RTA Kitchen Cabinet Market 2026: Strategic Readiness Notes from PW Consulting

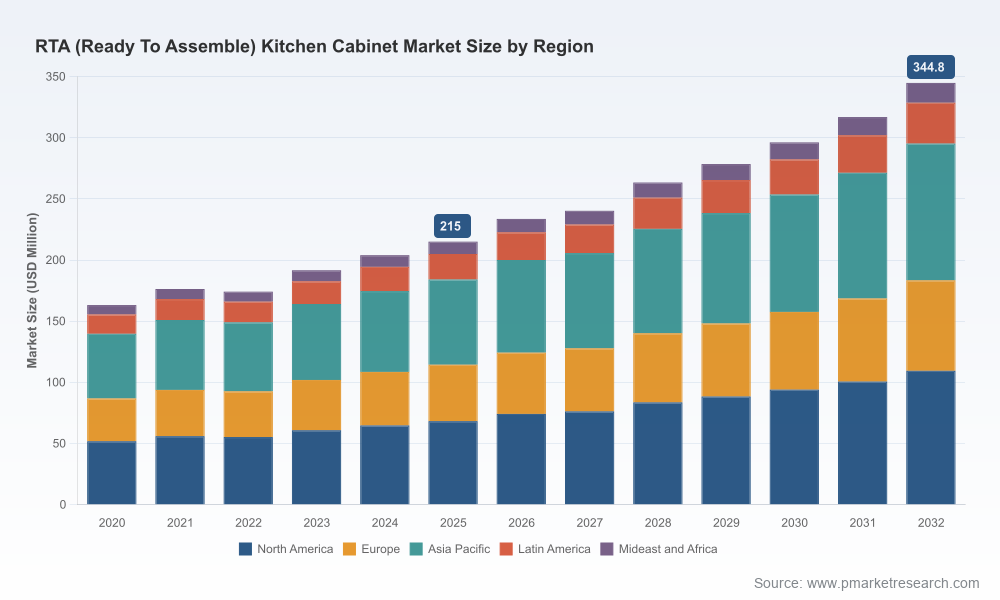

The Ready-To-Assemble (RTA) kitchen cabinet market is entering 2026 on a trajectory that demands decisive, data-led strategic moves. PW Consulting’s newest market study — with a 2025 base year and a forecast window through 2032 — shows the sector recovering and expanding from the pandemic-era volatility, growing from an estimated USD 163.15 million in 2020 to USD 215.0 million in 2025, and projected to reach roughly USD 344.8 million by 2032. That path represents an expected compounded annual growth rate of approximately 5.67% across the forecast window, a rate that is neither hypercompetitive nor stagnant: it signals steady expansion with pockets of disruptive opportunity.

RTA (Ready To Assemble) Kitchen Cabinet Market

Why this report matters for 2026 decision-makers

- It converts headline growth into executable strategy. The macro trajectory is clear; our study translates it into sourcing, pricing, and channel playbooks designed for the constraints and levers that will matter in 2026.

- It anticipates regulatory and tariff moves that will materially affect gross margins and sourcing choices in the coming 12–24 months.

- It exposes where product innovation, service differentiation, and distribution excellence most effectively capture market share in a fragmented competitive landscape.

What the PW Consulting RTA report delivers (practical contents)

- Market sizing and validated five-year historicals (2020–2025) plus a detailed forecast (2026–2032) with scenario-adjustable models for conservative, base, and upside cases.

- Demand-driver diagnostics: renovation cycles, new-build activity proxies, consumer-price sensitivity elasticities, and builder/developer procurement behaviors.

- Supply-side analysis: manufacturing footprints, imported kit exposure, landed cost modeling, and logistics-through-assembly time studies.

- Regulatory and trade-impact frameworks: tariff-sensitivity matrices and playbooks for duty mitigation, vertical integration, and nearshoring scenarios.

- Competitive benchmark decks: product, pricing, and go-to-market profiles for leading and emerging players, plus CR analysis to quantify concentration and competitive intensity.

- Actionable go-to-market guides: channel segmentation for retail, wholesale, and builder channels; SKU rationalization templates; dealer/developer program blueprints; and digital conversion levers.

- M&A and partnership heatmaps identifying targets and strategic fits by capability gaps, geographic footprint, and cost-to-serve synergies.

Market dynamics to watch in 2026

- Tariff environment and import risk: The industry’s import exposure is increasingly material. Recent measures and proposed tariff escalations have introduced step-changes in landed costs — notably through tariff actions tied to specific HTSUS categories and staged ad valorem increases. These moves force urgent re-evaluation of sourcing strategies for any firm with significant imported components or finished kits.

- Quality and certification as a competitive moat: Industry standards such as the KCMA A161.1 quality certification are shifting from ‘nice-to-have’ to commercial differentiators. Certification drives purchaser confidence among trade buyers and can justify price premiums in distribution channels that prioritize durability and warranty.

- Product and finish innovation: Consumer taste cycles are accelerating around contemporary shaker variants, painted-wood finishes, and frameless lines. Companies that codify rapid product introduction cycles — while maintaining assembly simplicity — will capture specification share among builders and remodelers.

- Channel bifurcation and service expectations: End customers now expect integrated digital ordering, precise lead-times, and clear labor/assembly guidance. Firms that pair product breadth with superior order-to-install experiences will outcompete those relying solely on price.

- Operational margin pressure: Given the expected growth rate, winners will be those that retain margin through procurement sophistication, supply-chain hedging, and SKU rationalization rather than volume alone.

Competitive landscape: what leading players are doing

The market remains fragmented: our concentration analysis shows modest top-player shares, which creates both competitive intensity and acquisition opportunity. The present CR3 and CR5 metrics indicate a sector where scale advantages are present but not decisive — meaning differentiation and operational excellence matter more than sheer size.

RTA (Ready To Assemble) Kitchen Cabinet Market

- ProCraft Cabinetry — positioning and product leadership: ProCraft’s recent activity, including a high-profile presence at KBIS 2026 and a relaunch of a frameless line with refreshed finishes and a new brand identity, signals a move to couple design leadership with channel visibility. Their strategy exemplifies how trade-show-driven brand refreshes can accelerate specification adoption among dealers and designers.

- Cabinet City — inventory and wholesale focus: With a new catalog emphasizing stocked assortments for builders and developers, the company highlights a tried-and-true path: marrying in-stock availability to speed-to-site can win volume business where assembly-labor scarcity matters.

- Kavalan Cabinetry, American Made Cabinets, and 10% Cabinetry — service and niche plays: These firms illustrate differentiated plays — contractor-focused distribution, cost-positioning, or regional dealer networks. Their active dealer programs and fulfillment propositions are instructive for companies weighing whether to prioritize channel depth over broad national presence.

Strategic implications and recommended moves for 2026

Companies that treat 2026 as a year to lock in defensible economics while positioning for medium-term growth will outperform. The following framework is designed for executives making capital allocation, sourcing, and market-entry decisions this year.

RTA (Ready To Assemble) Kitchen Cabinet Market

- Immediate (0–12 months)

- Run tariff-impact stress tests on all product lines: quantify the margin delta under current and escalated duty scenarios and model pass-through thresholds for different distribution channels.

- Accelerate KCMA or equivalent quality certification for high-volume SKUs to protect price realization and reduce return/rework costs.

- Prioritize SKU rationalization in low-turn assortments to free working capital and reduce storage/transport complexity.

- Secure short-term logistics and labor flex: hedge container and pallet capacity and shore up assembly-labor partnerships (contractors, installation networks).

- Medium-term (12–36 months)

- Pursue localized manufacturing or nearshoring pilots for duty-sensitive SKUs — small-capex, high-frequency lines can be the fastest path to landed-cost parity.

- Invest in digitization of order-to-assembly workflows (3D configurators, BOM exportability, digital instructions) to reduce friction for both pro and DIY segments and to capture aftermarket revenue.

- Evaluate bolt-on M&A to secure distribution footprints or complementary manufacturing capacity; targets should unlock measurable synergies in procurement, fulfillment, or product breadth.

- Design premium service bundles (installation warranties, accelerated lead-times, finished hardware packs) to create margin-dense revenue streams less sensitive to commodity price swings.

How PW Consulting’s RTA study accelerates implementation

- Scenario-ready financial models. Pre-built sensitivity models let you test tariff outcomes, cost inflation, and demand shifts against the report’s base forecast and alternate cases.

- Supply-chain mapping and supplier scorecards. Detailed supplier profiles, cost-to-serve matrices, and contingency playbooks support rapid decision-making for nearshoring or supplier diversification.

- Channel and product playbooks. Practical templates for dealer programs, builder/developer partnerships, and SKU rollouts reduce time-to-execution for commercialization initiatives.

- Competitive intelligence appendices. While our public summary highlights trends, the full package contains granular competitor profiles, recent product launches, and trade-show intelligence that inform positioning and product timing.

- M&A diligence accelerants. Deal-room-ready materials: valuation comparables, integration risk matrices, and synergies calculators tailored to the RTA space.

Next steps

For executives planning capital allocation, commercial strategy, or supply-chain redesign in 2026, the choice is between reacting to tariff and product shocks or shaping outcomes with a defensible playbook. PW Consulting’s RTA Kitchen Cabinet report synthesizes the macro growth pathway and the levers that change the odds in your favor.

To access the full dataset, segmented scenarios, and the tactical annexes that contain detailed competitor benchmarking and the regulatory impact matrices, please visit our report page. The public briefing you’ve read is intentionally selective — it surfaces the strategic implications and next-step frameworks while reserving the granular tables and forecast-by-segment files for licensed report subscribers who require transaction-grade intelligence.

For detailed analysis of this topic, please visit the official page:RTA (Ready To Assemble) Kitchen Cabinet Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com