Hoe werkt Valium in het lichaam? Effecten en aandachtspunten

Health |

2026-04-08 18:29:31

Metal injection molding (MIM) materials are moving from a niche manufacturing input to a strategic lever for product differentiation, supply-chain resilience and sustainability. PW Consulting’s new market study — anchored on a 2025 base year and a 2026–2032 forecast horizon — finds the global MIM materials market has grown from roughly USD 2.6 billion in 2020 to about USD 4.0 billion in 2025 and is poised to approach the USD 7.6 billion mark by 2032, expanding at a compound annual growth rate of approximately 9.5%. For executives setting priorities in 2026, this trajectory signals a window to capture premium value by aligning materials strategies to evolving regulatory, technological and sourcing risks.

Metal Injection Molding Materials Market

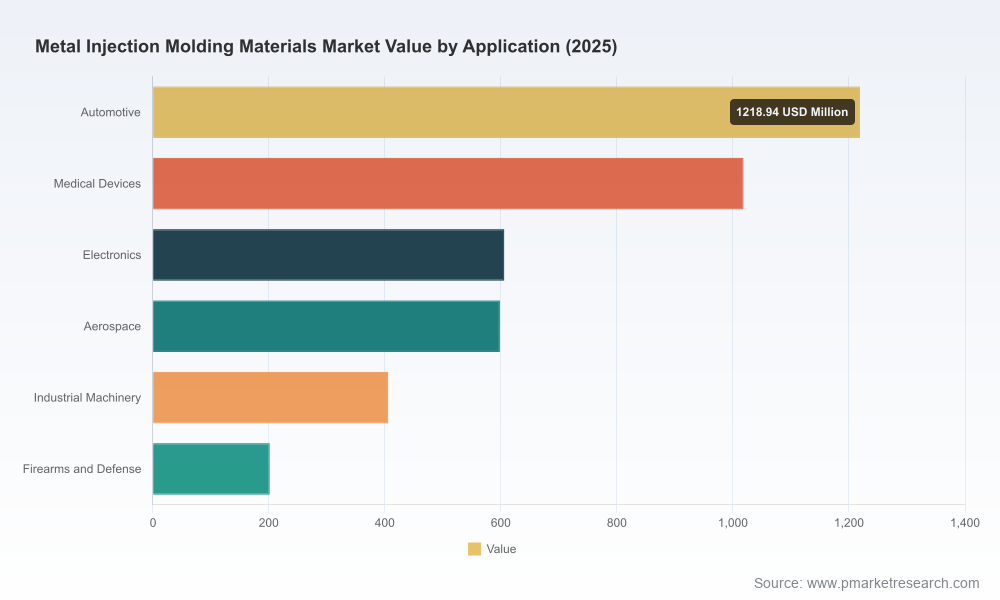

Growth is broad-based but outcome-driven: The market’s double‑digit equivalent expansion is being driven not simply by volume, but by higher-value materials (titanium alloys, specialty stainless grades, copper alloys) and by increased adoption in high-margin applications such as medical, aerospace and precision electronics.

Metal Injection Molding Materials Market

Regulation and sustainability are no longer peripheral: Environmental policies in major markets and public-sector initiatives to rebuild domestic powder/feedstock capacity are already reshaping sourcing economics and technology roadmaps.

Metal Injection Molding Materials Market

Supply-side competition is intensifying around feedstock innovation and vertical integration: Established chemical and powder metallurgy players are investing in high-purity powders, catalytic debinding feedstocks and localized capacities to shorten lead times and reduce lifecycle footprint.

Three dynamics will determine winners and losers in the coming 18–36 months.

Cost-to-performance pressure. Raw material availability, atomization capability and feedstock formulation expertise are the core value drivers. Buyers who can translate material selection into total-cost-of-ownership advantages — by combining powder selection, debinding processes and sintering profiles — will capture differentiation.

Regulatory and policy tailwinds. Stricter environmental rules in parts of Europe, and strategic initiatives in the United States to onshore powder and feedstock capabilities, are creating incentives for near-term capital allocation to domestic processing and low-carbon feedstock technologies.

Application-driven technical requirements. Medical and aerospace applications impose material purity, process traceability and qualification demands that raise barriers to entry but also expand margins for suppliers that can scale certified production.

The market combines specialist powder producers, chemical formulators and integrated powder metallurgy groups. The competitive topology favors firms that can combine material science leadership with manufacturing scale and compliance credentials.

BASF SE: Continues to advance its Catamold® portfolio with sustainability-focused feedstocks. Recent product introductions underscore the role of chemical formulators in reducing lifecycle environmental impact.

Hoganas AB and Sandvik AB: These powder specialists are investing in atomization and high‑purity production to meet rising demand for titanium and specialty stainless powders.

GKN Powder Metallurgy: Capacity expansions and advanced manufacturing investments are examples of how legacy powder‑metallurgy players are consolidating their position across feedstock and component value chains.

Regional and specialist players (e.g., OptiMIM, AMT, Epson Atmix, Indo‑MIM, Jiangsu GIAN, Advanced Powder Products and INMATEC): Provide agility through custom blends, fast prototyping and strong partnerships with OEMs in targeted applications.

Recent industry moves — from BASF’s sustainability-focused feedstock launch to GKN’s capacity investments and the renewed platform activity around MIM conferences — indicate a cycle of technology maturation and commercialization that will accelerate in 2026.

This is not a high-level brochure. The report is architected for decision-makers who must translate market signals into investment, sourcing and product-architecture choices during 2026 planning cycles. Key practical outputs include:

Scenario-based demand modelling: Demand curves and sensitivity analyses built around alternate adoption rates for premium alloys, debinding technologies and regulation-driven reshoring.

Supplier risk and opportunity maps: An actionable framework to prioritize engagement with powder producers, feedstock formulators and contract manufacturers based on capability, capacity and compliance readiness.

Commercial playbooks: Go-to-market and partnership templates for materials vendors and OEMs, including negotiating levers, qualification roadmaps for critical applications and pricing strategies under constrained supply.

Technology adoption roadmaps: A comparative assessment of catalytic debinding, thermal debinding and sintering profiles, with implications for throughput, yield and lifecycle carbon intensity.

Investment appraisals: CapEx/Opex modelling to evaluate local capacity expansion vs. contract manufacturing, including break-even analytics and stress-testing for raw-material volatility.

Supply Chain & Procurement: Rebalance supplier portfolios to reduce single-point powder dependency, prioritize partners with traceability and environmental credentials, and structure multi-year offtake agreements with flex clauses for alloy mix changes.

R&D & Product Management: Embed materials-selection constraints into early-stage design. Shortlist 1–2 feedstock partners for co‑development to accelerate qualification cycles for high-value applications.

Operations & Manufacturing: Pilot localized feedstock pre-processing or semi-finished powder handling to lower inbound risk and lead times, while benchmarking emissions intensity per production line as a procurement KPI.

Corporate Development & Strategy: Evaluate bolt-on acquisitions or joint ventures to secure technology (atomization, debinding catalysts) and to access certified production capacity in priority markets.

Executives should track a concise set of leading indicators that will materially affect MIM materials strategies:

Policy signals around domestic powder/feedstock capacity and environmental compliance timelines.

New product introductions from chemical formulators and powder producers that materially alter process yields or reduce lifecycle emissions.

Consolidation moves among mid‑tier feedstock suppliers, which could compress competition in specialty alloys.

Qualification timelines for medical and aerospace approvals — slippage here can reallocate demand across material grades and geographies.

PW Consulting’s research is designed as an executable toolkit for budget cycles and board-level discussions. Use the report to:

Prioritize capital allocation between onshore capacity and long-term supplier agreements using the included investment appraisal templates.

Refine product roadmaps by overlaying application-level demand scenarios with supplier qualification timelines included in the study.

Negotiate from an informed position: the report’s commercial playbooks provide contract clauses, price-indexing mechanisms and escalation triggers tailored to MIM feedstock realities.

Consistent with our commitment to commercial-grade intelligence, this release shows trends, strategic implications and supplier dynamics, but deliberately omits detailed segment-level tables, regional splits, application share-by-dollar, and proprietary cost model outputs. Those granular data — including country-level forecasts, SKU-level pricing models and the full supplier capability matrix — are available exclusively in the full report and online data dashboard.

The MIM materials market is at an inflection point. With the global market expanding at roughly a mid‑single-digit doubledigit equivalent pace and demand increasingly favoring higher-value alloys and application‑specific feedstocks, 2026 will be the year that separates strategic movers from reactive participants. Companies that secure differentiated access to quality powders, invest selectively in localized processing, and align product qualification pipelines to regulatory and customer timelines will capture disproportionate share and margin as the market advances toward 2032.

For C-suite teams preparing 2026 plans, PW Consulting’s report is structured to convert market intelligence into executable decisions — from sourcing strategies and technology investments to M&A plays and sustainability roadmaps. Access to the full dataset and operational tools is available on our report page; professionals seeking the detailed segmentation tables, supplier benchmarking matrix and downloadable cost models will find the precise inputs required to underwrite investments and negotiate from a position of strength.

To explore the full analysis and obtain the complete data package for scenario planning and procurement negotiations, please visit our report page for PW Consulting’s Metal Injection Molding Materials Market study.

For detailed analysis of this topic, please visit the official page:Metal Injection Molding Materials Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com