PW Consulting: Food Cans Market — 2026 Strategic Brief for Executive Decision-Makers

Executive summary

As global food systems continue to balance resilience, cost pressure and sustainability, the food cans market has entered a period of steady but structurally significant change. PW Consulting’s new Food Cans Market report (base year 2025; historical 2020–2025; forecast 2026–2032) quantifies that evolution and converts it into operational guidance for C-suite and functional leaders preparing plans for 2026 and beyond.

Food Cans Market

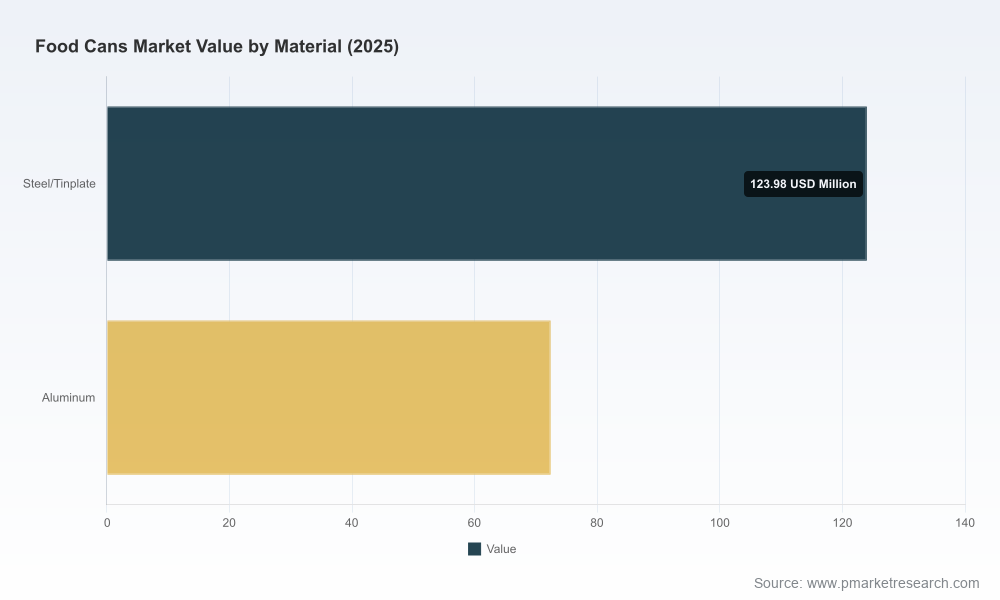

At a macro level, the market expanded from approximately 160 Million USD in 2020 to roughly 196.37 Million USD in 2025 and is projected to reach some 240.53 Million USD by 2032 under our central scenario — an implied compound annual growth rate (CAGR) of 2.89% over the forecast horizon. These headline numbers frame a market that is mature, capital-intensive and increasingly sensitive to raw-material cycles, regulatory shifts and end-user product innovation. Our report is designed as a decisioning tool: it builds forward-looking scenarios, operational playbooks and prioritized action items for 2026 investment and commercial cycles — without giving away the fine-grain splits that subscribers obtain from our primary datasets.

Food Cans Market

Why 2026 is a strategic inflection point

- Regulatory reframing: Regulators are actively reshaping how canned foods are defined, labeled and traced. The FDA’s 2025 revocation of certain longstanding standards of identity, the extension of FSMA Rule 204 traceability deadlines to July 2028, and state-level mandates such as California’s AB 660 (standardized quality or safety dates effective July 2026) raise both compliance costs and shelf-communication requirements for manufacturers and packagers.

- Input-cost volatility: Tariff policy and metal markets are altering the cost calculus for tinplate and aluminum. Section 232 tariffs on tinplate steel imports remain in force, and tin prices surged more than 25% since the start of 2026, increasing pressure on producers that rely on imported tinplate and weakening historical cost advantages.

- Product & material evolution: Advances in coating technologies and aluminum processing are shifting technical trade-offs. The market continues to balance traditional steel/tinplate offerings with aluminum alternatives for specific formats (retort, two-piece) — with coatings, closure systems and shelf-life solutions becoming differentiators.

- Consolidation dynamics: Concentration metrics indicate material market power among top players, presenting both risk and opportunity for mid-market manufacturers and private equity seeking roll-up potential.

Key strategic imperatives for 2026

Our analysis translates market trends into a set of prioritized, actionable imperatives that belong in every 2026 strategic plan for players across the value chain.

Food Cans Market

- Hedge procurement and diversify sourcing: Implement multi-supplier contracts, indexed pricing collars and strategic inventory buffers for tinplate and key alloys. Scenario-model the impact of tariffs and a continuation of elevated tin prices on gross margins and pass-through strategies.

- Adopt a dual-material product playbook: Where technical and commercial trade-offs allow, maintain both steel/tinplate and aluminum manufacturing or partnerships to serve distinct product platforms and customer requirements; invest selectively in tooling that can be repurposed across formats.

- Capitalize on coatings and closures as value levers: Coating innovations and easy-open end technologies are becoming commercial differentiators. Prioritize partnerships with innovative coil-coating suppliers and accelerate trials for next-gen internal coatings designed for pet food and retort applications.

- Embed traceability and labeling capabilities now: With FSMA Rule 204 timelines extended but enforcement certainty increasing, invest in traceability systems (item-level, batch linking) and prepare labeling templates that comply with AB 660 and evolving federal guidance.

- Refine go-to-market segmentation: Re-evaluate account-level economics by overlaying can-format profitability, regulatory exposure and distribution complexity; adopt value-selling for customers seeking sustainability credentials or extended shelf life.

- Target M&A and partnerships strategically: The market’s top concentration levels create payoffs for bolt-on acquisitions that provide geographic diversification, capacity for aluminum formats, or specialty coating capabilities. Build an M&A scorecard that prioritizes synergies under raw-material stress-test scenarios.

- Move on sustainability with pragmatism: Invest in circularity where it aligns with customer willingness-to-pay and regulatory direction (e.g., recycled content, lightweighting) while quantifying short-term cost impacts and longer-term competitive value.

Competitive landscape — who matters and why

The market is led by a mix of global metal-packaging giants, regional manufacturers and specialized domestic players. PW Consulting’s report maps the competitive positions, capability footprints and likely strategic moves for the leading names — enabling acquirers, OEMs and commercial teams to prioritize engagements for 2026.

- Crown Holdings, Inc. (Atlanta, Georgia, United States) — Produces food cans and closures alongside beverage cans, with North American tinplate operations focused on food and aerosol applications. https://www.crowncork.com

- Silgan Holdings Inc. (Stamford, Connecticut, United States) — Major manufacturer of metal cans for food and beverage packaging, including food-specific lines. https://www.silgan.com

- Ardagh Group (Dublin, Ireland) — Produces steel and aluminum food cans, with a strong presence in food and beverage metal packaging. https://www.ardaghgroup.com

- Ball Corporation (Westminster, Colorado, United States) — A leader in aluminum cans including retort and two-piece food cans for various food categories. https://www.ball.com

- Toyo Seikan Group Holdings, Ltd. (Tokyo, Japan) — Global producer of food cans and metal packaging solutions. https://www.toyo-seikan.co.jp/e/

- CPMC Holdings Limited (Hong Kong, China) — Major supplier with deep reach in Asia and export markets. https://www.cpmc.com.cn/

- Can-Pack Group (Poznań, Poland) — Produces steel and aluminum food cans for global markets. https://www.canpackgroup.com

- Kaira Can Company Limited (Mumbai, India) — Indian manufacturer with capabilities focused on domestic and export opportunities. https://www.kairacans.com

- Nampak Limited (Johannesburg, South Africa) — Provides food and beverage cans across Africa and international markets. https://www.nampak.com

- Independent Can (United States) — US-based producer of food cans with a focus on domestic manufacturing. https://independentcan.com

Recent industry moves highlight tactical shifts that matter to 2026 planning. Notably, a major coatings supplier launched an aluminum coil-applied non-intentional PVC-NI coating specifically engineered for pet food cans and easy-open ends in the U.S. (April 2026), signaling supplier-driven margin opportunities and formulation differentiation. Regional players are also active on the trade-show circuit to showcase packaging innovations and new product formats (e.g., Independent Can at Pack Expo International, Chicago, February 2026).

Report contents — what you will get and why it matters

PW Consulting’s Food Cans Market report is organized for pragmatic use by strategy, procurement, commercial and M&A teams. Key deliverables include:

- Market sizing and three scenario forecasts (baseline, downside, upside) for 2026–2032 with sensitivity analytics.

- Supply-chain stress tests modeling tariffs, commodity shocks (tin, aluminum) and logistics disruptions.

- Regulatory impact matrix summarizing compliance pathways, timeline implications (including FSMA 204 and AB 660) and labeling risk maps.

- Competitive playbooks for leading and challenger firms, including capability maps, customer exposure overlays and likely strategic moves.

- M&A & partnership scorecards highlighting targets and synergy estimates under different price scenarios.

- Commercial optimization tools: price-pass mechanisms, product-mix optimization and channel-specific go-to-market tactics.

- Operational checklists for coatings selection, easy-open end adoption, and quality systems aligned with extended traceability requirements.

- An interactive Excel model with the assumptions and drivers underlying our headline forecasts (subscriber access required for segment-level detail).

Methodology and confidence

The report combines primary interviews with manufacturers, suppliers and brand owners; trade data; proprietary MOQ-adjusted capacity models; and price and tariff scenarios. The base year is 2025, with a historical review covering 2020–2025 and a forecast window of 2026–2032. We model a central CAGR of 2.89% for the forecast period and provide transparent sensitivity ranges tied to tin and aluminum price trajectories, tariff scenarios and regulatory compliance timelines.

How to use this intelligence in 2026 planning

- Embed the report’s scenario outputs into your 2026 budget and five-year strategic plan rather than relying on single-point forecasts.

- Make procurement decisions contingent on hedging outcomes and real options analysis (do not assume permanent low-cost access to tinplate).

- Prioritize short-term investments that unlock optionality (cross-format tooling, coating compatibility trials) over irreversible, highly specialized capacity spending.

- Use the competitive playbooks to identify counterparty risk and to structure M&A bids that reflect integration costs under stressed raw-material scenarios.

Final note — a trailer, not the feature

PW Consulting’s public briefing is intended to preview the depth of analysis available in the full Food Cans Market report. We have deliberately shown our macro market sizing, growth trajectory and strategic line-of-sight while reserving detailed segment-by-segment data, proprietary company scorecards and downloadable models for report subscribers. For procurement directors, corporate strategy leads and private equity teams planning activity in 2026, the full report provides the executable evidence base to act with conviction.

To request the full report, data extracts or to schedule a briefing with our senior industry analysts, visit PW Consulting’s report page or contact our Food & Beverage Packaging practice. Make 2026 the year your organization converts packaging risk into competitive advantage.

For detailed analysis of this topic, please visit the official page:Food Cans Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com