3 High explanation why males are going through abrupt well being disaster

Health |

2026-06-01 11:26:11

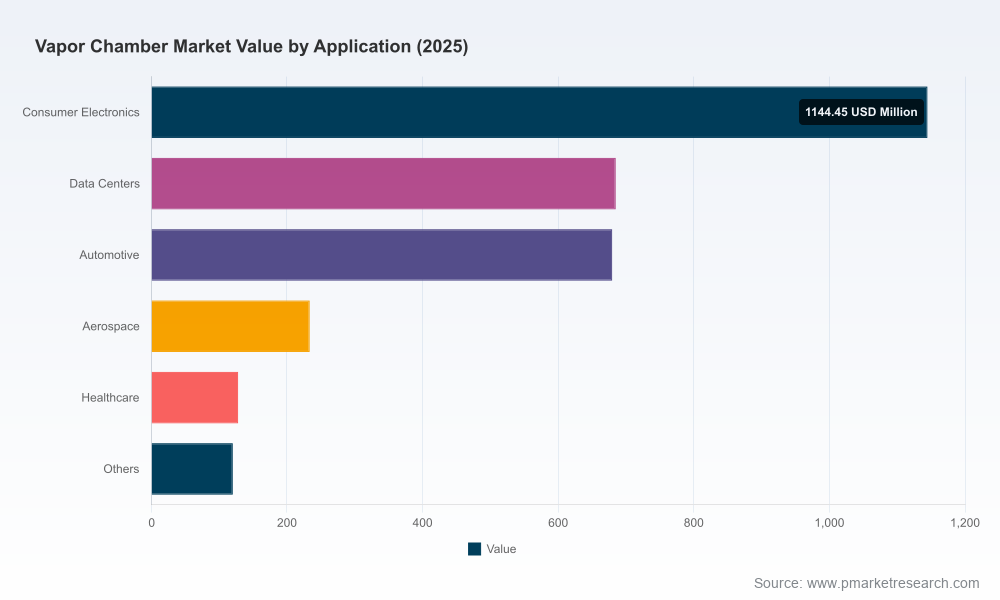

As organizations position for a new wave of compute-intensive products and electrified platforms, vapor chamber thermal solutions are moving from niche to foundational. Our latest PW Consulting market study — with a 2025 base year and a 2026–2032 forecast horizon — projects continued strong expansion at a compound annual growth rate of 10.5%. The global market, which stood at roughly USD 2,990 million in 2025, is on a trajectory to approach USD 5.8 billion by 2032. That growth is being driven by converging forces: the proliferation of AI and high-density data center workloads, rising power densities in consumer and automotive electronics, and the premium placed on thin, high-performance thermal spreaders in portable form factors.

Vapor Chamber Market

Strategic timing — 2026 is a pivot year for procurement, capacity, and qualification decisions. With near-term capacity expansions ramping and a multi-year sales runway forecasted, companies that secure design wins and supply contracts now will realize disproportionate access to the fastest-growing demand pockets over the coming investment cycle.

Vapor Chamber Market

Cost and supply chain sensitivity — raw material volatility (notably copper) and trade policy changes are material to unit economics. These dynamics increase the value of supplier diversification, cost pass-through mechanisms, and localized sourcing strategies.

Vapor Chamber Market

Qualification as a barrier to entry — automotive and medical-grade applications impose long, capital- and time-intensive qualification cycles. Firms that align product development timelines to meet standards such as AEC-Q100, IATF 16949, and ISO 13485 will create durable competitive separation.

Fragmented supplier base — the market is not dominated by a handful of suppliers; top-three and top-five shares indicate a moderately fragmented structure. That fragmentation supports M&A and strategic partnership opportunities while preserving negotiation leverage for large OEM buyers.

Our report is designed to be operationally actionable. It blends forward-looking market modelling and risk-tested scenarios with supplier-level intelligence and pragmatic roadmaps. Key deliverables include:

Market forecast with scenario sensitivities (base, upside, downside) through 2032 — enabling CAPEX and revenue planning tied to alternative demand trajectories.

Supplier scorecards that evaluate capacity, technical depth, certifications, time-to-qualify, and commercialization risk — presented in a format that supports shortlists for RFQs and strategic sourcing.

Technology and product roadmaps that translate thermal performance trends (ultra-thin architectures, embedded solutions, high-throughput vapor chambers) into engineering and procurement milestones.

Cost and BOM sensitivity models that quantify exposure to commodity swings, tariff regimes, and process yield variations — paired with hedging and supplier-partnership playbooks.

Regulatory and qualification playbooks for automotive, medical, and aerospace programs, including recommended test matrices and realistic timelines for OEM sign-off.

M&A and partnership themes mapped to market concentration dynamics and customer qualification bottlenecks.

The vendor ecosystem combines long-standing thermal specialists, regional contract manufacturers, and newer entrants with targeted capabilities for AI and mobile platforms. Several strategic patterns are particularly relevant:

Capacity scale-ups oriented to AI servers — industry actors have announced meaningful capacity investments targeted at high-power applications. Large, dedicated expansions signal a race to secure design wins with hyperscalers and AI-stack providers; these moves materially alter lead times and bargaining leverage for buyers.

Product differentiation in thin and embedded solutions — suppliers are bifurcating around ultra-thin form factors for consumer devices and higher-volume, ruggedized modules for servers and automotive power electronics.

Geographic and vertical specialization — many suppliers maintain deep bench strength in specific verticals (consumer electronics, server, automotive, or medical) and are augmenting capabilities—materials, process control, quality systems—to win OEM qualifications.

Examples of strategic moves: recent capacity expansions and new-product launches underscore a fast-evolving supplier mix. Some vendors are scaling monthly output dramatically to target AI and ASIC cooling, while others focus on high-specification series aimed at next-generation thermal requirements.

Three non-market technical levers will determine winners in 2026:

Qualification standards: Automotive and medical programs require robust quality systems and multi-year validation plans. Buyers intending to enter these verticals must factor extended qualification timelines and supplier audits into program schedules.

Material cost exposure: Copper and related commodity dynamics are a meaningful cost driver. Recent commodity price pressure and tariff actions have made supplier cost models more sensitive; procurement strategies must be redesigned accordingly.

Supply chain policy risk: Trade and tariff developments affecting key inputs can alter on-shore vs. off-shore sourcing calculus overnight. Scenario-based sourcing that combines regional manufacturing pools with contingency inventory is now a baseline requirement.

Product and engineering leaders — prioritize early thermal architecture choices, and lock in prototype volumes with suppliers that have validated qualification pathways aligned to your end-market (e.g., AEC-Q100 for automotive). Doing so reduces schedule risk and improves negotiating position once volumes scale.

Procurement and supply chain — adopt a three-tier procurement strategy: strategic partners for high-spec platforms, diversified second sources for volume resiliency, and a tactical pool for spot coverage. Include commodity pass-through clauses and capacity reservation options in master agreements.

Corporate development — look for tuck-ins that add complementary process capabilities (ultra-thin stamping, embedded assembly, high-vacuum sealing) or regional footprints that mitigate tariff exposure and shorten lead times for critical customers.

Risk and compliance — embed qualification milestones into program governance and stress-test roadmaps against commodity and tariff shock scenarios. Build cross-functional playbooks for certification audits and recall-risk mitigation in regulated end markets.

PW Consulting models indicate decision-makers will face two dominant pathways this calendar year:

Accelerate-in strategy — invest in preferred suppliers and secure long-term capacity commitments to capture share in the rapidly growing AI and server segments. This pathway favors companies with balance-sheet flexibility and close OEM partnerships.

De-risk-and-diversify strategy — hedge commodity and policy risk by regionalizing supply and maintaining flexible second-source agreements. This pathway suits companies that prioritize margin protection and schedule certainty over first-mover share capture.

Vapor chambers have moved from an enabling technology to a strategic lever. With the market expanding at roughly 10.5% CAGR and near-term capacity and product shifts underway, 2026 is a make-or-break year for thermal strategies. Organizations that integrate supplier qualification timelines, commodity exposure analysis, and targeted partnership investments into their product roadmaps will turn thermal engineering into competitive advantage rather than a bottleneck.

The market brief above is a strategic preview. Our full Vapor Chamber Market Report includes the granular, actionable intelligence you need to execute in 2026: supplier scorecards, contract negotiation playbooks, BOM-level cost sensitivity models, qualification timelines, and prioritized M&A themes. For segment-level breakout data, detailed supplier assessments, and tailored scenario workshops, please download the full report from PW Consulting or contact our industry team for a bespoke briefing.

For detailed analysis of this topic, please visit the official page:Vapor Chamber Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com