Magnetron Market 2026: Strategic Imperatives from PW Consulting’s Magnetron Market Report

Executive teaser

As organizations prepare strategic moves in 2026, magnetron technologies—long the backbone of microwave heating, industrial processing, radar and select medical systems—are entering a new phase of market maturity and application-driven expansion. PW Consulting’s Magnetron Market report (base year 2025) synthesizes five years of historical analysis (2020–2025) with a detailed forecast window for 2026–2032. Our model projects a compound annual growth rate (CAGR) of 7.25% across the forecast period, driven by sustained demand in appliance and industrial segments, higher-power industrial and defense applications, and increased adoption inside semiconductor and medical equipment manufacturing. The total market, which PW tracks on an annual basis, shows clear acceleration from the mid-cycle level observed in 2025 into a multi-year upswing through 2032.

Magnetron Market

Why this report matters for 2026 corporate decisions

- Capital allocation: quantitative scenarios and sensitivity analysis make it straightforward to size near-term R&D and capacity investments under distinct demand and regulatory outcomes.

- Supply chain strategy: granular supplier mapping and tiered risk scoring enable procurement teams to prioritize dual-sourcing, inventory hedging, and local footprint choices that reduce lead-time and quality risk.

- M&A and partnerships: our competitive-mapping and valuation heuristics identify assets likely to produce scale benefits or technology synergies within 12–36 months.

- Product portfolio decisions: evidence-based roadmaps support decisions on continuous-wave vs pulse magnetron development, thermal management investments, and modular integration for OEM partners.

- Regulatory compliance and certification planning: practical checklists and timelines de-risk product launches in regulated end-markets, including medical and defense.

What the report contains — practical, operational intelligence

This is not a high-level narrative. PW Consulting’s Magnetron Market report delivers executable intelligence for commercial teams and corporate boards, including:

Magnetron Market

- Market sizing and methodology with transparent assumptions (base year 2025; historical 2020–2025; forecast 2026–2032).

- Demand-driver frameworks and scenario-models calibrated to macroeconomic, end-market adoption, and regulatory inputs.

- Technology and product roadmaps distinguishing continuous-wave and pulsed magnetron adoption paths, thermal and EMI design constraints, and system-integration best practices.

- Supplier landscape and a proprietary vendor scorecard covering technology capability, capacity flexibility, quality certifications and OTD (on-time delivery) performance.

- Go-to-market playbooks for OEMs and subsystem integrators, including commercial negotiation templates and cost-to-serve analytics.

- Risk heatmaps and mitigation templates for supply shock, regulatory change, and component obsolescence.

- M&A playbook with valuation multiples, integration checklists and post-acquisition value-capture levers.

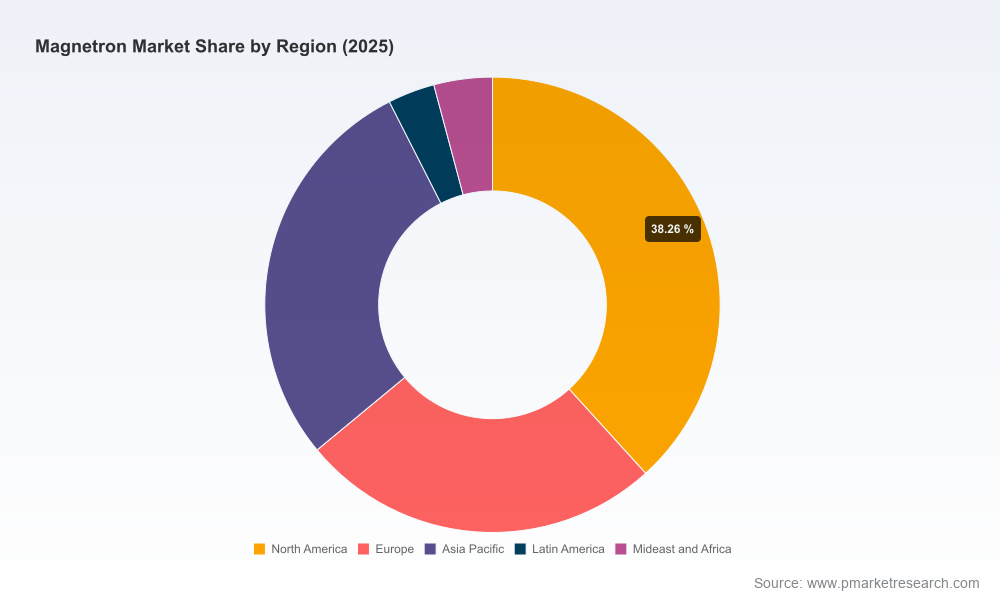

To preserve commercial value for clients, the report carefully withholds granular regional or application split figures in public summaries; full segmentation tables, line-level forecasts, and vendor-level share estimates are available in the complete report download.

Magnetron Market

Market dynamics shaping 2026 planning

Three structural dynamics will determine winners and losers in the next 18–36 months:

- Regulatory and standards pressure: Stricter emissions and electromagnetic compatibility rules affect device form factors and BOM cost. Compliance-driven design choices—such as EMI shielding and forced-air cooling for higher-power units—are increasing system complexity and can add material and assembly cost pressure for compact systems.

- Power-density and thermal management: Continuous operation beyond defined power thresholds requires more sophisticated cooling strategies and thermal materials. These constraints are influencing platform choices in portable and compact industrial deployments.

- Cross-domain adoption: Magnetron use in semiconductor plasma systems, medical radiation platforms and radar continues to grow. These high-value applications impose more stringent reliability, qualification and certification demands, creating opportunities for vendors that can demonstrate controlled production and documented compliance.

Regulatory and infrastructure context — actionable takeaways

- FCC equipment authorization and EMI limits materially affect enclosure and shielding budgets; procurement teams should assume an added cost delta for compact, tightly packaged systems.

- Engineering teams must account for compulsory cooling strategies when designing systems with sustained high-power magnetrons—this influences enclosure design, serviceability and total installed cost.

- Medical device approvals continue to evolve. Recent clearances underscore that magnetron-based therapies and platforms can meet regulatory equivalence pathways, but manufacturers must plan for documentation and validation cycles consistent with medical device timelines.

- Infrastructure adoption is visible: millions of magnetron components are already embedded across radar, medical and industrial systems, with hundreds of thousands integrated into advanced semiconductor tools—this creates both scale opportunities and concentrated supplier risk.

Technology and product trends to watch

- Energy efficiency and application-specific magnetron tuning are now front-and-center. Recent product advancements in food processing illustrate how uniformity and reduced cycle times can become differentiators.

- Integration of active thermal management and smart diagnostics is emerging as a must-have for industrial and medical systems aiming to deliver uptime guarantees.

- Modular subsystem approaches—where magnetrons are delivered as integrated modules with standardized mechanical, electrical and cooling interfaces—are reducing OEM integration costs and accelerating time-to-market.

Competitive landscape — positioning and near-term implications

The magnetron market exhibits moderate concentration. Our concentration metrics indicate that the top three players account for a meaningful but not overwhelming share of the market, with the top five nearly half of global supply. This structure allows scale players to protect margins through volume and integrated systems capabilities, while mid-market and regional players compete on customization, cost and proximity to OEMs.

Below is a concise strategic read on core vendors featured in the report:

- Communications & Power Industries (CPI) — Strong in high-power, defense-grade and industrial microwave components; attractive for partners seeking robust quality systems and long-term defense contracts.

- Toshiba Hokuto Electronics — Deep specialization in industrial magnetrons and appliance components, with long-standing compliance and engineering pedigree for demanding electrical specifications.

- LG Electronics — Leverages appliance-scale manufacturing and brand channels to drive volume in household and commercial appliance segments; potential to scale industrial offerings through system integration.

- Panasonic Corporation — Focuses on continuous-wave products for industrial and HVAC applications; capability in integrated solutions is a competitive advantage for large OEMs.

- Samsung Electronics — Household and emerging industrial systems play, supported by strong supply-chain integration and consumer channel reach.

- Hitachi Ltd. — Supplies industrial heating and drying magnetrons; well positioned to capture demand in processing and manufacturing systems that require industrial-grade reliability.

- Teledyne e2v — Specializes in medical and high-reliability applications; its European footprint and technical depth make it a go-to for regulated end-markets.

- Kunshan GuoLi (GLVAC) — Chinese OEM with strengths in vacuum electronic devices; competitive on cost and regional responsiveness for Asian supply chains.

- Midea Group & Galanz Group — Large appliance manufacturers that integrate magnetron production into their appliance value chains, exerting pricing pressure and ensuring secure supply for consumer markets.

Recent market moves — indicators of strategic direction

- Significant funding into high-power microwave systems indicates intensified activity at the defense and industrial convergence—capital inflows are enabling scale deployments and accelerated product roadmaps.

- Targeted equity infusions and MoUs among subsystem suppliers show an emphasis on achieving module-level integration and localization for critical systems.

- Acquisitions by industrial conglomerates have consolidated certain high-power production capabilities, suggesting future bundling opportunities between magnetron components and motion/control or thermal management systems.

- Product launches focused on processing speed, uniformity and energy efficiency signal that incremental product differentiation will increasingly influence purchasing decisions.

Strategic recommendations for 2026

- Procurement and Engineering alignment: Synchronize sourcing timelines with product qualification cycles. Build supplier scorecards that weight regulatory compliance and thermal-management capabilities more heavily than price alone.

- Modular product strategy: For OEMs targeting shorter time-to-market, prioritize partnerships with suppliers offering integrated magnetron modules and standardized interfaces.

- M&A and JV playbook: Target tuck-in acquisitions that accelerate thermal, EMI or continuous-wave expertise rather than broad horizontal consolidation. Consider minority strategic investments to secure capacity in constrained subsegments.

- Regulatory-first design: For medical and defense-adjacent projects, front-load certification planning and validation—this reduces late-stage rework and shortens commercialization timelines.

- Scenario planning: Use our 2026–2032 forecast scenarios to stress-test capital plans under alternative adoption and regulatory environments; preserve optionality for capacity scaling.

How executives should use this report

- Board and investment committees: Use the report’s scenario outputs to align capital deployment with downside protections over a multi-year horizon.

- Business unit and product leaders: Apply the vendor scorecard and go-to-market templates to accelerate launches and reduce integration risk.

- M&A teams: Leverage our competitive mapping and valuation heuristics to prioritize targets with highest integration lift and lowest execution risk.

- Procurement: Implement the supply-risk heatmaps and dual-sourcing templates immediately to de-risk next-generation product builds.

Next steps — where to get the full intelligence

PW Consulting’s Magnetron Market report is deliberately structured as a decision-support tool: we expose methodology, scenarios and strategic guidance here while preserving the commercial-grade, line-level segmentation and vendor-share tables in the full report package. For teams that require the underlying dataset, supplier-level forecasts, and downloadable financial models (2026–2032), please access the full report on our website. The complete deliverable includes actionable templates, ready-to-use procurement scorecards, and an M&A integration checklist that executives can deploy within 30–90 days.

In an industry balancing mature appliance demand with high-growth industrial and regulated end-markets, the choices made in 2026—about capacity, partnerships, and product architecture—will define competitive position for the decade ahead. PW Consulting’s Magnetron Market report gives leaders the foresight and tools to make those choices with confidence.

For detailed analysis of this topic, please visit the official page:Magnetron Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com