Plastic Sorting Machine Market: Strategic Imperatives for 2026 — PW Consulting Releases Forward-Looking Industry Brief

PW Consulting’s new market research brief on the Plastic Sorting Machine Market (base year 2025; forecast period 2026–2032) delivers a focused, decision-ready interpretation of where the industry is heading and what senior executives must act on in 2026. Our analysis finds the market expanding at a robust compound annual growth rate (CAGR) of 11.68%, with total industry revenues rising materially from a 2025 base. This trajectory, combined with concentrated supplier structures and tightening regulation in major end-markets, creates both acceleration and risk for manufacturers, recyclers, investors, and public procurers planning capital allocation and supply-chain strategies next year.

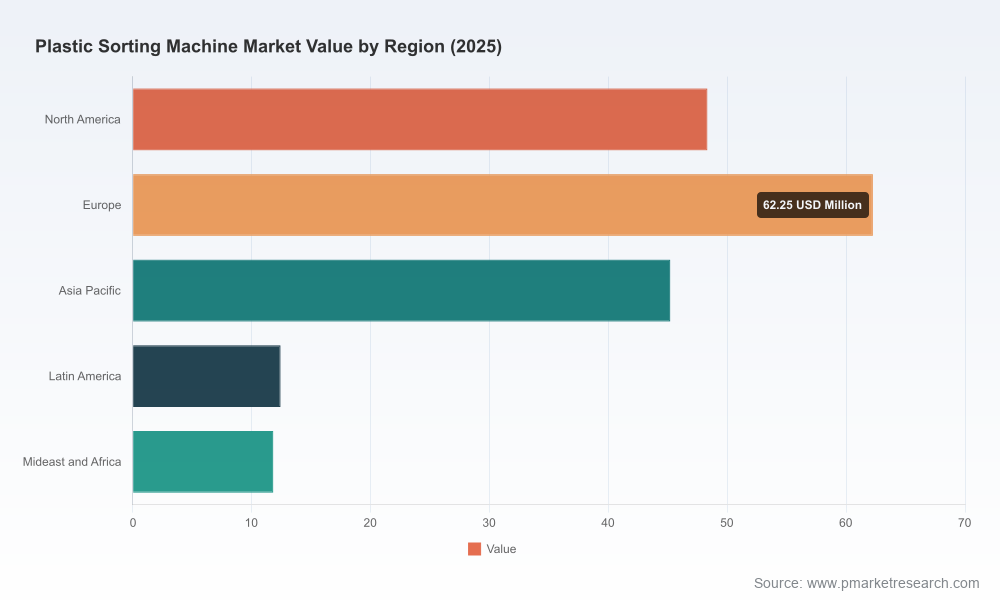

Plastic Sorting Machine Market

Headline trajectory: what the numbers imply for strategy

The market’s growth profile is unambiguous: higher volumes of post-consumer and post-industrial plastics, heightened recycling targets, and rising automation adoption are collectively translating into multi-year demand expansion for plastic sorting equipment. A faster-than-average market CAGR through the 2026–2032 forecast window means that 2026 is a pivotal planning year — the moment to move from pilot projects to scalable deployments or to recalibrate supplier exposure before component lead times and pricing volatility fully manifest.

Plastic Sorting Machine Market

Why 2026 is a strategic inflection point

- Regulatory timing: Several extended producer responsibility (EPR) and recycled-content mandates come into sharper effect in 2025–2026, creating near-term compliance deadlines that will drive capex decisions in 2026.

- Supply constraints: Critical components for NIR and short-wave infrared systems are produced by a concentrated set of suppliers, producing lead-time volatility measured in months. Procurement windows must therefore be extended and hedged.

- Consolidation pressure: The market exhibits meaningful concentration among the top vendors, making partner selection a strategic choice that influences access to spare parts, software upgrades, and service networks.

Market dynamics and operational risks

Our dynamic analysis synthesizes regulatory, supply-chain, and labor-cost signals that are already shaping procurement and operations decisions:

Plastic Sorting Machine Market

- Regulatory acceleration: Emerging mandates on recycled content and producer responsibility are increasing demand for sorting throughput and quality. Compliance-driven projects in 2026 will favor technologies that maximize purity and reporting transparency.

- Component-level volatility: Specialist detector arrays and SWIR cameras (used in NIR and hyperspectral systems) have experienced lead-time volatility of roughly 16–24 weeks due to supplier concentration. This raises procurement risk for OEMs and end-users planning 2026 installations.

- Labor arbitrage and automation: High labor cost environments (notably in some Western jurisdictions) continue to incentivize higher automation intensity and remote diagnostics, accelerating the adoption of AI-enabled inspection and sorting modules.

- Cost of advanced optics: Advanced NIR spectroscopy modules represent a material capital line item for linebuilders and buyers. Buyers who delay procurement risk facing price and delivery premiums.

Technology and segmentation trends (what we disclose and what we don’t)

The report highlights three dominant technology families — conventional optical color sorters (RGB-based), near-infrared (NIR) spectroscopy systems (including AI-assisted NIR variants), and hyperspectral imaging solutions — and profiles their fit across common recycling and waste-management use cases. Each technology path offers a distinct trade-off between throughput, material-purity performance, and total cost of ownership.

In this release we present qualitative differentiation and performance benchmarks for these technologies, while withholding granular segment-level revenue breakdowns by type, application, and region. This “preview” approach demonstrates analytical depth while directing readers to our full dataset for detailed allocations and model outputs.

Competitive landscape: who matters for 2026 partnerships

The supplier landscape is a mix of specialist optical-sorter OEMs, vertically integrated players, and regional equipment manufacturers. Market concentration metrics indicate that leading firms command a meaningful portion of commercial activity — a factor that affects pricing power, spare-parts availability, and aftermarket support.

- Anhui Zhongke Optic-Electronic Color Sorter Machinery Co., Ltd. (Hefei, China) — Offers a broad portfolio of optical sorting solutions for bottles, flakes and pellets, including AI-augmented NIR systems and intelligent control suites. Their full-range positioning makes them a top-tier supplier for scale projects.

- Anhui Jietai Intelligent Technology Co., Ltd. (Hefei, China) — Focuses on advanced optical color sorters targeted at recycling applications; notable for solutions optimized around throughput and integration into existing sort lines.

- Hefei Changlong Optoelectronic Technology Co., Ltd. (Hefei, China) — Produces bottle and flake sorters leveraging optical and AI-NIR stacks; strong in tailored machine configurations.

- Hefei Meixing Intelligent Technology Co., Ltd. (Hefei, China) — Emphasizes whole-bottle and mixed-plastic sorting with integrated optical systems and factory automation features.

- Anhui Jiexun Photoelectric Technology Co., Ltd. (Hefei, China) — Builds intelligent color sorters using imported German/Japanese components to balance cost and premium performance.

- Promech Industries (Mark Color Sorter) (India) — Specializes in RGB camera-based color sorters for post-consumer recycling, often chosen where cost and local supportability are decisive.

Recent trade-show activity, product reveals, and academic projects underline the breadth of innovation and market interest. Exhibitions in 2025 showcased multiple new optical-sorting platforms, and university-led prototypes demonstrate accelerating grassroots innovation — but commercial scale requires validated reliability and serviceability, which remains the domain of established OEMs.

What the full report contains — practical tools for 2026 decision cycles

Our comprehensive report is intentionally operational. It equips executive teams with the templates and datasets to make high-stakes 2026 decisions, including:

- Actionable TCO models and CapEx payback calculators that incorporate component lead-time risk and service-cost inflation assumptions.

- A supplier risk matrix and procurement playbook designed to shorten negotiation cycles while preserving delivery reliability.

- Regulatory-impact playbooks that translate EPR and recycled-content mandates into required throughput and purity thresholds for different compliance timelines.

- Scenario-based demand models for 2026–2032 that stress-test investments against combinations of regulation, commodity pricing, and labor-cost shifts.

- Go-to-market and retrofit strategies for recyclers and OEMs, including modular upgrade paths and software-as-a-service (SaaS) opportunities for analytics and remote maintenance.

- Competitive benchmarking and M&A signal maps to identify attractive acquisition targets or partnership candidates in 2026.

Implications for capital allocation and procurement in 2026

Key recommendations derived from our analysis for 2026 planning:

- Advance procurement timelines for optical and NIR modules: Given multi-month lead times for specialized imaging detectors, organizations should move orders forward by at least one procurement cycle or contract with OEMs that maintain buffer inventories.

- Insist on service SLAs and local-spare strategies: The commercial value of a sorting line increasingly depends on uptime and predictable throughput; negotiate service level agreements that include rapid spare-part delivery and remote-diagnostic capabilities.

- Hedge technology bets with modularity: Select platforms that support incremental upgrades (e.g., adding NIR or hyperspectral modules later) to balance near-term budget constraints with mid-term purity requirements.

- Factor regulatory timing into ROI: Capital approvals in 2026 must explicitly model the impact of recycled-content requirements and EPR schedules on revenue and avoidance-of-fine economics.

- Explore commercial alternatives: Service models, such as equipment-as-a-service or revenue-sharing for retrofit installations, can accelerate adoption while preserving capex flexibility.

How PW Consulting’s brief helps senior leaders

This brief is designed for boards, CFOs, Head of Engineering, and strategic procurement leads who require a clear, prioritized set of actions for 2026. We combine proprietary demand modeling with supplier intelligence, regulatory mapping, and practical procurement checklists so leaders can:

- Decide which technology families to adopt at scale in 2026 versus pilots to defer;

- Structure contracts to mitigate component-supply risk and protect margins;

- Design capital plans that align with regulatory milestones and commercial recycling economics;

- Identify high-probability partnership or acquisition targets to accelerate capability build-out.

Next steps and where to access the full intelligence

This press release presents the strategic narrative and core implications of our analysis while deliberately withholding the full segment-level tables, regional splits, and line-item financials that form the foundation of procurement and investment decision-making. For complete datasets, downloadable models, supplier scorecards, and the full methodological appendix, please access the PW Consulting report landing page.

2026 will be a year in which timing matters as much as technology choice. Organizations that move early to secure components, lock in service partnerships, and align investments with regulatory timetables will capture outsized value. Our report gives you the framework and the numbers to do exactly that — with the detailed, segment-level intelligence available on the report webpage to validate vendor selection, finalize capex approvals, and operationalize compliance planning.

For detailed analysis of this topic, please visit the official page:Plastic Sorting Machine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com