Clinical Reference Laboratory Services Market: Strategic Intelligence for 2026 Decision-Making

Executive summary

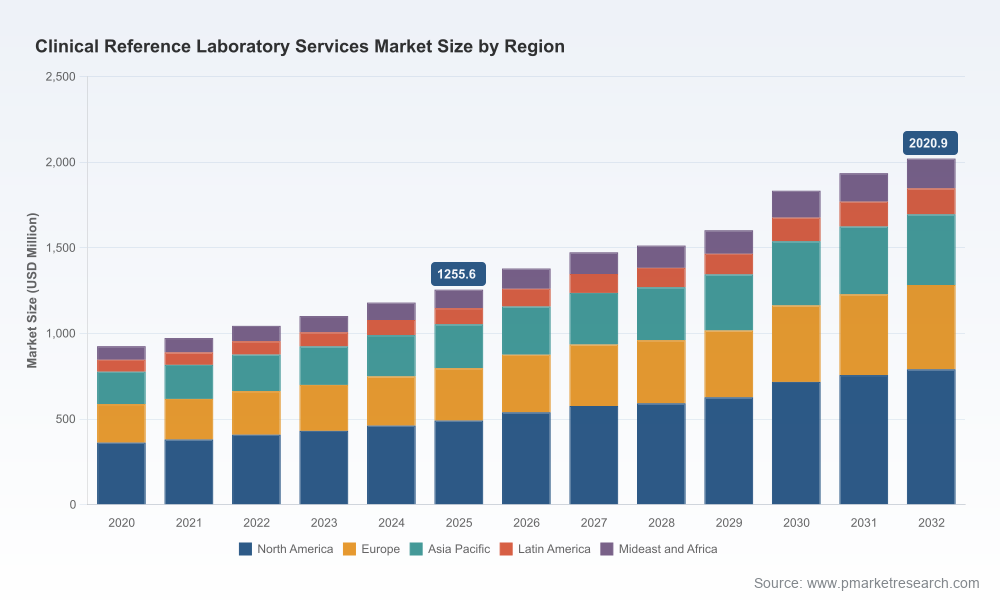

As healthcare providers, diagnostics companies, and investors position for the next wave of clinical innovation, our latest market research — anchored on a 2025 base year and projecting through 2032 — delivers the strategic intelligence required to make confident decisions in 2026. The Clinical Reference Laboratory Services market is on a sustained growth trajectory, characterized by a mid-single-digit compound annual growth rate (CAGR) of 7.25% and an evident shift in provider and payer models. From a historical industry value under a billion dollars in 2020, the market expands into a multi-billion-dollar opportunity by the end of the forecast window, reflecting rising demand for molecular and specialty diagnostics, cross-border consolidation, and digital care integration.

Clinical Reference Laboratory Services Market

Why this report matters to 2026 planning

- Actionable foresight for capital allocation. The report translates high-level growth projections into decision-ready scenarios for capacity investments, M&A prioritization, and platform rollouts — enabling CFOs and corporate development teams to align spend with anticipated service mix and reimbursement trends.

- Operational roadmaps for lab leaders. Lab directors and operations executives will find practical playbooks for workforce optimization, automation adoption, quality-control scaling, and supply-chain resilience that are tailored to the unique throughput and regulatory constraints of reference testing.

- Commercial strategies for market entry and expansion. Commercial and product teams gain prioritized go-to-market pathways and buyer-persona guidance that reduce time-to-adoption for novel assays and diagnostics services, particularly where telehealth and remote specimen collection are reshaping engagement models.

- Risk-adjusted scenarios for payers and providers. The analysis includes reimbursement sensitivity testing and regulatory-impact assessments so health systems and payers can model short- and medium-term cost implications of outsourcing, vertical integration, or insourcing specialized panels.

What the report contains — practical, deployable content

- Market sizing and scenario models (historical 2020–2025 calibration, forecast 2026–2032), with base-case, accelerated-adoption, and downside scenarios calibrated to changes in reimbursement, regulation, and technology adoption.

- Operational playbooks for automation, staffing, turnaround time (TAT) optimization, and quality assurance — including KPI templates and implementation milestones suitable for 12–36 month programs.

- Competitive benchmarking and vendor due diligence frameworks for acquisition screening, partnership structuring, and joint development agreements.

- Commercial frameworks: buyer personas, channel design for direct-to-patient and institutional customers, pricing-impact matrices, and sample negotiation playbooks for contracts with health systems and payers.

- Regulatory and reimbursement impact maps that translate policy shifts into financial and operational sensitivities for labs of different scale.

- Use-case deep dives on high-growth diagnostics (e.g., molecular and specialty testing), including lab-capacity models and cost-per-test sensitivity analyses to guide capex planning.

Market dynamics shaping 2026 choices

- Steady market expansion with nuanced drivers. Historical growth from 2020 through 2025 demonstrates system-wide uptake in reference diagnostics. Projected growth through 2032 is supported by technological advances, portfolio expansion of molecular and personalized diagnostics, and broader clinical adoption pathways.

- Regulatory and certification pressure. National certification lists and oversight continue to influence network design and transactional risk. HHS certification and related public registers remain a gating factor for certain service lines and federal contracts.

- Reimbursement volatility as a strategic variable. Reimbursement policy remains a principal determinant of pricing strategy and service viability. Our report includes sensitivity testing showing how modest adjustments in reimbursement can materially affect unit economics for high-cost specialty assays.

- Labor and automation. Persistent shortages of skilled laboratory personnel are accelerating automation investments. Labs that balance automated pre-analytic and analytic workflows with targeted human expertise will gain measurable improvements in throughput and error reduction.

- AI and digital enablement. The adoption of AI in diagnostics — both for analytical interpretation and operational optimization — is a strategic inflection point. Early adopters are realizing reductions in TAT and increased interpretive depth, creating a competitive delta for advanced reference providers.

- Supply-chain and outsourcing strategies. Outsourcing of specialized testing remains a recommended resilience strategy in public health system planning; contract design that secures reagent and consumable continuity is critical in multi-year procurement negotiations.

Competitive landscape — positioning the leaders

The Clinical Reference Laboratory Services market displays moderate vendor concentration, with the top three participants accounting for a significant yet non-dominant share and the top five collectively representing a plurality of market activity. This structure creates attractive windows for both national incumbents and regional specialists.

Clinical Reference Laboratory Services Market

- Clinical Reference Laboratory, Inc. (Lenexa, KS) — A large private laboratory with diversified services spanning toxicology, workplace testing, molecular diagnostics, and corporate wellness. Its breadth in occupational testing and private-market channels offers partners rapid access to employer-based specimen flows.

- Quest Diagnostics (Secaucus, NJ) — A major, broad-based reference provider with integrated diagnostic information services and substantial contract reach into hospitals and health systems. Quest remains a primary comparator for scale-driven network and logistics capabilities.

- Laboratory Corporation of America (LabCorp) (Burlington, NC) — A leading multi-service provider; recent strategic collaborations with telehealth platforms underscore its approach to extend diagnostic access into virtual care pathways.

- Sonic Healthcare Limited (Australia) — An international pathology operator that brings best-practice lab medicine processes and a multi-country footprint, relevant to clients assessing cross-border capabilities and standards harmonization.

- Mayo Clinic Laboratories (Rochester, MN) — Differentiates through research-driven, specialist-supported diagnostic services and complex-case expertise — a strategic partner archetype for rare-disease workflows.

- ARUP Laboratories (Salt Lake City, UT) — Known for molecular, genetic, and specialized testing; ARUP represents a model for R&D-driven reference lab growth.

- Eurofins Scientific, Synlab, Unilabs — European-headquartered operators that expand clinical reference services through acquisitions and innovative test launches; recent deals and product rollouts illustrate the pace of consolidation and product differentiation in specialty areas.

Recent industry moves that matter for 2026

- Strategic collaboration trends. LabCorp’s 2025 collaboration with a major telehealth provider signals a deliberate move to embed diagnostics into virtual care pathways — an acquisition-adjacent strategy that can accelerate specimen volumes and diversify revenue streams.

- Acquisition-driven capability build. Eurofins’ acquisition of a U.S. specialty laboratory underscored the strategic value of targeted assets that fill diagnostic gaps (e.g., kidney disease testing), enabling rapid access to specialized specimen flows and clinical expertise.

- Product innovation and validation. New clinically validated assays for psychiatric and complex conditions — exemplified by Synlab’s product launch in 2025 — demonstrate how diagnostic innovation can create novel clinical pathways and payer discussion points.

Strategic implications and recommended actions for 2026

- For executives considering M&A: Prioritize assets that deliver immediate clinical differentiation or upstream specimen access (telehealth partnerships, employer channels, specialty disease portfolios). Use our M&A readiness checklist to quantify integration risk and post-close synergies.

- For operations leaders: Fast-track modular automation projects with a focus on pre-analytic automation and sample routing to achieve measurable TAT reductions within 12 months. Implement a layered staffing model that pairs automation with in-house subject-matter experts.

- For commercial teams: Revisit contracting approaches with payers and health systems to include performance-based clauses tied to accuracy, TAT, and cost-per-case metrics. Leverage bundled-service pilots to demonstrate value for chronic and specialty disease pathways.

- For product and R&D: Invest selectively in AI-augmented interpretation and validated multi-analyte panels where clinical need and reimbursement prospects align. Build evidence-generation plans early to support payer conversations.

- For public-sector planners: Incorporate outsourcing options into resilience planning, emphasizing contractual safeguards for reagent supply and surge capacity during public health events.

Call to action

This briefing highlights the strategic directions and operational levers that will matter most in 2026. For market participants who require the detailed modeling, tactical playbooks, and proprietary benchmarking that underpin board-level and investment decisions, access to the full Clinical Reference Laboratory Services Market report is essential. The report provides the underlying datasets, scenario models, and step-by-step implementation checklists that we intentionally reserve for the full publication — the exact intelligence that will convert diagnostic market visibility into competitive advantage.

Clinical Reference Laboratory Services Market

PW Consulting remains available to support executive briefings, bespoke modeling, and M&A diligence aligned to your portfolio priorities. Contact us to schedule a tailored advisory session and secure the full report for operational deployment.

For detailed analysis of this topic, please visit the official page:Clinical Reference Laboratory Services Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com