Calculators Market 2026 Preview: Strategic Imperatives from PW Consulting’s New Report

PW Consulting’s latest Calculators Market report (base year: 2025; historical window: 2020–2025; forecast: 2026–2032) provides an evidence-based, practitioner-focused roadmap for executive decision-making as organizations enter 2026. The report synthesizes robust market modelling with go-to-market playbooks, scenario-based risk analysis, and competitive intelligence—designed so CFOs, product leaders, channel partners, and strategic investors can act with conviction while avoiding common missteps in a market that is small in headline dollars but structurally important across education, professional and business workflows.

Calculators Market

Headline dynamics and what they mean

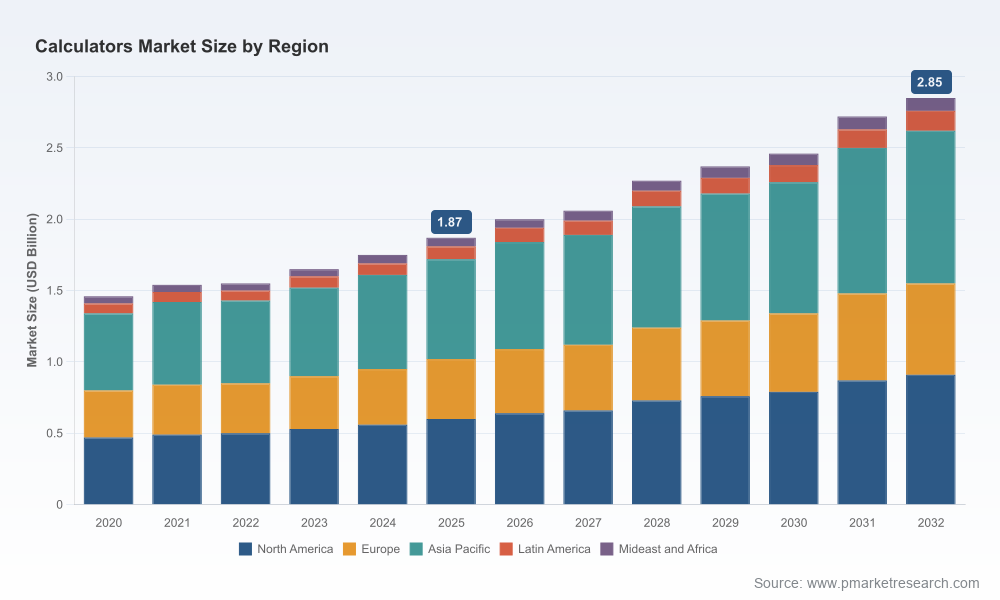

From a macro perspective, the calculators market has demonstrated steady, resilient growth through mid-decade. Our historical model shows market size expanding from USD 1.45 Billion in 2020 to USD 1.87 Billion in 2025. Under conservatively modelled uptake scenarios, PW Consulting projects the market will continue expanding to reach roughly USD 2.85 Billion by 2032, representing a compound annual growth rate (CAGR) of 5.12% across the forecast horizon. These figures frame the market as a stable, mid-single-digit growth opportunity—appealing for targeted investments that prioritize product differentiation, distribution efficiency, and services monetization over volume-led scale plays.

Calculators Market

Key structural features visible in the dataset and qualitative research are summarized below and inform the strategic implications that follow:

Calculators Market

- Demand drivers remain anchored in education and professional workflows, where hardware reliability, exam compliance, and institutional procurement cycles continue to support baseline unit volumes.

- Product heterogeneity—from basic and scientific through graphing and financial models—creates natural niches for differentiation that are not easily disrupted by single-channel entrants.

- The market’s competitive profile is moderately fragmented: the top three suppliers account for roughly a quarter of industry revenues, and the top five for around a third. This concentration pattern leaves room for both niche-focused innovators and consolidation plays.

- Regulatory noise is minimal. Our sector dynamics sweep found no new regulatory developments materially affecting device certification, classroom use policies, or cross-border distribution requirements as of June 2026—removing a key uncertainty from near-term planning.

Strategic takeaways for 2026 planning

- Prioritize product-market fit over broad coverage. Given the modest overall market scale and clear segmentation by user needs, success in 2026 will favor targeted investments—e.g., enhancing graphing UX for secondary/tertiary education or extending battery and connectivity robustness for field professionals—rather than blanket SKU proliferation.

- Monetize services and software adjuncts. With hardware margins under pressure in mature segments, recurring revenue levers—warranty/repair programs, secure content subscriptions for education providers, classroom management integrations—are high-return complements that the full report models quantitatively.

- Channel and procurement playbooks matter. Institutional purchasing cycles dominate certain subsegments. Negotiating multi-year procurement agreements, building preferred-vendor relationships with textbook publishers and educational platforms, and optimizing reseller economics will outsize product feature improvements in near-term ROI.

- Design for constrained disruption. While mobile devices and apps encroach on simple calculation tasks, exam-regulated environments and professional certification bodies maintain persistent hardware demand. Successful firms will explicitly design products and go-to-market strategies to coexist with digital alternatives (e.g., secure, exam-compliant functionality; hardware-anchored workflows).

- Use scenario planning to manage supply and pricing risk. Our report includes stress-tested scenarios for component shortages, FX volatility, and channel dislocations. Executives should adopt the recommended hedging and inventory strategies to avoid margin erosion in episodic supply shocks.

What’s inside the PW Consulting report — practical, executable content

The report is structured for immediate operational use. Highlights include:

- Proprietary market model with downloadable spreadsheets: baseline, upside, and downside scenarios calibrated to 2020–2025 trends and forward-modeled through 2032. The model is parameterized so teams can swap in custom assumptions and see P&L impacts.

- Go-to-market playbooks by customer archetype: education procurement, retail mass-market, professional specialist channels, and OEM/B2B partnerships—with detailed negotiation levers, pricing bands, and channel margin models.

- Feature-pricing sensitivity analyses and product roadmap templates that translate feature priorities (e.g., graphing performance, exam locks, rechargeable systems) into projected revenue uplift and payback periods.

- Supply-chain stress test templates, including component lead-time buffers, dual-sourcing checklists, and contract language to transfer risk.

- M&A and partnership playbooks for scale or capability acquisition, including a stepwise diligence checklist, valuation heuristics, and integration scorecards tailored to the calculators market.

- Competitive benchmarking dashboards: deliberate, comparable matrices that assess incumbents on product breadth, channel reach, price positioning, and institutional relationships (note: detailed segment-by-segment revenue tables are curated in the full report to preserve analytical integrity and are accessible on request).

- SKU-level pricing and cost templates that allow finance teams to run margin recovery scenarios and evaluate aftermarket service economics.

Collectively, these assets convert market insight into executable decisions—what to fund, when to accelerate distribution, and which partnerships to pursue in 2026.

Competitive landscape: profiles and implications

Our competitive analysis focuses on established suppliers active across education, professional, and office verticals. PW Consulting’s qualitative and quantitative assessment synthesizes product positioning, channel footprints, and strategic intent.

- Texas Instruments Incorporated (Dallas, Texas, USA) — https://www.ti.com/ TI remains synonymous with graphing and scientific calculators, with entrenched adoption in educational institutions. Their product line benefits from strong brand recognition, exam compliance, and broad teacher/institutional familiarity. For competitors, TI’s presence increases switching costs in education, making targeted innovation (user interface, software integration, or specialized ancillary services) essential to erode incumbency.

- Casio Computer Co., Ltd. (Shibuya, Tokyo, Japan) — https://www.casio.com/ Casio’s offerings span scientific, graphing, and financial calculators and maintain strong distribution in global education markets. The brand’s multi-segment footprint gives it resilience across cyclical demand shifts. Strategic plays against Casio require either specialty superiority in a niche or partnerships that expand reach within underserved institutional channels.

- HP Inc. (Palo Alto, California, USA) — https://www.hp.com/ HP competes with professional-grade scientific models and leverages an enterprise-oriented go-to-market muscle. Their advantage lies in cross-selling to existing office and professional clients and leveraging broader enterprise procurement channels. For PE-backed entrants, HP’s presence underscores the value of channel alignment with office-focused distribution partners.

- Sharp Corporation (Sakai, Osaka, Japan) — https://global.sharp/ Sharp’s catalog includes scientific and financial calculators suitable for educational and business use. The company’s strengths are product reliability and office-channel integrations. Positioning against Sharp benefits from differentiated features or value-added service models.

- Canon Inc. (Tokyo, Japan) — https://global.canon/ Canon’s calculator lines complement its broader office equipment portfolio. Their integration opportunity—with office supplies and enterprise contracts—creates a platform effect that new entrants should evaluate when designing channel strategies.

- Victor Technology LLC (Bolingbrook, Illinois, USA) — https://victortech.com/ As a supplier of scientific, financial, and printing calculators (including partnerships under the Sharp brand), Victor plays a specialized role in U.S. professional and education markets. Their presence highlights the patchwork nature of distribution and the importance of localized channel partnerships.

Collectively, these players create a competitive environment characterized by brand endurance, channel complexity, and feature-led differentiation. With the top three firms accounting for approximately 25% of revenues and the top five for about 36%, the sector remains open to targeted disruption and consolidation—particularly in aftermarket services and adjacent digital offerings.

Recommended next moves for decision-makers

- For OEMs and product leaders: Adopt PW Consulting’s feature-pricing sensitivity tool to prioritize R&D spend that yields the fastest payback; pursue modular product architectures to reduce SKU proliferation costs.

- For channel partners and distributors: Negotiate value-added service clauses and examine exclusive procurement windows with education providers to smooth seasonality.

- For private equity and strategic investors: Target tuck-ins that provide aftermarket services, classroom management software, or regional distribution efficiencies rather than chasing broad hardware scale.

- For school systems and institutional buyers: Use the report’s procurement playbook to standardize total cost of ownership (TCO) evaluations and to structure multi-year agreements that lock favorable pricing and service levels.

Closing — access the full analytical toolkit

PW Consulting’s report balances strategic depth with practical tools designed for immediate adoption in 2026 planning cycles. This release intentionally foregrounds the analytic framework, scenario logic, and executive playbooks that underpin our recommendations while preserving detailed segment-level tables and proprietary dashboards for subscribers. Readers requiring the full dataset, vendor-level revenue breakdowns, and downloadable modelling workbooks can obtain the complete report and supporting deliverables via PW Consulting’s report page.

For executives preparing budgets and strategic roadmaps for 2026, the calculus is clear: prioritize targeted differentiation, monetize services, and align channels to institutional demand. PW Consulting’s Calculators Market report delivers the empirical foundation and operational templates needed to translate that strategy into results.

For detailed analysis of this topic, please visit the official page:Calculators Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com