Biolubricants Market Size, Share & Growth Outlook

Art |

2026-06-22 09:59:52

PW Consulting today publishes a strategic briefing derived from our comprehensive Transient Voltage Suppressor (TVS) Diodes Market report (base year 2025). This release is intended as a decision-useful preview for senior executives, product and procurement leaders, and investors preparing choices in 2026. It highlights the high-level market trajectory, competitive dynamics, qualification forces reshaping supplier selection, and the pragmatic playbook we recommend — while deliberately reserving the detailed segment tables and proprietary datasets to the full report.

Transient Voltage Suppressor (TVS) Diodes Market

Our macro model places the global TVS diodes market at USD 190 Million (Million USD) in 2025, following a steady recovery and expansion from USD 128 Million in 2020. Under a central scenario, the market is expected to grow at a compound annual growth rate (CAGR) of approximately 8.2% over the 2026–2032 forecast window, reaching roughly USD 330 Million by 2032. Near-term annual progression is visible from the 2026 projection onward, reflecting a mix of rising unit demand and increasing average selling prices tied to higher-voltage, automotive-grade and protection arrays.

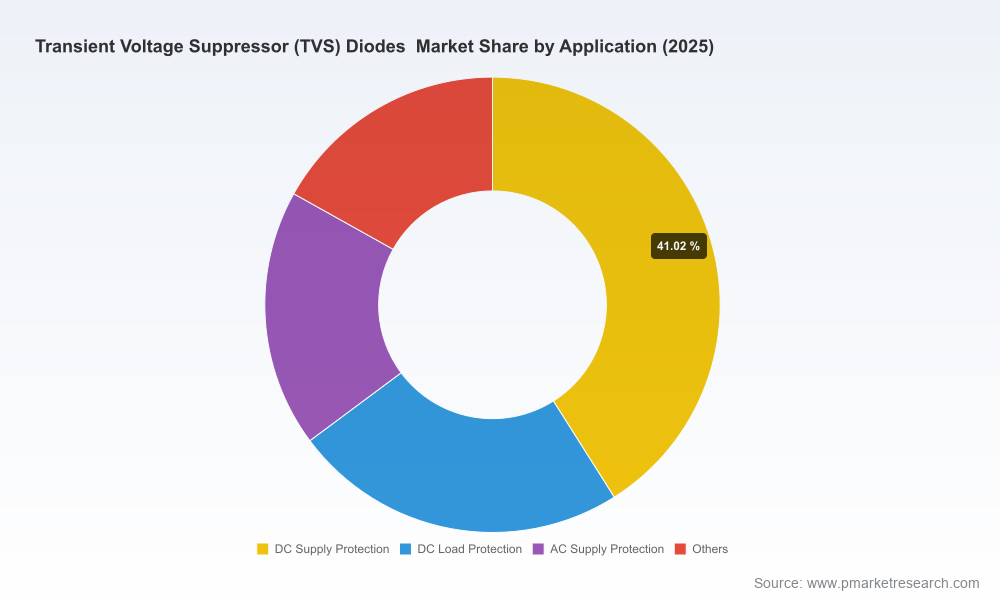

Transient Voltage Suppressor (TVS) Diodes Market

Two implications follow for 2026 decision-making: first, TVS diodes are transitioning from tactical commodity parts to strategic architecture elements in high-value systems (automotive, industrial and energy). Second, suppliers and OEMs that move now on qualification, design-in support, and roadmap alignment will capture outsized share as customers consolidate around fewer trusted sources.

Transient Voltage Suppressor (TVS) Diodes Market

Electrification and high-voltage architectures: The continuing proliferation of electric vehicles, energy-storage systems and high-voltage industrial power electronics is driving demand for TVS solutions that combine high standoff voltage, low clamping characteristics and automotive qualification.

Qualification and reliability are decisive procurement filters: AEC-Q101 and PPAP-capable offerings are increasingly table stakes for automotive programs, while military- and aerospace-grade qualifications (e.g., MIL-PRF) open premium segments. Recent vendor moves underscore this trend: major suppliers have introduced high-voltage, AEC-Q101-compliant series and expanded PPAP-capable portfolios in 2025–2026.

Consolidation of sourcing: Market concentration measures indicate a moderately consolidated market (top-3 suppliers represent a majority share, and the top-5 enlarge that position). That structure favors incumbent leaders but leaves bandwidth for mid-tier specialists to exploit niche applications and regional OEM relationships.

Design complexity and system-level thinking: TVS selection is less about a single diode spec today and more about system-level protection strategies, integrating transient suppression with surge arrestors, filters and board-level layout constraints. Suppliers offering design-support services and customization will consistently win design-ins.

Our full report delivers actionable intelligence tailored to commercial strategy and procurement planning. Highlights include:

Robust market sizing and trend analysis — historical (2020–2025) and scenario-based forecasts (2026–2032) for market value and unit demand.

Technology roadmap and product taxonomy — classification of TVS types, key performance levers (standoff voltage, clamping voltage, power dissipation), and migration pathways for automotive and industrial HV applications.

Supplier benchmarking — comparative profiles of incumbent and challenger firms, go-to-market models, manufacturing footprints, qualification capabilities and channel strategies.

Commercial playbooks — pricing and margin sensitivity, contract structures for long-term supply, and strategies to accelerate design wins (engineering cadences, sample programs, joint validation plans).

Supply chain and risk analysis — capacity mapping, component-level bottlenecks, substitution risks and tactical mitigation measures for procurement teams.

M&A and partnership landscape — screens for acquisition and alliance targets, valuation considerations and integration risk checklists for corporate development teams.

Regulatory and qualification matrix — mapping of AEC, military and industry standards to product families and customer requirements.

The TVS market is characterized by a mixture of large diversified semiconductor houses, dedicated discrete specialists, and emerging regional players. Our strategic review examines a set of industry participants that shape technology, qualification norms and channel dynamics. Key observations include:

Littelfuse, Inc. — a prominent supplier with a focused push into high-voltage automotive TVS families. Recent product introductions and PPAP-capable, AEC-Q101-qualified offerings strengthen their position for EV and high-voltage powertrain protection. Their portfolio strategy emphasizes application-specific series for battery disconnect units and high-voltage HVAC systems.

Bourns, Inc. — historically strong in protection components with sustained investment in automotive-grade TVS lines and qualification processes, making them a reliable partner for OEMs demanding AEC-Q101 compliance.

Major semiconductor groups (e.g., Infineon, Vishay, STMicroelectronics, ON Semiconductor, Texas Instruments, Nexperia) — leverage scale, broad distribution and integrated systems expertise to bundle TVS with power-management offerings, while competing on reliability, cost and qualification pipelines.

Specialists and niche suppliers (e.g., Diodes Incorporated, Semtech, Diotec/MCC, INPAQ, PROTEK) — win on agility, customized form-factors and competitive lead times. Several have strong footholds in specific application verticals or regional OEM networks.

Concentration dynamics — our analysis finds the top three suppliers account for a decisive share of the market (reflecting established OEM relationships and qualification momentum), with the top five increasing that concentration. This environment creates both barriers and opportunities: barriers for late entrants in mainstream automotive programs, opportunities for specialists in emergent niches.

Qualification regimes are now a primary determinant of commercial success. Automotive OEMs and Tier-1s expect AEC-Q101 compliance and PPAP readiness for critical protection components; military and aerospace programs continue to demand MIL-PRF family qualifications for high-reliability arrays. Notable trends include:

Major suppliers publicizing AEC-Q101 and PPAP-capable TVS series to support 800 V+ architectures and battery subsystem protection.

Availability of MIL-PRF-level TVS arrays from selected vendors for mission-critical applications.

Qualification timelines increasingly dictating program cadence — early engagement and shared validation plans materially speed design-in and reduce later-stage change orders.

For executive teams and procurement leaders looking to act in 2026, our advisory priorities are:

For suppliers: prioritize AEC-Q101 and PPAP accreditation for HV product lines, invest in robust application engineering services, and build flexible manufacturing capacity to capture evolving design-wins in EV and energy storage programs.

For OEMs and Tier-1s: adopt supplier scorecards that weight qualification status, design support and supply resilience more heavily than unit price alone. Lock in engineering partnerships earlier in the development cycle to reduce rework and qualification delays.

For investors and corporate development teams: evaluate targets based on qualification pipelines, niche application penetration and the ability to offer system-level protection solutions. Mid-tier specialists with strong OEM relationships and qualified product families are particularly attractive consolidation candidates.

For procurement: diversify qualification-approved suppliers across geographies to mitigate lead-time and concentration risk, while negotiating longer-term conditional commitments that align investment with forecasted uptake.

The TVS diodes market is no longer a low-engagement commodity lane; it is a strategic node in the architecture of electrified, connected and safety-critical systems. Our full market study provides the empirical backing, supplier intelligence, and executable playbooks required to translate that realization into commercial advantage. We provide the detailed segment tables, regional and application-level forecasts, product-level gap analyses, and supplier scorecards that procurement and strategy teams will need to finalize 2026 commitments.

To access the full dataset, granular segmentation, and the step-by-step decision playbooks referenced in this briefing, please visit the official PW Consulting report page. The full report contains the detailed breakdowns and proprietary scenario models necessary for contractual, R&D and M&A planning.

For detailed analysis of this topic, please visit the official page:Transient Voltage Suppressor (TVS) Diodes Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com