Image Capture Cards Market — Strategic Preview for 2026 Decisions

Executive synopsis

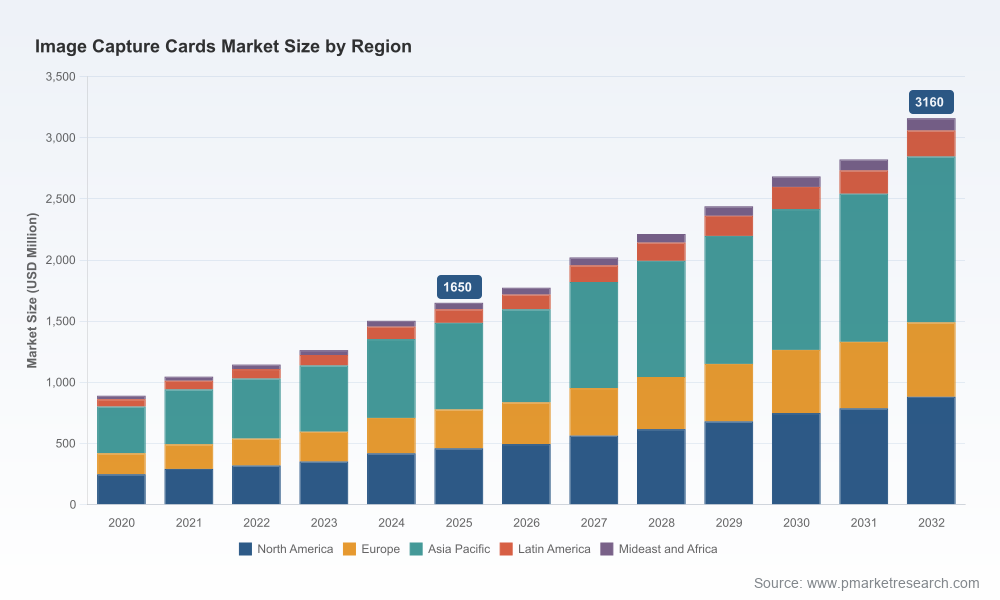

PW Consulting’s latest market study on Image Capture Cards provides an actionable intelligence package designed to inform executive decision-making throughout 2026. Anchored on a 2025 base year and a 2026–2032 forecast window, the research quantifies a market that has expanded materially since 2020 and is expected to maintain near-double-digit growth through the decade. Our topline modelling shows the market more than doubling from its early‑2020 level and tracking at a compound annual growth rate (CAGR) of 9.8% across the forecast period — an environment that creates both opportunity and structural disruption for incumbent vendors, challengers, and enterprise buyers.

Image Capture Cards Market

Market snapshot (select macro figures)

- History and momentum: PW Consulting tracked multi-year growth from the 2020 market base to a robust 2025 market size used as the base year for modelling, reflecting accelerating demand across live content, professional AV, and enterprise imaging workflows.

- Forward view: Under our central case assumptions the market continues to expand through 2032, reinforcing strategic imperatives for capacity planning, channel investment, and product roadmaps.

- Concentration: The market exhibits moderate concentration — our market concentration metrics indicate the top three and top five suppliers hold a material share of industry revenues, a dynamic that shapes competitive behaviors and partner selection strategies.

What the report contains — practical deliverables for 2026 planning

- Granular market architecture: validated market-sizing and growth scenarios by vintage (historic 2020–2025) and forecast (2026–2032) with sensitivity cases tuned to supply‑chain and demand shocks.

- Competitive intelligence: detailed supplier profiles and strategic posture maps, cross-referenced to product roadmaps, channel footprints, and IP positions.

- Commercial playbooks: go-to-market prioritization, price‑to‑value frameworks, and distributor/VAR segmentation to accelerate channel conversion in key verticals.

- Product and R&D guidance: feature-prioritization matrices and time-to-market sequencing calibrated against OEM cost curves and component availability scenarios.

- Risk & resilience diagnostics: a supply-chain heat map, component sourcing alternatives, and a 90‑/180‑day mitigation plan for foundry and ASIC tail risks.

- M&A and partnership scorecards: opportunity screening templates for bolt-on acquisitions, JV constructs, and licensing pathways to capture adjacent value pools.

Why this matters for 2026 corporate choices

Executives entering 2026 face three linked decisions: how aggressively to invest in differentiated capture functionality (higher-performance codecs, low-latency pipelines, hardware-accelerated preprocessing), how to reconfigure supply chains in light of persistent semiconductor tail risks, and how to defend or expand margins under entry-level commoditization pressure. Each choice carries trade-offs in CapEx, time-to-market, and channel economics — and our report translates those trade-offs into quantified scenarios so boards and product leaders can sign off with confidence.

Image Capture Cards Market

Competitive landscape: who to watch

- Magewell (Nanjing, China) — Well-positioned in the professional capture segment with Pro Capture and Eco Capture families across PCIe, USB, and M.2. Recent product cadence signals push into higher-bandwidth inputs; notably, a 2025 product launch introduced a USB Capture SDI 4K Pro device supporting 12G‑SDI and USB 3 Gen 2x2, underscoring an emphasis on low-latency, high‑throughput external capture solutions. Strategic implications: rapid feature refresh cycles, competitive OEM supply relationships, and targeted moves up‑market.

- Datapath (Derby, UK) — Focused on high‑performance multi-channel capture cards (VisionSC, VisionAV, Vision ranges) tailored to complex AV and control-room installations. Strengths include multi-stream synchronization and software-enabled management. Strategic implications: strong fit for enterprise AV suites and verticals that prioritize reliability and multi‑channel scaling.

- Blackmagic Design (Melbourne, Australia) — Known for DeckLink PCIe series able to capture and play back at professional 4K/8K SDI/HDMI specifications. Brand equity and content-creator adoption are core assets. Strategic implications: leverages ecosystems in post‑production and broadcast; competes on end‑to‑end creative workflows rather than purely component pricing.

- Anyoyo (China) — Aggressive at the entry and mid-market with USB capture cards aimed at 4K@60fps gaming and live streaming. Their cost position exerts downward pressure on OEM ASPs in the consumer‑grade tier. Strategic implications: accelerates commoditization at the lower end and forces incumbents to clarify their value differentiation strategies.

Dynamics and risks shaping 2026 outcomes

- Semiconductor and foundry tail risk: component shortages and extended lead times experienced in 2021–2022 remain a structural tail risk. Geopolitical pressure on advanced foundry capacity (notably in Taiwan) introduces meaningful lead‑time and cost volatility for vendors relying on advanced capture ASICs.

- Commoditization from low-cost OEMs: intensified price competition at entry levels compresses margins, forcing Western and branded vendors to accelerate feature differentiation, bundled software, or service monetization to sustain revenue per unit.

- Regulatory fragmentation and data localization: increasing national requirements for data residency and content control complicate architectures for cloud‑based capture and streaming workflows, introducing compliance costs and localized deployment needs for multinational customers.

Strategic playbook — prioritized actions for 2026

Based on scenario modelling and vendor benchmarking, PW Consulting recommends the following priority actions for vendors, enterprise buyers, and investors planning for 2026:

Image Capture Cards Market

- Defend margin via differentiation: Invest selectively in hardware features that unlock monetizable services — e.g., onboard preprocessing, embedded AI inference for frame tagging, and low‑latency passthrough. Combine with software subscriptions for firmware updates, cloud integration, and premium support to shift ASP pressure toward recurring revenue.

- Supply-chain resilience program: Deploy a dual‑sourcing strategy for critical ASICs, maintain safety stock calibrated to product lifecycle stages, and pursue strategic buffer contracts with foundries and distributors. Short‑term: implement a 90‑day component hedging playbook; medium‑term: consider packaging or co‑development agreements to secure capacity.

- Channel and pricing optimization: Re-segment channels by white‑label, pro AV, and creator ecosystems. Use value-based pricing for pro segments and loss‑leader ASPs for entry channels to protect brand equity while curbing low‑margin churn.

- Regulatory-aware architecture: Offer localized firmware builds and enterprise deployment options that honor data localization rules; partner with local integrators where compliance or performance constraints require on‑prem solutions.

- M&A and partnerships: Screen targets that provide complementary software (workflow orchestration, AI analytics) or regional go‑to‑market footprints. For system integrators and broadcasters, consider partnership models that co‑sell hardware subscriptions integrated with managed services.

For enterprise buyers: procurement and risk checklist for 2026

- Prioritize suppliers with transparent supply‑chain mapping and contingency plans for ASICS and connectors.

- Negotiate SLAs that reflect component scarcity; require commitments around security patches and firmware support horizons.

- Favor modular architectures that allow incremental upgrades (e.g., external USB/Thunderbolt modules) to reduce CapEx risks tied to rapid format shifts.

What’s behind our projections — methodology highlights

PW Consulting’s forecasts synthesize bottom‑up SKU-level shipment modelling, proprietary channel checks, and buyer-interview insights across broadcast, streaming, gaming, medical imaging, and enterprise AV verticals. We stress‑tested market trajectories under alternative scenarios (supply‑driven contraction, accelerated cloud migration, and rapid commoditization) to quantify strategic break‑points. To preserve the value of our primary research, this briefing intentionally omits the granular regional and application splits that are included in the full report; those tables are essential for revenue planning and partner prioritization and are available in the paid release.

Conclusion — the strategic edge for 2026

The Image Capture Cards market presents a classic inflection: growing demand and technical complexity create room for premiumization, but persistent supply-chain fragility and low‑cost competition compress traditional hardware margins. For leaders, the priority in 2026 is to convert growth into durable profitability by aligning product innovation, supply‑chain resilience, and commercial model transformation. PW Consulting’s report provides the diagnostic mapping and executable playbooks to support those decisions — from boardroom scenario planning to product‑line prioritization and M&A screening.

Next steps

For full access to the complete dataset, regional and application splits, supplier scorecards, and the executable 90‑/180‑day playbooks referenced above, request the full Image Capture Cards Market report on the PW Consulting website. The full report contains the proprietary tables and appendices that enterprise procurement, product management, and corporate development teams will require to finalize their 2026 budgets and strategic milestones.

For detailed analysis of this topic, please visit the official page:Image Capture Cards Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com