Camera Module Adhesives Market: Strategic Imperatives for 2026 — PW Consulting Intelligence Brief

As global device architectures accelerate toward higher optical performance, greater automation in module assembly, and tighter regulatory scrutiny, the camera module adhesives market is emerging as a strategic battleground for materials suppliers, OEMs and tier‑1 assemblers. PW Consulting’s latest market research — anchored on a 2025 base year and projecting into 2032 — quantifies a resilient sector growing at a mid‑single digit compound annual rate (CAGR) and provides the practical playbook executives need to convert that momentum into sustainable advantage in 2026.

Camera Module Adhesives Market

Why this market matters to 2026 decision cycles

Adhesives have migrated from a commoditized joining medium to a performance‑critical enabler across camera module value chains. The overall market is projected to expand materially during the 2026–2032 forecast window, reflecting continued demand from consumer electronics, automotive ADAS programs, and adjacent industrial applications. For strategists planning 2026 investments, this market sits at the intersection of three secular forces: optical miniaturization (driving tighter alignment and lower‑stress bonds), automation/throughput optimization (favoring fast‑curing chemistries and process integration), and compliance/regulatory pressure (demanding reformulation and disclosure). Our analysis shows that companies that align product development, sourcing and go‑to‑market strategies to these forces will capture disproportionate value.

Camera Module Adhesives Market

Macro snapshot (strategic takeaways)

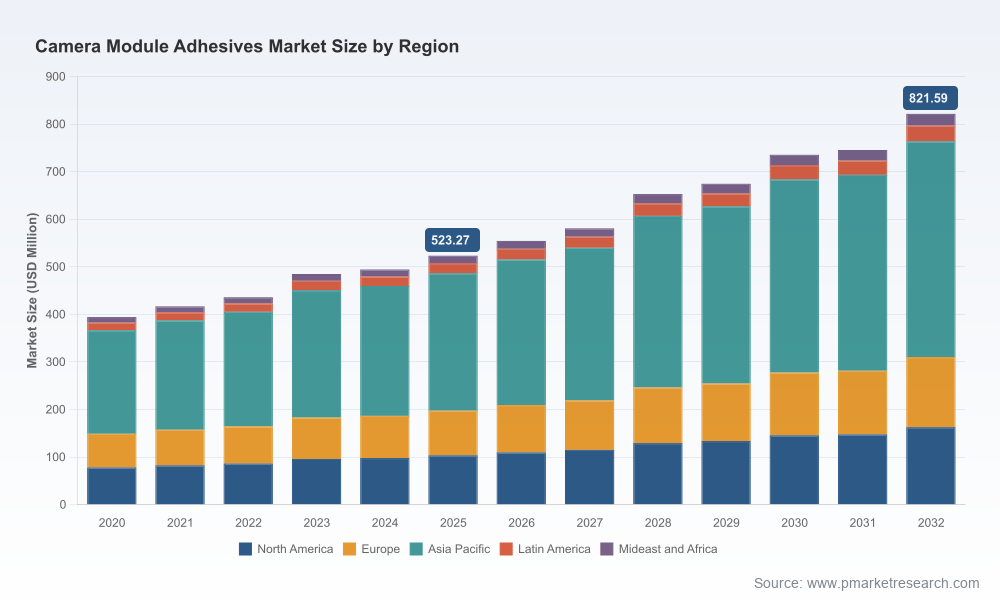

- Growth trajectory: The market has demonstrated steady recovery and expansion from the early 2020s into the mid‑decade and is forecast to continue on a durable upward path through 2032 at approximately a mid‑single digit CAGR. This trajectory underwrites near‑term investment in capacity and process upgrades, while also supporting longer‑horizon R&D for next‑generation chemistries.

- Concentration and competitive balance: Market concentration metrics indicate a moderately consolidated landscape — a handful of global players together control a meaningful share of demand, yet there remains room for nimble specialists and regional players to differentiate by application, process integration and regulatory compliance services.

- Profit pool dynamics: Margin opportunity is shifting to adhesives that reduce cycle time, lower defect rates during active alignment, and support heat‑sensitive substrates. Players that can couple material performance with process engineering and analytics command premium pricing.

What the full report delivers — actionable intelligence, not theory

PW Consulting designed the report as an operational toolkit for functional leaders and corporate strategists. Rather than a high‑level summary, subscribers receive:

Camera Module Adhesives Market

- Proprietary market sizing and a transparent forecasting model covering 2020–2032 with scenario toggles for demand shocks and regulatory stress tests;

- Technology and product roadmaps showing where curing modalities (UV, dual‑cure, thermal) and polymer classes (epoxy, acrylic, polyurethane, silicone and hybrids) intersect with assembly processes such as active alignment and lens bonding;

- Detailed supply chain maps highlighting critical raw materials, pinch points, tariff exposures, and alternative sourcing pathways; includes time‑phased recommendations to de‑risk 2026 procurement;

- Competitive benchmarking and capability heat maps across formulation expertise, authorization for automotive standards, regional manufacturing footprint and channel relationships;

- Commercial playbooks for a range of initiatives — from price‑mix optimization and distributor strategies to value‑based selling pilots with Tier‑1 OEMs — including templates for supplier scorecards and customer ROI calculators;

- M&A and partnership scouting lists prioritized by strategic fit, integration complexity and likely valuation multiples, plus modelled synergies for tuck‑ins focused on technology or geographic expansion;

- Regulatory impact matrix and compliance conversion plans for RoHS, REACH and emerging disclosure requirements — including estimated CAPEX/OPEX implications under plausible 2026 enforcement timelines;

- Operational diagnostics and pilot blueprints to reduce cycle time during active alignment, increase yields in lens bonding, and control VOC emissions in solvent‑based lines.

Competitive landscape — implications for 2026 playbooks

Our market layer maps show a spectrum of specialized incumbents and innovation leaders that will set the pace in 2026. Notable profiles include light‑curable epoxy specialists and dual‑cure innovators who balance low‑shrinkage chemistry with high throughput, alongside regional formulators focused on cost and compliance for specific end markets.

- Dymax Corporation: A leader in light‑curable optical epoxies, Dymax has reinforced its operational commitment and recently extended its position at its U.S. headquarters. Strategic implications for 2026: expect continued product launches aimed at lowering shrinkage during active alignment and accelerating cycle times. For partners and competitors, Dymax’s investments signal rising importance of rapid‑cure chemistries in high‑mix manufacturing.

- NAMICS Corporation: With strengths in insulating and alignment adhesives for fixed‑ and auto‑focus modules, NAMICS represents a classic specialty play. Their engineering depth suggests opportunities for co‑development with camera module assemblers seeking tailored formulations.

- ThreeBond Co., Ltd.: Focused on rapid, low‑temperature curing solutions for consumer electronics, ThreeBond exemplifies the segment targeting heat‑sensitive assemblies — a priority where processing temperatures constrain adhesive selection.

- DELO Industrial Adhesives: Recent product introductions geared to first lens bonding and active alignment underscore an aggressive innovation cadence. DELO’s dual‑cure and UV solutions are directly relevant to manufacturers striving to improve throughput without sacrificing optical integrity.

- MacDermid Alpha: Provider of low‑temperature and UV‑cure adhesives, positioned for assemblies sensitive to thermal stress. MacDermid’s product portfolio and application services make them a natural collaborator for OEMs migrating to tighter optical tolerances.

Taken together, recent company moves — from lease renewals signifying commitment to local manufacturing, to product launches sharpening low‑stress, fast‑cure capabilities — reveal a competitive pattern in 2026: differentiation will be built on integrated solutions (material + process + service) rather than raw chemistry alone.

Industry dynamics that will shape plans in 2026

- Regulatory tightening: The EU’s enhanced chemical disclosure requirements and continuing global RoHS constraints are not merely compliance checkboxes; they materially affect formulations, supplier qualification timelines and go‑to‑market claims. Companies must budget both R&D and documentation resources into 2026 product roadmaps.

- Trade and tariff effects: Elevated duties on imported specialty resins and curing agents have increased landed costs and forced procurement teams to reassess supplier diversification. For 2026 planning, firms should model alternative sourcing, nearshoring and hedging approaches as part of capital and working‑capital scenarios.

- Raw material volatility and labor intensity: Reformulating solvent‑based adhesives to meet VOC and safety standards lifts labor and compliance overhead. Process automation that reduces reliance on manual mixing and handling becomes a tangible route to margin protection.

- Manufacturing and quality imperatives: As active alignment tolerances narrow, adhesives must deliver predictable shrinkage, reliable cure profiles and compatibility with automated dispensing. Facility investments in inline metrology and process control will be an important differentiator in 2026 contracts.

Practical 2026 strategic moves — prioritized

- Invest selectively in dual‑cure and low‑shrinkage chemistries that demonstrably reduce active alignment cycle time — prioritize pilots with high‑volume customers where ROI is shortest.

- Initiate a near‑term sourcing diversification program for specialty resins and curing agents; model duty and lead‑time scenarios and qualify secondary suppliers before H2 2026.

- Embed regulatory resilience: create a cross‑functional REACH/RoHS conversion playbook and assign accountability for documentation turnaround to avoid product launch delays.

- Differentiate via services: bundle formulation with on‑site process engineering, dispensing recipes and yield analytics to move conversations from price to total cost of ownership.

- Pursue bolt‑on acquisitions or strategic alliances to supplement gaps in curing technology or regional footprint rather than large scale roll‑ups; the market concentration profile supports targeted consolidation.

How PW Consulting’s deliverables de‑risk your 2026 choices

Clients using our report gain immediate operational instruments: a scenario‑driven financial model they can plug into corporate planning, supplier scorecards to accelerate procurement decisions, and engineered pilot plans that reduce time‑to‑value for adhesive conversions. For M&A teams, our prioritized target list and synergy models narrow diligence focus; for product and process leaders, our technology maps identify the three chemistry roadblocks most likely to erode yield in 2026.

Concluding counsel — convert insight into leverage

The camera module adhesives market in 2026 will reward firms that convert technical differentiation into manufacturable, compliant solutions and partner closely with assemblers to shorten alignment cycles. The macro growth underpins investment, but structural and regulatory headwinds elevate execution risk. Executives who align R&D, procurement and go‑to‑market motions — and who leverage data‑driven scenario planning — will secure disproportionate share of the profit pool.

PW Consulting’s full Camera Module Adhesives Market report contains the detailed segmentations, company scorecards, and executable playbooks referenced here. For teams preparing capital allocations, R&D roadmaps or M&A pipelines in 2026, the report functions as both a risk‑mitigation tool and a growth accelerator. Visit our website to access the complete study and the interactive forecast model.

For detailed analysis of this topic, please visit the official page:Camera Module Adhesives Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com