Vegan Ingredients Market Tracked to Multiply in Value Driven by Global Clean-Label Trends and Allergen-Free Formulations

Food |

2026-05-21 14:58:20

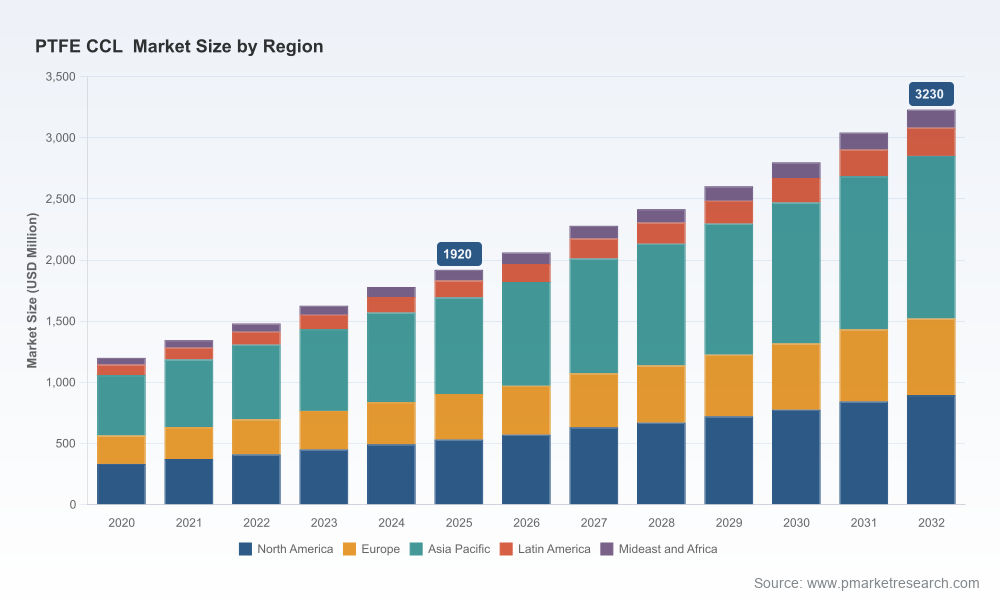

PW Consulting’s new PTFE Copper-Clad Laminate (CCL) Market report—anchored on a 2025 base year and projecting through 2032—delivers a decision-grade synthesis for executives planning capital allocation, product roadmaps, and supply-chain strategies in 2026. The market shows steady expansion driven by demand for low-loss substrates across 5G/mmWave, automotive radar, aerospace, and advanced communications infrastructure. Our model points to a compound annual growth rate (CAGR) of 7.8% for the forecast window, with the total addressable market growing from a base of approximately USD 1.92 billion in 2025 toward a multi-billion-dollar opportunity by 2032. This release summarizes the strategic implications; full granular datasets, scenario outputs, and vendor scorecards are available in the full report.

PTFE CCL Market

2026 is a pivotal year for firms in the PTFE CCL ecosystem. Technology transitions (mmWave, higher-frequency radar), regulatory tightening around advanced materials and dual-use electronics, and supply-side moves (capacity additions and distribution reshuffles) are converging to re-price risk and opportunity. Companies that treat PTFE CCL not as a commodity substrate but as a strategic technology asset—integrating supply, IP, and application-driven differentiation—will capture disproportionate value as the market scales at near-8% CAGR.

PTFE CCL Market

Demand drivers: Persistent build-out of high-frequency communications (including higher-band 5G deployments and next-wave backhaul), accelerating automotive ADAS radar adoption, and sustained aerospace/defense procurement for low-loss, high-reliability substrates.

PTFE CCL Market

Supply-side momentum: Targeted capacity expansions and strategic partnerships are already changing availability for specialist PTFE-based laminates, while new product variants (ceramic-filled PTFE, fiberglass-free low-Df laminates) are enabling performance differentiation.

Consolidation and concentration: The PTFE CCL market exhibits moderate concentration at the top. Market leaders control significant share, but there is room for mid-tier challengers that combine niche product performance with regional supply agility.

Regulatory and raw-material pressures: Export control regimes and mineral export policies have heightened supply-chain complexity. These dynamics affect not only downstream design choices but also sourcing, inventory policy, and partner selection.

For 2026 planning, the report highlights four strategic imperatives. Each is supported by scenario-tested recommendations and operational playbooks:

Embed substrate strategy into product R&D: Firms must align PTFE CCL selection to system-level electrical and thermal targets early in the design cycle. Trade-offs between dielectric constant, dissipation factor, and manufacturability are application-specific; a formalized substrate decision framework reduces costly late-stage rework.

De-risk the supply base via layered partnerships: Expect selective capacity expansions and distributor realignments to continue. A layered supply strategy—primary supplier agreements, regional second-sources, and distributor-level safety stock—mitigates both regulatory-triggered export limitations and supplier-specific outages.

Differentiate through materials and process know-how: Proprietary laminate stacks (e.g., ceramic-filling for thermal control, fiberglass-free weaves for low loss at mmWave) will be defensible product differentiators. Investing in co-development and IP-backed specifications increases switching costs for OEM customers.

Operationalize regulatory intelligence: Export controls and mineral policy shifts materially affect where and how advanced PTFE laminates can be produced and shipped. Integrating regulatory scenario planning into supply-chain and M&A diligence is now table stakes.

Our competitive analysis places emphasis on product roadmaps, regional capacity positioning, and go-to-market strategies rather than raw price competition. Key firms we evaluate in depth include:

Rogers Corporation (Chandler, AZ): Well-known for RO3000® ceramic-filled PTFE composites and RT/duroid® high-frequency laminates, Rogers continues to invest in capacity for high-frequency markets, with recent European expansion reinforcing supply options for global customers.

AGC Inc. (Tokyo): AGC’s Fluon® PTFE derivatives and CCL offerings through legacy brands combine materials science with an extensively distributed sales footprint; selective distributor agreements have broadened access in target geographies.

Chukoh Chemical Industries (Osaka): Specializes in precision-controlled PTFE laminates with low dielectric constants—positioning that appeals to communications and defense applications where tight tolerances matter.

Shengyi Technology (Dongguan): Strong in glass-fabric reinforced PTFE RF materials and commercially oriented mmWave products. Strategic partnerships with electronics houses underline a playbook focused on integrated product development.

Doosan Corporation Electro-Materials (Seoul): Bringing targeted solutions for automotive radar (notably 77 GHz motherboards), Doosan’s technical specialization aligns with fast-growing automotive segments.

Taiflex Scientific (Kaohsiung) and Nanya Plastics (Taipei): Both bring portfolio depth to mmWave and 5G base station substrates, with product lines emphasizing low-loss and manufacturing consistency for high-volume programs.

We benchmark each supplier across technology performance, capacity flexibility, regulatory exposure, and commercial agility. The full vendor matrix in the report includes supplier scorecards, sample RFI templates, and negotiation playbooks tailored to large OEMs and contract manufacturers.

Partnerships and distribution expansions have reshaped access: Expanded distributor agreements and strategic alliances are shortening lead-times for certain customer segments, while also introducing new geographic dependencies.

Capacity additions: Targeted plant expansions for high-frequency laminates are moderating near-term supply tightness but are uneven across regions and product types—timing and qualification windows matter for customers with ramping programs.

Regulatory tightening and mineral controls: Recent updates to export control regimes and national mineral export policies add a new layer of complexity to procurement and compliance. These are not static risks; they bear directly on supplier selection and inventory posture.

The full PTFE CCL Market report is practical and execution-focused. Highlights include:

Top-line market model with historicals and scenario-based forecasts through 2032, highlighting sensitivity to macro and regulatory shocks.

Supplier scorecards and contract negotiation playbooks (including RFP/RFI templates and qualification checklists).

Technology deep dives (ceramic-filled PTFE, fiberglass-free substrates, and process controls) and their implications for manufacturability and reliability.

Detailed supply-chain risk register with mitigation levers (dual-sourcing templates, inventory hedging strategies, nearshoring criteria).

M&A and partnership library: valuation heuristics for bolt-on acquisitions, JV term-sheet outlines, and integration checklists focused on PTFE laminate capabilities.

Regulatory scenario playbooks that translate export-control permutations and mineral policy shifts into procurement and production actions.

Conduct substrate-first design reviews for any new RF/mmWave and automotive radar programs to lock in manufacturable material choices before tooling commitments.

Establish at least two qualified suppliers per critical laminate family and codify escalation protocols to switch volumes within defined technical acceptance windows.

Pursue selective co-development agreements with producers that offer unique process controls (e.g., thickness precision, low Df glass alternatives), securing technical exclusivity or first-right allocations for key programs.

Integrate regulatory-monitoring into procurement KPIs, with quarterly trigger reviews tied to inventory replenishment policies and contract clauses for force-majeure and export limitations.

Evaluate strategic investments (capacity minority stakes, toll-manufacturing agreements) in markets where lead-time and qualifying barriers materially affect time-to-market.

PW Consulting’s PTFE CCL Market report is designed as an executable toolkit for the 2026 decision cycle: it couples a macro growth trajectory (7.8% CAGR through our forecast window) with supplier intelligence, regulatory scenarios, and operational playbooks that turn insight into action. The report provides the evidence base and templates buyers, OEMs, and materials companies need to move from strategic intent to measurable outcomes.

For executives who need rapid, risk-calibrated plans, PW Consulting offers custom workshops that overlay your product roadmap and supplier contracts on our market model. To review the full dataset, vendor matrices, and scenario outputs that underpin these findings, access the full report and supplemental tools through our publication page.

For detailed analysis of this topic, please visit the official page:PTFE CCL Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com