GLP-1 Receptor Agonists Obesity Drugs Market: Insights, Key Players, and Growth Analysis

Other |

2026-06-08 03:20:33

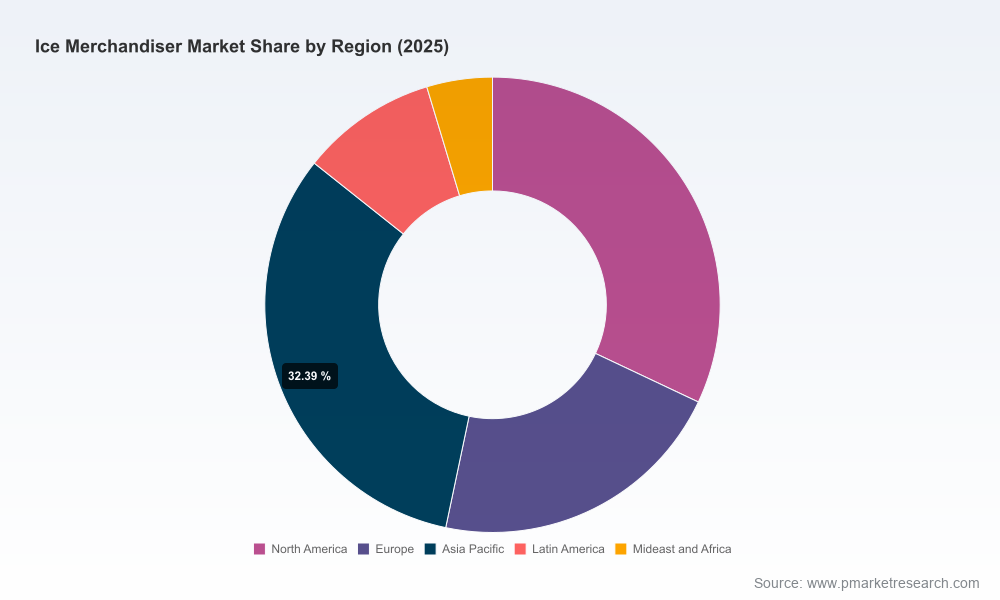

PW Consulting’s latest Ice Merchandiser Market report (base year 2025) frames a clear strategic horizon for executives making capex, product development, and channel decisions in 2026. The market is on a steady expansion path: from an estimated market size of USD 215.0 Million in 2025, the sector is projected to advance at a compound annual growth rate (CAGR) of 6.98% through our forecast window (2026–2032), reaching an anticipated market scale in the high hundreds by 2032. That trajectory is driven by intersecting regulatory, supply-chain and technology vectors that will materially affect unit economics, service models and aftermarket opportunity this year and beyond.

Ice Merchandiser Market

2026 is a pivot year. Manufacturers and channel partners are being asked to reconcile near-term operational pressures with long-term compliance and sustainability mandates. This report translates macro trajectories into decision-ready guidance: it quantifies market momentum, sequences the tactical moves that protect margins, and prescribes mid-term investments that unlock differentiated value (energy efficiency, low‑GWP refrigerants, service ecosystems). We adopt a practitioner-first orientation — scenario-based advisories, supplier playbooks and implementation checklists — to accelerate strategic choices while preserving operational optionality.

Ice Merchandiser Market

Regulatory acceleration: Global and national refrigerant policies (notably phasedowns of high‑GWP HFCs) are forcing faster adoption of low‑GWP alternatives such as hydrocarbons (e.g., R‑290), CO2 systems and emerging HFO blends. These transitions create both retrofit demand and new‑product requirements for safety, certification and technician training.

Ice Merchandiser Market

Material and component inflation: Stainless steel price pressure and volatility in commodity markets have materially increased production cost baselines. Manufacturers must re‑engineer bills of materials and explore alternate alloys or design efficiencies to preserve margins without compromising durability.

Supply‑chain continuity risk: Lead times for critical refrigeration components (compressors, evaporator coils, specialized controls) have stretched substantively. Strategic inventory and dual‑sourcing now affect launch schedules and warranty exposures.

Energy and lifecycle economics: ENERGY STAR and equivalent efficiencies are increasingly table stakes. Buyers are shifting from purchase‑price comparison to lifecycle cost equations, augmenting the monetization of energy‑saving features and maintenance contracts.

Exhibition and product cycles: Trade shows and industry gatherings in 2025–2026 have already served as launch pads for new merchandisers and refrigeration approaches. These events are fertile ground for channel recruitment and partnership signaling.

Market sizing and high‑confidence forecasting: A transparent topline time series for 2020–2032 with scenario overlays (baseline, accelerated regulation, commodity shock) that enable capital allocation under uncertainty.

Strategic segmentation frameworks: Taxonomies that map product types, applications and buyer archetypes to profitability levers — designed to inform portfolio prioritization and SKU rationalization.

Cost‑to‑serve and lifecycle models: Templates and worked examples that quantify tradeoffs between upfront price, energy consumption, refrigerant choice and service spend over realistic asset lifespans.

Procurement and supplier playbooks: Practical checklists for lead‑time buffers, component hedging and contract language to mitigate single‑source dependency risks.

Regulatory compliance mapping: Country‑by‑country impact matrices, retrofit timelines and certification pathways to align product roadmaps with evolving refrigerant policies.

Competitive landscaping and vendor scorecards: A pragmatic assessment of incumbent strengths/weaknesses and go‑to‑market postures, tailored to support M&A screening, alliance formation and distribution strategies.

Implementation playbooks: 90‑, 180‑ and 360‑day operational checklists for R&D, manufacturing, service teams and sales to rapidly operationalize strategic pivots.

The Ice Merchandiser market remains fragmented relative to heavy industrial sectors. Measured concentration metrics indicate that top suppliers do not dominate to the extent seen in consolidated industries, leaving space for nimble challengers and regional specialists to gain share through service differentiation, cost leadership or rapid regulatory compliance. In practice, this means incumbents must pursue both defensive and offensive moves: shore up aftermarket revenues and certification capabilities, while exploring bolt‑on acquisitions that add specialty capabilities (e.g., natural‑refrigerant engineering, outdoor‑rated enclosures).

True Manufacturing Co. — Known for commercially oriented ice merchandisers with NSF and ENERGY STAR certified options. Strength lies in regulatory‑compliant offerings and established retail channel relationships. Strategic focus: convert certification leadership into service bundles and leasing models that capitalize on energy savings.

Beverage Air — Broad refrigerated display portfolio including glass door and outdoor units positions the company well in both convenience retail and foodservice. Strategic focus: accelerate product line adaptations for low‑GWP refrigerants while tightening dealer training programs for field service.

Turbo Air — Early mover on natural refrigerants and ENERGY STAR lines. Competitive advantage is in technology positioning; to scale, Turbo Air should formalize training ecosystems and standardize retrofit kits for legacy installations.

Hussmann Corporation — Deep expertise in retail display and refrigeration systems; their strength is integration across store architecture. Strategic play: leverage system integration to sell energy‑optimization services and long‑term maintenance agreements.

Master Bilt — Focus on ice cream merchandisers and display refrigeration; strong product design heritage. Strategic focus: diversify into modular, serviceable platforms that reduce total cost of ownership.

ICEMaid — Offers dedicated merchandisers, bagged ice and refrigeration products. With direct product-market fit, ICEMaid can capture aftermarket and logistics synergies through bundled distribution agreements.

Polar Temp — Known for commercial and outdoor display units. Outdoor enclosure and reliability expertise creates a niche that is defensible with targeted field service networks.

Leer Inc. — Insulated merchandisers and cold storage solutions suggest opportunities to expand into last‑mile cold-chain services and turnkey store installations.

FOGEL USA — Commercial refrigeration and ice display equipment provider; strategic emphasis should be on product modularity and retrofit paths to low‑GWP systems.

Thermal Manufacturing Inc. — Insulated merchandisers and cold wall units highlight manufacturing quality. Opportunity: monetize quality through extended warranties and certified refurbishment programs.

Trade show cadence remains strong: Major industry events in 2025–2026 have served as launch platforms and scouting arenas for distributors and technology partners. Use exhibitions to validate prototype demand and recruit channel partners.

Product launches in 2025 underscore competitive momentum in refrigerated merchandisers — incumbents and challengers alike are refreshing portfolios with higher capacity and open‑air display designs.

Conferences oriented to cold‑chain and packaged ice trade groups remain important venues to monitor aftermarket trends and regulatory adoption timetables.

Accelerated regulatory scenario: Prioritize certification roadmaps and partner with HVAC/electrical training providers to build a certified service network. Lock in component suppliers for low‑GWP systems and deploy retrofit test programs.

Commodity shock scenario: Implement material substitution and design for manufacturability (DFM) sprints; renegotiate multiyear contracts with key metal suppliers and deploy targeted product SKUs for high‑margin accounts.

Rapid technology adoption scenario: Offer energy‑performance guarantees and bundled energy‑management services to convert total cost of ownership (TCO) savings into a compelling buyer proposition.

Review product BOMs for alloy and component alternatives; quantify margin sensitivity to material price swings.

Audit service capabilities and create a certification and training roadmap for low‑GWP refrigerant servicing.

Implement minimum inventory buffers for high‑risk components and initiate dual‑sourcing agreements where feasible.

Deploy pilot retrofit offers to key accounts to validate logistics and pricing models for transitioning existing installed bases.

Align product roadmaps to ENERGY STAR and NSF pathways and secure third‑party validation plans to accelerate market acceptance.

For executives, 2026 is the year to move from reactive compliance to proactive value creation. The Ice Merchandiser market’s steady CAGR and the structural signals described above create both risk and opportunity: manufacturers that combine regulatory foresight, supply‑chain resilience and service monetization will widen margin gates and capture aftermarket annuities. Our report provides the analytics, scenarios and tactical playbooks required to execute those moves.

This briefing follows the “trailer” principle: it outlines the report’s strategic contours and actionable frameworks while withholding proprietary segment‑level matrices and granular regional/application datapoints that underpin our forecast. PW Consulting’s full Ice Merchandiser Market report includes the detailed segmentation, interactive dashboards and vendor scorecards required to operationalize the strategies summarized above. Visit the PW Consulting portal to download the complete report and access the supporting tools, models and executive workshops designed to support 2026 decision cycles.

For detailed analysis of this topic, please visit the official page:Ice Merchandiser Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com