in 2026. The global flyash market expanded from an estimated USD 11.0 Billion in 2020 to USD 15.2 Billion in 2025 and, under the baseline scenario embedded in our analysis, is projected to grow at a 6.6% CAGR to reach approximately USD 23.8 Billion by 2032. Market concentration is meaningful — the top three players control just over half of the market, while the top five approach two-thirds — a fact that materially shapes competitive strategy, M&A opportunity and supply security.

Flyash Market

Strategic procurement and contracting: With supply tightening in several producing regions and price signals already emerging, procurement teams must revisit contracting cadence, hedging approaches and contingency inventories.

Flyash Market

Capital allocation and portfolio strategy: Manufacturers and materials investors need forward-looking scenarios to prioritize investments in beneficiation, low-carbon product lines, or logistics infrastructure that protect margins as markets shift.

Flyash Market

Regulatory and compliance planning: Evolving regulation alters reuse economics and permitting risk; near-term policy shifts can change the addressable market for recycled ash and low-carbon cement substitutes.

Several converging forces are defining a new structural dynamic for flyash markets:

Supply-side attrition of coal generation in major markets has constrained fresh flyash availability in key producing geographies. Reduced output, plant retirements, and shifts in fuel mix have created a widening supply-demand gap in markets that historically relied on steady ash streams.

Regulatory toggles are ambiguous and regionally divergent. Recent proposals in the U.S. would lower barriers to reuse by relaxing certain groundwater-monitoring requirements, potentially unlocking higher utilization rates for beneficiated and landfill-sourced ash. At the same time, some jurisdictions maintain strict ash-utilization mandates that incentivize near-term demand for ash-derived materials.

End-market demand is being supported by two secular trends: infrastructure investment cycles and decarbonization-driven substitution in cement and concrete production. The latter is creating premiumization opportunities for low-carbon or beneficiated flyash products.

Price volatility has already surfaced in response to regional scarcity, with observable disparities across major producing countries. These microprice signals are driving supplier diversification and localized beneficiation investments.

The flyash marketplace today is a mixture of legacy utilities, specialist processors and global cement majors. PW Consulting’s assessment of incumbent capabilities shows three strategic archetypes:

Resource-centric leaders: Large utility-affiliated suppliers continue to leverage their feedstock ownership and logistics scale to supply industrial customers and infrastructure projects. These players are advantaged in feedstock access but face reputational and regulatory complexity when expanding reuse channels.

Value-added processors and niche specialists: Dedicated beneficiation and SCM (supplementary cementitious material) specialists focus on quality control, consistency and certifications required by concrete and precast producers. These firms capture a quality premium and are natural partners for construction material OEMs seeking low-carbon inputs.

Integrated building-materials companies: Cement and concrete multinationals are folding flyash into broader low-carbon portfolios, bundling product offerings and leveraging procurement scale to secure feedstocks and lock in forward pricing.

Representative company assessments in our report include:

Eco Material Technologies (US) — A dominant name in North America with long-standing feedstock access and market share leadership. Their scale provides defensive supply security for large industrial customers and makes them an acquirer of choice for complementary logistics or beneficiation capabilities.

Charah Solutions Inc. (US) — Operates a multi-source network serving diverse applications including ready-mix and remediation. Their distributed model is well-suited to capture demand close to end-use sites and to offer logistical flexibility.

Holcim Group (Switzerland) — Integrating low-carbon flyash products into a broader ECO materials portfolio, global cement groups can capture margin both upstream (feedstock beneficiation) and downstream (low-carbon cement and precast offerings).

NTPC and BALCO (India) — Large utility and alumina-linked producers who have been central to India’s high utilization rates. Their ability to marshal national policy and deliver scale makes them pivotal to domestic supply security.

Titan America LLC (US) — Cement-focused suppliers that utilize flyash as part of their cementitious mix, highlighting the strategic importance of long-term offtake and integrated sourcing.

Utilization momentum: Industry reporting indicates rising recycling rates and increasing concrete use of flyash in several markets, underscoring both the environmental narrative and real demand lift for processed ash.

Large-scale national programs: Some governments have achieved very high utilization numbers through combination of mandates, incentives and investments in beneficiation — a model private players should monitor as it materially alters regional supply-demand balances.

Price divergences: Observable price spreads across producing regions have already prompted re-routing of traded material where logistics economics permit and are accelerating regional beneficiation projects to produce higher-value SCM products.

For procurement and supply-chain leaders: Reassess contracts with an emphasis on duration diversity (short and long forms), include quality and liability clauses for reused ash, and model inventory buffers under multiple stress scenarios. Develop alternative sourcing corridors and strategic storage nodes near high-demand clusters.

For commercial and product teams: Prioritize low-carbon, beneficiated flyash products and pursue co-development with downstream concrete and precast customers. Use spot markets tactically but secure offtake for core volumes.

For corporate development and investors: Evaluate bolt-on acquisitions that add beneficiation, drying and logistics capabilities. Given the market concentration dynamics, targeted M&A can rapidly increase market access and address quality constraints that limit premium pricing.

For regulatory and sustainability teams: Monitor proposed regulatory changes closely. Where regulation lowers barriers to reuse, accelerate product approvals; where stricter controls are possible, increase remediation and traceability capabilities to reduce permitting risk.

PW Consulting equips clients with three actionable scenarios (conservative, baseline and accelerated-adoption) that translate macro assumptions into P&L, working-capital and balance-sheet outcomes across a range of operational archetypes. Each scenario includes a pragmatic playbook — listing prioritized initiatives by time horizon and estimated ROI — so teams can make 2026 capital and sourcing decisions with clarity.

The report is designed as an operational toolkit, not just a narrative. Highlights include:

Market-sizing and trend dashboards (historical and forecast through 2032), including scenario-adjustable drivers and sensitivity levers.

Supply-chain stress tests and logistics-cost overlays to model delivered cost under various fuel and freight scenarios.

Regulatory impact maps and a compliance-action checklist for major producing and consuming jurisdictions.

Company capability profiles and a tactical M&A playbook that identifies candidate capability gaps and integration risks.

Commercial contracting templates and a supplier scorecard framework to operationalize procurement strategy.

Risk matrix with mitigation playbooks covering quality variability, permitting, reputational exposures and pricing shocks.

90 days: Run a supplier-vulnerability heatmap; prioritize critical contracts for renegotiation; initiate pilot testing for beneficiated low-carbon ash in key accounts.

180 days: Lock in diversified logistics routes, finalize offtake agreements with tier-1 customers, and commence at least one capex project for drying/beneficiation where economics are compelling.

360 days: Execute strategic M&A or joint ventures to secure feedstock-to-product integration, and roll out a certified low-carbon SCM product across multiple markets.

This release shares the high-level market trajectory, structural dynamics and strategic implications. To preserve the tactical value of our modeling and to protect granular commercial data, the full report includes detailed regional and application-level splits, price curves, supplier-by-supplier production profiles, and downloadable scenario models — all accessible via PW Consulting’s report portal.

For firms exposed to cement, concrete and broader construction-materials value chains, 2026 is an inflection year: supply constraints, regulatory shifts and decarbonization demand are intersecting to create both risk and premiumization opportunities. PW Consulting’s Flyash Market report translates those macro forces into concrete actions — from procurement playbooks to M&A blueprints — enabling decision-makers to prioritize investments that protect margins and capture upside as the market scales toward our 2032 baseline projection.

To obtain the full dataset, regional and application breakdowns, proprietary pricing models and the complete operational toolkit, please visit PW Consulting’s report page and download the full Flyash Market report.

For detailed analysis of this topic, please visit the official page:Flyash Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com