Next-Generation Advanced Batteries Market: Strategic Preview for 2026 Decision-Makers

PW Consulting’s new market study — Next-Generation Advanced Batteries Market (base year 2025, forecast 2026–2032) — equips senior executives, investors, and policy teams with the strategic intelligence required to convert technological promise into commercial advantage. This executive preview highlights the report’s strategic value for 2026 corporate planning cycles, summarizes headline macro trajectories, and sketches the competitive and policy dynamics shaping near-term commercialization pathways. To preserve the commercial integrity of our proprietary segment models, this release purposefully omits granular segment-level data; the full dataset, models, and playbooks are available in the complete report.

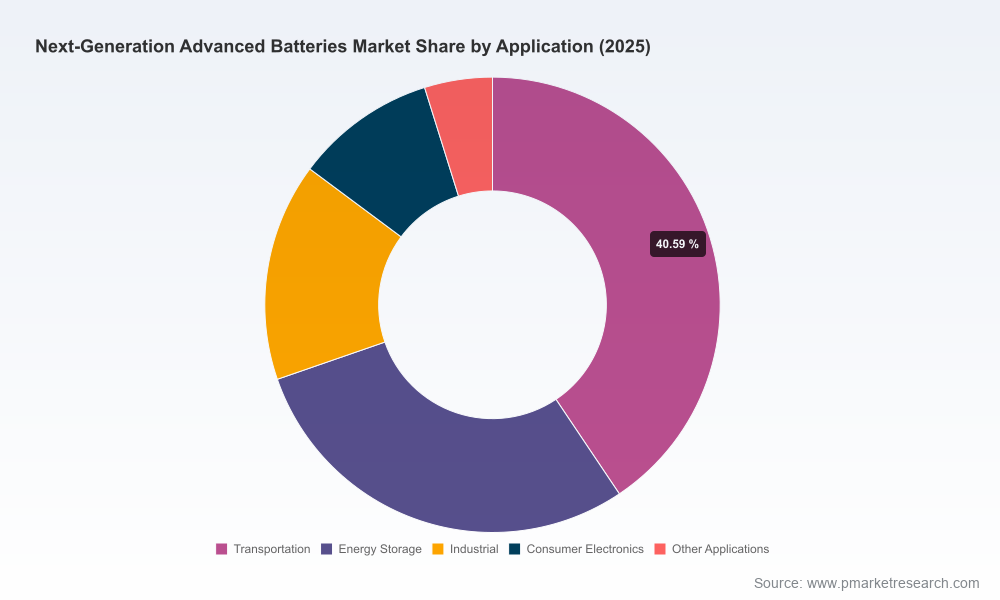

Next-Generation Advanced Batteries Market

Market Snapshot: Trajectory and Scale

Advanced battery innovations have moved from laboratory promise to near-commercial reality. Our market model, anchored on a 2025 base year, shows the total addressable market rising from an estimated USD 201.5 Million (revenue unit: Million) in 2025 toward a materially larger market by 2032, with a compound annual growth rate (CAGR) of 7.1% across the 2026–2032 forecast window. Historical growth since 2020 has already been robust — from roughly USD 130 Million in 2020 to USD 201.5 Million in 2025 — reflecting accelerating product-development investments, pilot production scale-up, and early fleet and grid demonstrators. Under our central forecast, the market reaches the low-to-mid hundreds of millions by the end of 2032, reflecting staged commercialization of solid-state, metal‑air, lithium‑sulfur, sodium-based chemistries, and other next‑generation approaches.

Next-Generation Advanced Batteries Market

Concentration metrics indicate a market where established and emerging pure‑play technology leaders exert meaningful control: the top three players collectively command roughly two‑thirds of identifiable market revenues (CR3 ~68%), while the top five approach three‑quarters (CR5 ~75%). That structure presents both entry barriers and partnership opportunities for new entrants and incumbent battery and OEM players.

Next-Generation Advanced Batteries Market

Why This Report Matters for 2026 Decision Cycles

- Investment prioritization: With major companies moving from pilots to pilot‑lines and gigafactory commitments, 2026 is the inflection year for capital allocation. The report quantifies break‑even horizons and capital‑intensity thresholds for different manufacturing archetypes, enabling CFOs and corporate development teams to size investments with greater confidence.

- Technology roadmap alignment: Product and platform leaders need to choose which chemistries to fast‑track, partner on, or hedge. Our analysis links lab metrics (cycle life, energy density, rate capability) to manufacturability indicators and time‑to‑revenue scenarios, creating an actionable technology prioritization framework.

- Supply chain and sourcing strategy: The U.S. and global capital commitments — including announced manufacturing pipelines and federal incentives — are reshaping raw‑material and equipment markets. The report provides supply‑side stress tests and sourcing playbooks that fit corporate procurement and strategic sourcing timelines for 2026–2028.

- Regulatory and standards navigation: A rapidly evolving regulatory environment (including incentives under major infrastructure and climate legislation) will be a determinant of regional competitiveness. Our policy scenarios translate regulatory levers into valuation and commercialization impacts for projects initiated in 2026.

What’s Inside: Practical, Decision‑Grade Deliverables

The report is designed as a playbook for action, not a theoretical overview. Key deliverables include:

- Proprietary market sizing and six‑scenario forecasts (2026–2032) by chemistry, application, and commercialization stage, with sensitivity to capex and material price volatility.

- Technology readiness and manufacturability heatmaps that translate lab metrics into production risk scores and scaled‑up cost trajectories.

- Supply chain network maps for critical inputs (anodes, electrolytes, ceramic separators, cell assembly equipment) and risk indices by region and supplier category.

- Capital expenditure modeling for pilot lines, gigafactories, and retrofit pathways, with modeled payback periods and unit economics under multiple demand scenarios.

- Competitive intelligence dossiers on more than 30 firms, including strategic positioning, IP posture, partnership pipelines, and M&A candidate scoring.

- Commercialization playbooks for OEMs, system integrators, and utilities (go‑to‑market strategies, procurement templates, and validation roadmaps).

- Policy and incentives compendium with a scenario matrix showing how incentives, tariffs, and standardization influence project NPV and localisation strategies.

Competitive Landscape: Players to Watch and Strategic Implications

The 2026 commercial environment is being defined by a mix of pure‑play innovators, incumbent battery OEMs, and emerging system integrators. Our competitive analysis focuses on the strategic choices these organizations are making and the implications for partners, investors, and rivals.

- Solid Power (Louisville, CO): Focused on all‑solid‑state lithium‑metal batteries for EVs and energy storage, Solid Power’s partnerships with OEMs position it as a candidate for vehicle platforms that prioritize safety and energy density improvements. Strategic implication: OEMs seeking tighter integration should evaluate equity or JV structures that accelerate cell validation timelines.

- QuantumScape (San Jose, CA): Recent cell validation achievements (Eagle Series achieving 1,000‑cycle validation at automotive discharge rates on a major OEM platform) indicate acceleration toward automotive qualification. Strategic implication: OEMs and Tier‑1 suppliers should assess interface agreements for thermal management and system integration now, before supplier capacity tightens.

- Enovix (Fremont, CA): Offering high‑energy 100% active silicon‑anode lithium‑ion cells, Enovix represents an intermediate risk/reward profile for customers seeking near‑term performance gains without the full manufacturing reinvention required by ceramic solid electrolytes.

- SES AI and Factorial Energy (Boston & Woburn, MA): Both pursing lithium‑metal and solid‑state approaches with a focus on manufacturability and cell architecture advances. Strategic implication: Tier‑1 battery materials and equipment suppliers should consider co‑development agreements to lock in scale‑up learning curves.

- ProLogium Technology (Taoyuan, Taiwan): ProLogium’s announced 6 GWh gigafactory in Europe signals a push to localize production and secure offtake. Strategic implication: Regional utilities, OEMs, and local governments should calibrate incentive capture strategies and grid readiness for factory ramp.

- Ambri, Blue Solutions (Bolloré), Natrion, Peak Energy: These firms exemplify the diversification of approaches — from molten‑salt long‑duration storage to lithium‑metal polymer and sodium‑ion grid solutions. Strategic implication: Utilities and system integrators should adopt a portfolio approach to storage procurement rather than a single‑chemistry bet.

Dynamics Shaping 2026 Commercial Choices

Several macro drivers will determine which technologies and strategies succeed over the next 12–36 months:

- Capital formation and industrial policy: Governments and corporates have announced substantial commitments — including a multi‑hundred‑billion pipeline of manufacturing investment and dedicated federal funding for next‑generation technologies — that are now being translated into pilot lines and factory briefs. These flows materially reduce execution risk for projects that secure offtake and policy alignment.

- Material and capacity buildout: Announced cell manufacturing pipelines measured in the low thousands of GWh globally are reshaping upstream raw‑material demand and creating strategic bottlenecks for specific precursor chemistries. Firms that lock long‑term contracts or verticalize critical steps will gain a durable cost advantage.

- Standards and commercialization milestones: As pilot production moves toward commercial lines — with dozens of pilot facilities in operation by 2025 and new roadmaps for solid electrolytes in 2026 — standardization and validation protocols will become gating factors for OEM qualification and regulatory acceptance.

- Technology maturity differences: Solid‑state, sodium‑ion, and metal‑air chemistries sit at different points on the maturity curve. Strategic plays that mix near‑term, de‑risked chemistries with targeted bets on transformative options will yield balanced portfolios for corporates and investors.

How Executives Should Use This Report in 2026

- Board briefings and capital requests: Use the report’s capex and commercialization timelines to stress‑test business cases presented to boards and investors.

- M&A and partnership screening: Apply our competitive scoring to prioritize targets for acquisition, minority investment, or JV with clear criteria tied to manufacturability and IP defensibility.

- Procurement and sourcing strategy: Implement the supply‑chain playbooks to secure tiers‑1 and critical‑materials contracts that align with project ramp milestones.

- Policy engagement: Leverage the policy scenario outputs to design lobbying and local‑content strategies that maximize incentives while minimizing execution risk.

Conclusion and Next Steps

2026 is the pivotal year in which pilots, pilot‑lines, and nascent gigafactories will determine which technologies move from promising to profitable. PW Consulting’s Next‑Generation Advanced Batteries Market report synthesizes market sizing, technology readiness, supply‑chain realism, and policy dynamics into decision‑grade guidance. It is designed to accelerate intelligent capital allocation, reduce execution risk, and pinpoint strategic partners for commercialization.

For detailed segment models, full company dossiers, interactive scenario tools, and proprietary datasets that underpin the analyses summarized here, access the complete report on our website. PW Consulting’s team is also available for bespoke briefings, scenario workshops, and board‑level strategy sessions to translate these insights into operational plans for 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Next-Generation Advanced Batteries Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com