Pharmaceutical Ethanol Market 2026 Outlook: Strategic Signals for Boardrooms and Procurement Teams

PW Consulting today releases a strategic preview of our upcoming market research report on the Pharmaceutical Ethanol market — a data-driven guide designed to inform enterprise decisions as companies set priorities for 2026. The full report (base year 2025; historical window 2020–2025; forecast 2026–2032) combines granular market modelling, supplier intelligence, regulatory mapping and executable playbooks so that C-suite leaders, procurement heads and investors can act with conviction as the sector enters its next growth chapter.

Pharmaceutical Ethanol Market

Why 2026 matters: the state of play in one paragraph

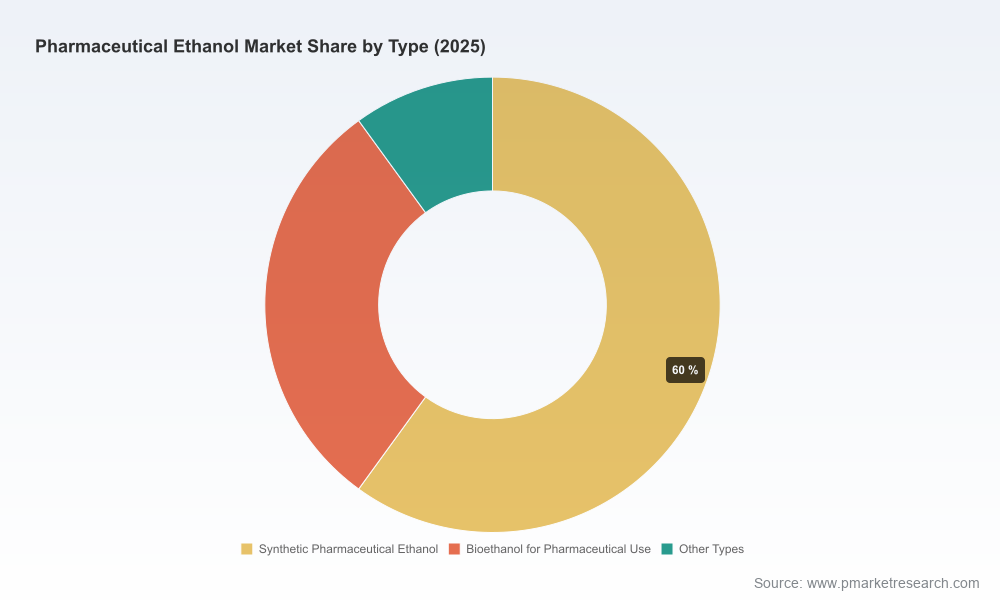

Pharmaceutical-grade ethanol has moved from a commodity adjunct to a strategic raw material. After steady expansion through the early 2020s, the market reached a measured size of USD 1.10 Million (revenue unit: Million) in 2025 and is modelled to grow at a compound annual growth rate (CAGR) of 6.5% across our 2026–2032 forecast horizon, reaching an estimated USD 1.73 Million by 2032. That growth is being driven by converging forces: renewed investments in sterile drug manufacture, persistent demand for sanitization and biopharma process solvents, regional industrial policy shifts, and a growing bifurcation between bio-based and synthetic supply chains. For companies planning capital allocation, sourcing strategies or M&A in 2026, these dynamics create both risk and opportunity windows that close quickly unless anticipated.

Pharmaceutical Ethanol Market

What the report delivers — practical, transaction-ready intelligence

- Market sizing & forecast: a transparent reconciliation of demand drivers and supply-side throughput, anchored to our audited 2020–2025 historical series and projecting to 2032.

- Supply chain and cost curve analysis: plant-level capacity overlays, marginal cost benchmarking and a short-list of supply-risk corridors that materially affect availability and price volatility.

- Regulatory and quality matrix: comparative requirements across major pharmacopeias, an audit-ready checklist for GMP-compliant procurement, and scenarios for regulatory tightening that matter to 2026 budgets.

- Buyer playbook: contract structures (term, indexation, quality specs), inventory sizing heuristics, and hedging approaches tailored to pharma-grade ethanol.

- M&A and partnership radar: target typologies, valuation sensitivities and due-diligence templates for strategic acquisition or JV decisions.

- Scenario modelling: three near-term demand-supply cases (baseline, accelerated adoption, and constrained supply) with decision trees for CAPEX and sourcing choices through 2032.

- Supplier intelligence: profiles, operational footprints and capability assessments of the leading producers and emerging entrants, with recommended engagement strategies.

Competitive landscape: how top players are positioning for 2026

The Pharmaceutical Ethanol market is moderately concentrated; our analysis indicates the top three suppliers control roughly half the market, with five players approaching 60% combined share. That concentration profile signals an environment where strategic relationships and logistics excellence can confer meaningful advantages — but not one where single-source dominance eliminates competition. Key corporate actors illustrate the range of strategies we see:

Pharmaceutical Ethanol Market

- Greenfield Global Inc. (Toronto, Canada) — A vertically integrated producer with dedicated high-purity distilleries and pharmaceutical packaging capability. Recent activity: in September 2025 Greenfield launched a UK distribution hub to hold local inventory and shorten lead times for pharmaceutical and biotech customers. For 2026, this move highlights a playbook worth watching: de-risking delivery through regional inventory and service-led differentiation rather than price alone.

- Archer Daniels Midland Company (ADM) (Chicago, USA) — A global ingredient specialist with established capabilities to supply USP-grade ethanol refined to pharmacopoeial standards. ADM’s comparative advantage lies in scale, integration with feedstock channels and long-standing customer contracts — factors that influence negotiation dynamics for large-volume purchasers.

- Godavari Biorefineries Limited (Hyderabad, India) — A regionally significant manufacturer tapping grain-based distillation capacity. Notable development: commissioning of a 200 KLPD grain-based distillery expected in January 2026 to raise production including pharmaceutical grades. This underscores the ongoing capacity additions in Asia that buyers must factor into sourcing and price outlooks.

- United Beta Industries (Saudi Arabia) — A domestically owned producer focused on near-anhydrous high-purity ethanol compliant with Ph.Eur. standards, positioning itself for both regional medical and export markets. Its emergence points to the broader theme of state-aligned industrial strategies reshaping geographic supply balances.

Strategic implications for 2026 decision-makers

Based on the report’s integrated models and scenario workstreams, we highlight five immediate decisions boards and procurement teams should prioritize in Q1–Q2 2026:

- Recalibrate sourcing risk tolerance: with growth accelerating at ~6.5% CAGR into the next decade, firms should stress-test supplier concentration, cross-border logistics exposure and single-site dependencies. Build alternate-supply clauses and inventory buffers into contracts where product continuity is mission-critical.

- Differentiate procurement by application: ethanol for sterile fill-finish and active pharmaceutical processes carries higher quality and traceability premiums than formulations for sanitizers. Adopt differentiated sourcing tracks — one for critical-drug-grade material and another for lower-risk sanitization requirements — to optimize cost without compromising compliance.

- Pursue supply-side partnerships over spot buying: recent hub launches and new distillery commissions show suppliers investing in service and capacity. Long-term offtake agreements with performance SLAs can secure priority allocation during supply shocks while offering producers demand visibility to justify further capacity expansion.

- Embed lifecycle and sustainability criteria into contracts: bioethanol availability and decarbonization commitments will increasingly factor into procurement decisions. Even where synthetic ethanol remains cost-competitive, ESG-related procurement mandates and customer expectations will require traceability and a CO2-footprint premium assessment.

- Align capital planning with scenario thresholds: for manufacturing and biotech firms contemplating captive distillation or minority investments in upstream capacity, the report provides break-even analysis under multiple demand-supply scenarios; use these thresholds to trigger investment committees rather than relying on single-point forecasts.

Operational playbook for procurement and operations leaders

Translating high-level strategy into 2026 operational steps is a focus of our report. Key operational actions we recommend implementing within the next 6–12 months include:

- Establish a contract review window that re-evaluates indexation clauses, QC acceptance criteria and force majeure definitions to reflect post-pandemic logistics realities.

- Create a supplier scorecard that weights quality, delivery performance, regulatory compliance and regional resilience — and integrate it into quarterly sourcing reviews.

- Run a rapid supplier audit of alternate regional suppliers (including those in new-capacity corridors) to qualify a second-tier list for rapid qualification testing.

- Implement a short-term inventory policy calibrated to the company’s mix of critical vs. non-critical ethanol use cases, balancing working capital with service continuity.

What executives will miss if they don't read the full report

Our preview intentionally outlines the strategic contours without publishing the proprietary segment analyses, regional flow matrices and price-elasticity tables that make operational change possible. The full report contains:

- Granular supplier scorecards and contact-level engagement recommendations;

- Plant-level capacity maps and marginal cost curves that reveal the most likely sources of future supply tightness;

- Proprietary scenarios linking feedstock price shocks to downstream pharmaceutical cost impacts;

- Template contractual language and a procurement playbook tuned to pharmaceutical quality and compliance needs.

These deliverables are designed to move teams from strategic intent to executable sourcing and investment decisions during 2026 — precisely when timing matters most.

Risk outlook and regulatory watch for 2026

Risk remains asymmetric: localized regulatory changes, feedstock constraints and bottlenecks in specialty packaging or transport could tighten supply rapidly. At the same time, capacity additions — including the 2026 and later facilities we have modelled — will alleviate pressure in base cases but will not uniformly substitute high-purity, pharmacopeial-grade volumes without targeted investment in purification and QA processes. Regulatory alignment across USP, Ph.Eur. and other standards, plus an emerging emphasis on traceability and origin declarations, will require procurement and compliance teams to upgrade specifications and testing regimes in the coming 12 months.

How PW Consulting can help you act in 2026

PW Consulting’s dedicated Pharmaceutical Ethanol report is built for decision-makers who need both the strategic view and the operational instruments to act now. Whether you are a buyer securing supply, an investor assessing capacity plays, or an industrial firm contemplating vertical integration, the report’s blend of market modelling, supplier intelligence and a procurement playbook was crafted to shorten the path from insight to action.

To access the full set of models, supplier dossiers, scenario workbooks and contract templates referenced in this preview, please visit our report page or contact our industry practice. In a market growing at a steady CAGR of 6.5% and transitioning through discrete supply and regulatory inflection points, 2026 is the year where proactive strategy translates into durable competitive advantage — and timely intelligence will separate leaders from laggards.

For detailed analysis of this topic, please visit the official page:Pharmaceutical Ethanol Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com