GaN Power Devices Market Expands with Rising Demand for High-Performance Power Electronics

Fitness |

2026-06-15 07:32:03

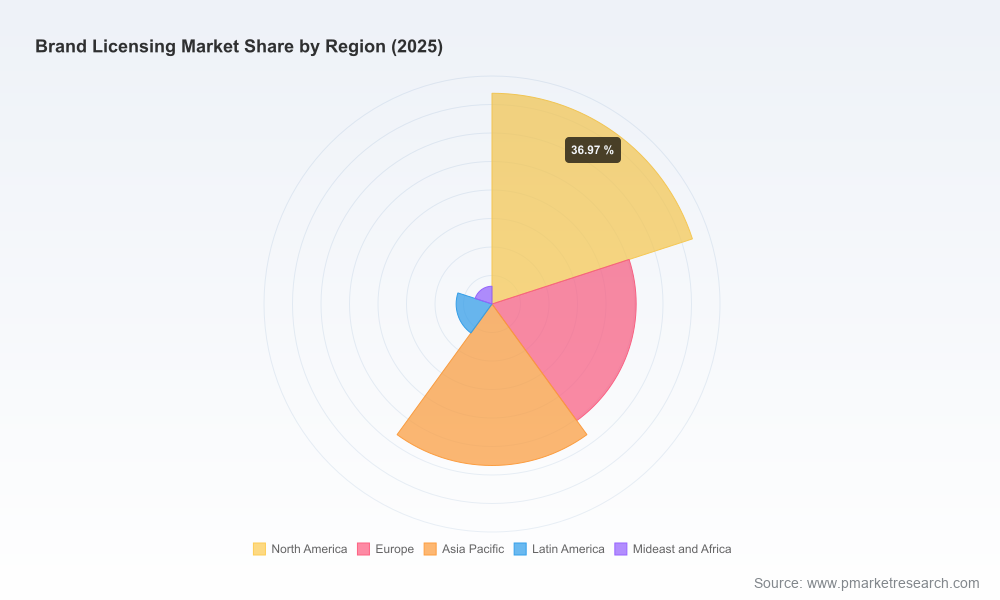

As organizations finalize 2026 roadmaps, the brand licensing landscape will be a decisive axis for growth, risk management, and capital allocation. Our new Brand Licensing Market report — built on a 2020–2025 historical foundation and a 2026–2032 forecast horizon — shows the global market reached USD 288.0 Billion in the base year (2025) and is projected to grow at a 5.2% CAGR through 2032, approaching the mid-400s billion-dollar range by the end of the forecast window. This brief highlights the most consequential takeaways for executives preparing strategic moves in 2026, while intentionally preserving the full, granular breakdowns for subscribers of the complete report.

Brand Licensing Market

Scale and Momentum: The market’s sustained growth trajectory creates a favorable backdrop for both incumbent licensors and newcomer content owners to monetize IP across physical and digital channels. Executives should treat licensing as a primary commercial lever, not an ancillary revenue line.

Brand Licensing Market

Consolidation and Concentration: Market concentration is meaningful — the largest players retain a dominant share of licensed revenues, reinforcing the benefits of scale in distribution, partner access, and IP ecosystem development. This dynamic shapes competitive strategy, partner selection, and M&A rationale.

Brand Licensing Market

Cross‑sector Opportunity: Licensing remains a powerful mechanism to extend entertainment and brand IP into fashion, consumer goods, gaming, and experiences. The most successful deals in 2025–2026 will be those that combine IP equity with rigorous commercial enablement (supply chain, retail placement, digital commerce mechanics).

Regulatory & Cost Pressures: Tariffs, trade barriers, and evolving emissions reporting are non‑trivial inputs into deal economics. Licensing teams must incorporate trade and sustainability variables into royalty models and contract structures.

Transparent Methodology: Replicable market-sizing framework, primary-source royalty triangulation, and validated partner revenue mapping so finance and strategy teams can reproduce and stress-test the headline forecasts.

Scenario Modeling Suite: Three alternative market paths (base, upside, downside) calibrated to consumer spending elasticity, content release cycles, and supply chain shock assumptions — designed for rapid incorporation into corporate planning and investor materials.

Deal Archetypes & Playbooks: Modular templates for common licensing structures (exclusive vs. non‑exclusive, territory-limited, co‑branding, revenue share vs. fixed minimum guarantees), with contract negotiation checklists and KPI scorecards.

Royalty Benchmarking Toolbox: Contextualized royalty ranges tied to product categories and commercialization complexity, plus guidance on escalators, clawbacks, and performance thresholds to protect brand value.

Go‑to‑Market Blueprints: GTM plans for license activation across retail, D2C, experiential, and digital channels, including launch timing playbooks aligned to entertainment windows and holiday cycles.

Supply Chain & Trade Risk Playbook: Tactical guidance on tariff mitigation, nearshoring options, and packaging reengineering to protect margins under evolving trade regimes.

Sustainability & Reporting Integration: Practical approaches to link licensed-goods lifecycle measurement and emissions allocation to royalty streams and partner reporting — a topic of growing investor and regulatory focus.

Competitive Intelligence Dossiers: Strategic profiles, capability maps, and recent development timelines for the industry’s core licensors, enabling rapid benchmarking and counter‑strategy design.

Major licensors are diversifying the ways IP is monetized. Legacy toy companies and entertainment studios are increasingly operating as IP platforms rather than single-channel manufacturers, licensing brands across apparel, collectibles, games, and experiences.

Hasbro exemplifies a diversified licensor model: broad IP portfolios, multi‑category out‑licenses, and an emphasis on strategic extensions. Their 2025 reporting underscores continued licensing growth and operational improvement initiatives that are relevant to peers designing scale‑efficient licensing engines.

The LEGO Group demonstrates an integrated validation approach — using partner royalty data to validate licensed goods volumes and tying emissions allocation to royalty revenue. This methodology is shaping market expectations for transparency and sustainability alignment in licensing agreements.

Mattel’s 2025 strategic reset toward brand‑centric IP partnerships shows how traditional product companies can reframe value creation around narrative, digital extension, and selective third‑party collaborations. Their public disclosures also emphasize macroeconomic sensitivity as a real constraint on discretionary spend.

Content owners like The Pokémon Company, Warner Bros. Discovery, Sony Pictures, and streaming-first creators are sharpening licensing playbooks to convert episodic and franchise engagement into durable consumer product streams. Each brings different strengths — retail reach, creative IP, marketing muscle, or platform distribution — that licensees should map when prioritizing partners.

For finance and corporate development teams, the competitive takeaway is twofold: secure access to high‑engagement IP, and structurally reduce execution risk through partner governance and operational KPIs.

Prioritize portfolio economics over breadth. Conduct a rapid portfolio triage that separates high‑leverage IP (where small investments unlock outsized royalties) from low-return extensions that consume scarce marketing and management bandwidth.

Embed supply‑chain flexibility into contracts. Negotiate clauses that allow agile sourcing shifts, tariff adjustments, and cost pass‑throughs to preserve margin under trade disruption scenarios.

Adopt sustainability‑linked commercial terms. Linking sustainability metrics to royalty adjustments or joint investment in impact measurement reduces counterparty friction and preempts regulatory scrutiny.

Invest in measurement and data flows. Replicate royalty validation practices (where feasible) and invest in data integrations with partners to enable faster, more accurate market monitoring and dispute avoidance.

Design hybrid licensing structures for digital-first IP: balances of guaranteed minimums, revenue shares on platform sales, and performance incentives tied to in‑game or subscription KPIs.

Use targeted M&A or JV activity to plug capability gaps (digital commerce, merchandising, or distribution) rather than broad horizontal consolidation unless the deal delivers clear, quantifiable synergies.

Consumer spending volatility. Mitigation: tiered rollouts, inventory-light models (print-on-demand, licensed drops), and stricter SKU rationalization to protect working capital and margins.

Tariffs and trade friction. Mitigation: dual-sourcing strategies, tariff pass‑through clauses, and localized production for high-margin SKUs.

Brand dilution through over‑extension. Mitigation: enforceable brand guidelines in contracts, staged rollouts with performance gates, and stricter approval rights on product quality.

Regulatory and reporting complexity (including emissions attribution). Mitigation: incorporate sustainability data requirements into licensing agreements and invest in partner audits or validated reporting systems.

Use the report’s scenario models to stress‑test 2026 revenue plans against upside and downside industry paths.

Deploy the deal archetypes and contract templates to accelerate negotiation cycles and reduce legal back‑and‑forth.

Apply the royalty benchmarking toolbox to align board‑level expectations and to structure incentive mechanisms for retail and digital partners.

Leverage the competitive dossiers when evaluating partnership targets or defensively positioning core IP in response to rival strategies.

Note: the report intentionally summarizes headline market sizing and concentration metrics here to orient readers. The full report contains the detailed segmentation, regional and application breakouts, and proprietary dashboards that clients use for transaction diligence and annual planning — access to that intelligence is available on the report landing page.

Conclusion — positioning for 2026: Licensing is no longer a back‑office monetization channel; it is a central strategic lever that links IP strategy, revenue diversification, and operational resilience. With a clear playbook — portfolio focus, contract engineering, supply‑chain agility, and data-enabled partner governance — organizations can capture a disproportionate share of the predictable, recurring value the market is creating. PW Consulting’s Brand Licensing Market report is designed to be the working document senior leaders bring to strategy sessions, deal rooms, and board updates as they navigate 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Brand Licensing Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com