Synthetic Biology Market Trends in DNA Synthesis and Genome Design

Other |

2026-06-22 13:12:08

As capital allocations tighten and project timelines compress in 2026, ETFE membrane systems have moved from niche architectural experimentation to a strategic material choice across high-profile roofing, façade and enclosure programs. PW Consulting’s new ETFE Membrane Market report (base year 2025) synthesizes five years of historical performance and a seven‑year forecast to deliver a decision-grade toolkit for corporate strategy, procurement and engineering teams. This release is designed as a strategic “trailer”: it surfaces high-conviction trends, supplier dynamics and actionable pathways while reserving project-level, segmented datasets for subscribers and licensed clients.

ETFE Membrane Market

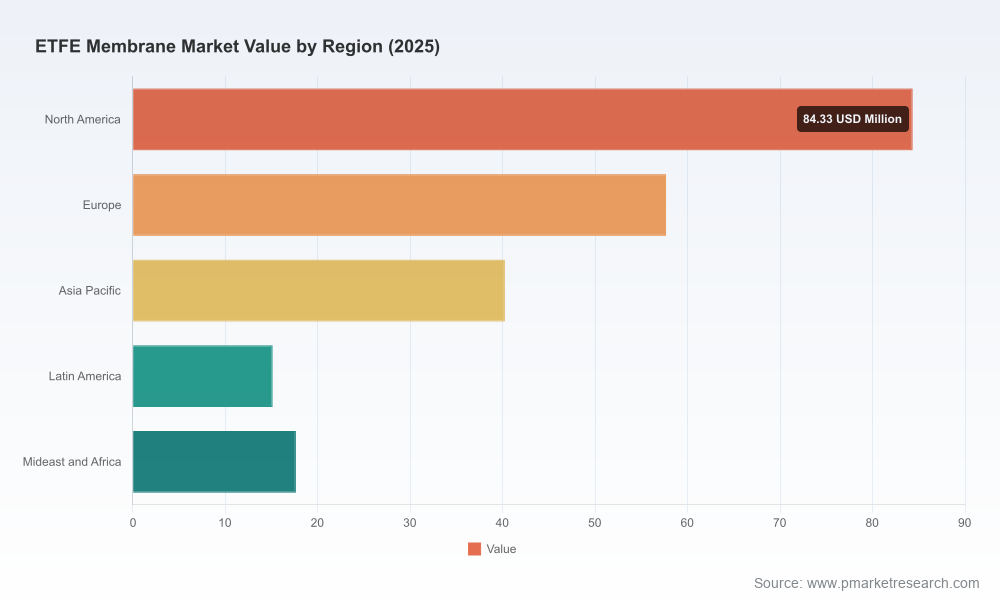

The ETFE sector has exhibited sustained expansion through the 2020–2025 historical window, reaching a market size of USD 215.0 Million (base year 2025). Our consolidated forecast through 2032 projects continued robust growth to USD 409.06 Million, underpinned by an 8.8% compound annual growth rate (CAGR) across the 2026–2032 horizon. These figures reflect cumulative adoption across architectural, sports and specialty industrial applications as stakeholders favor lighter, recyclable and high‑transparency membrane solutions.

ETFE Membrane Market

For executives planning 2026 capital allocation rounds, the headline implication is straightforward: ETFE represents a maturing, investible materials class with predictable growth, yet a market structure that remains relatively fragmented (CR3 ≈ 24.6%, CR5 ≈ 26.2%). The combination of healthy growth and low top‑end concentration creates multiple routes to capture value — from upstream resin sourcing to integrated system delivery — but it also elevates tactical supplier selection and risk management as critical near‑term priorities.

ETFE Membrane Market

Standards and design certainty: The activation of the DIN CEN/TS 19102 standard for tensioned membrane structures (including welded ETFE connections) in 2024 has materially reduced design uncertainty for large-scale tenders. For owners and lead designers, standardized limit-state guidance shortens approval cycles and supports predictable warranty and lifecycle planning.

Materials innovation and UV resilience: Material enhancements — typified by Daikin’s introduction of a high-UV-resistance ETFE film in 2023 — are raising the performance floor for envelope longevity. These technical advances shift procurement conversations from “if” to “which grade,” demanding more sophisticated technical specifications and performance-based contracting.

Supply chain differentiation: Legacy producers with long-established polymer manufacturing footprints and in-region production sites provide distinct delivery and quality advantages. Several legacy producers emphasize premium resin formulations and process control (for example, melt-extrusion and cast film technologies). Procurement teams need supplier scorecards that weight process provenance, resin traceability and aftermarket support.

System-level adoption and turnkey play: Market participants increasingly favor full-system solutions — combining membrane supply, pillow fabrication, edge and cushion systems, and installation services — especially for complex stadia and transit projects. This trend benefits firms with integrated capabilities or established installation partners, while creating margin and differentiation opportunities for specialty fabricators.

High-visibility project momentum: Landmark installations (for example, a notable ETFE roof installed at a major transportation-linked plaza in August 2025) continue to function as live demonstrations of cost, maintenance and daylighting benefits. These projects accelerate client confidence but also sharpen scrutiny around acoustic, lifecycle and cleaning regimes.

The ETFE value chain is populated by a mix of polymer manufacturers, film converters and membrane system integrators. Our report profiles the players below and analyzes their strategic levers — useful for sourcing, partnership formation or M&A diligence.

NOWOFOL Kunststoffprodukte GmbH & Co. KG (Siegsdorf, Germany) — A legacy European film producer with over 50 years of operations, NOWOFOL’s NOWOFLON series emphasizes architectural-grade film quality and deep process experience. Its long-run manufacturing history supports claims on production consistency and supply continuity.

Dyneon GmbH (3M) (Germany) — Focused on ETFE resins and films for high-performance applications, Dyneon leverages fluoropolymer expertise and a global chemicals footprint to serve demanding architectural and industrial specifications.

Chemours Company (United States) — With its Tefzel ETFE resins, Chemours is a strategic supplier for manufacturers targeting high-performance durability and chemical resistance. Its upstream resin position is a bargaining chip for customers seeking formulation control.

Asahi Glass Company (AGC) (Japan) — AGC’s Fluon ETFE film offerings span solar, architectural and membrane applications, reflecting a diversified industrial approach and R&D emphasis on film application performance.

Daikin Industries, Ltd. (Japan) — A catalyst for material-level innovation, Daikin’s UV-resistant ETFE development shifts lifecycle and warranty expectations and pressures competitors to demonstrate equivalent UV stability.

Textiles Coated International (TCI) (United States) — TCI’s melt extrusion casting from 100% virgin premium-grade ETFE resin positions it as a supplier of controlled, high-purity film suited to architectural projects where optical and mechanical consistency matters.

Birdair Inc. (United States) — As a system integrator, Birdair offers TensoSky ETFE film solutions and end-to-end tensile membrane services, which are attractive to clients seeking single‑contract responsibility.

Novum Structures (United States/EU) — Novum’s product set (air-filled pillows, stressed-skin membranes) targets clients who prioritize performance customization and modular installation workflows.

Enclos Tensile Structures (United States) — Enclos supplies ETFE as part of tensile and canopy solutions, emphasizing installation expertise and integration with building envelope systems.

Collectively, these companies illustrate two dominant strategic archetypes: upstream resin/film technology incumbents that compete on material science and supply security, and downstream integrators that compete on system performance and delivery risk management. Successful 2026 strategies will typically combine elements from both archetypes: secure resin supply and validated film chemistry, plus proven system integration and aftercare.

Procurement & contracting: Shift to performance-based specifications that tie warranty payments to validated UV and weathering outcomes; require traceability to resin production lots. Adopt multi-layer contracting where material supply and installation responsibilities are split to protect against single‑point failures.

CapEx & portfolio planning: Prioritize pilot projects that test new film grades under local climatic loads before scaling. Use our TCO templates to quantify trade-offs between higher upfront film specification costs and lower lifecycle maintenance.

Supply-chain resilience: For critical programs, secure long‑lead resin commitments from upstream producers or negotiate supplier-financed inventory arrangements with converters, particularly where production footprint and logistics risk are concentrated.

Innovation partnerships: Engage material innovators and testing labs in co‑funded durability studies to accelerate acceptance of next‑gen films and to capture first‑mover advantages in new application niches.

M&A and alliance play: Consider bolt‑on acquisitions that close capability gaps (e.g., a film converter acquiring a fabrication specialist) to create vertically integrated offers that command system premiums.

ESG and lifecycle strategy: Embed recyclability and resin origin into procurement scoring and public communications; material traceability will be increasingly material to public infrastructure tenders and private ESG mandates.

Our synthesis of the 2020–2025 performance window and the 2026–2032 forecast equips decision-makers with both the macro lens (market size, 8.8% CAGR, fragmented concentration) and the micro levers (supplier capabilities, technical standards, and procurement mechanics) necessary to convert market growth into durable competitive advantage. The industry is poised between rapid technical improvement and a commercialization phase where delivery certainty — not just material novelty — will win contracts.

For any organization evaluating whether to (a) specify ETFE for a marquee project, (b) integrate ETFE supply into its materials strategy, or (c) pursue investment or M&A in the space, the choices made in 2026 will materially affect long-term returns. PW Consulting’s report provides the missing operational grammar — from contract clauses to scorecards — that transforms high-level conviction into low-friction execution.

To access the full dataset, segmented maps, supplier scorecards and project-level cost models referenced here, visit the PW Consulting ETFE Membrane Market report landing page. The full report contains the granular regional, type and application splits, and downloadable financial templates that are intentionally withheld from this briefing to protect the integrity of client-grade analytics.

Contact PW Consulting’s ETFE practice for bespoke briefings, procurement clinic workshops, or M&A diligence support tailored to your 2026 strategic timeline.

For detailed analysis of this topic, please visit the official page:ETFE Membrane Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com