Solder Market 2026: Strategic Imperatives from PW Consulting’s New Market Report

As electronic complexity, regulatory pressure, and raw-material volatility converge, the solder market has become a strategic fulcrum for hardware manufacturers, EMS providers, component suppliers, and investors. PW Consulting’s latest Solder Market report (base year 2025) delivers the high-fidelity insights that 2026 decision-makers need: a consolidated market view, forward-looking scenarios, and pragmatic playbooks that translate industry dynamics into executable choices.

Solder Market

Macro snapshot: What the numbers tell strategic planners

Our market model places the global solder market at USD 5.09 Billion in 2025 (base year), with a multi-year compound annual growth rate of 4.2% across the forecast horizon. Under base assumptions, the market scales toward the late-stage forecast, reflecting steady demand from electronics assembly, semiconductor packaging, and automotive electrification. The sector is neither hyper-consolidated nor atomistic: the top three players account for roughly 45% of market share while the top five rise to approximately 55%, indicating a competitive landscape where scale matters but differentiation through technology and service remains decisive.

Solder Market

Why this report matters for 2026 strategy

- Decision-grade forecasting: Our blended model combines historical sales (2020–2025), proprietary demand signals, and Monte Carlo scenario runs for 2026–2032, enabling procurement, R&D, and corporate development teams to stress-test plans against plausible market inflection points.

- Supply-chain fragility mapped to action: We translate raw-material exposure—most notably tin-centric demand drivers—into procurement hedges, contract clauses, and supplier diversification tactics that reduce margin and delivery risk without compromising quality requirements.

- Regulatory-first commercialization: With global regulatory frameworks accelerating lead elimination in many markets, our playbooks show how firms can accelerate lead-free adoption, justify price-premium strategies, and forecast margin impacts given the higher input cost base of alternative alloys.

- Investment and M&A prioritization: Because the market has moderate concentration, targeted acquisitions and strategic alliances can move the needle on capability and geography. The report ranks inorganic opportunities and overlays financial, technical, and integration risk filters to prioritize targets.

What’s inside the report (practical content highlights)

- Executive market model (2020–2032) with scenario layers and sensitivity matrices for raw-material price shocks, regulatory acceleration, and demand substitution.

- Segment playbooks that translate type, application, and regional dynamics into go-to-market tactics for vendors, CMs, and OEMs—designed to be actionable without requiring deep metallurgy expertise.

- Supply-chain topology and single-point-of-failure heatmaps that identify bottlenecks across alloy, flux, and preform supply—plus mitigation templates for procurement teams.

- Competitive benchmark and capability matrix for leading suppliers, including product strength, process certifications, and route-to-market footprints.

- Regulatory tracker and compliance roadmap tailored to lead-free adoption schedules across major purchasing jurisdictions.

- Commercial tools: pricing impact calculators, TCO (total cost of ownership) worksheets for lead vs. lead-free choices, and R&D prioritization scorecards.

- M&A playbook: valuation priors, integration risk checklists, and three case-study integrations that highlight common pitfalls and accelerators.

Competitive landscape: What leading firms are doing now

The report includes a nuanced, consultative analysis of the core vendor universe. A few themes stand out from our company-level workstream:

Solder Market

- Technology leadership as a market moat: Firms that combine alloy development with process know-how and strong reliability data (e.g., long-term thermal cycling, drop/flex survivability) secure premium positions in high-reliability segments such as semiconductor packaging and aerospace electronics.

- Channel and service differentiation: Suppliers that layer technical support, certification programs, and localized stocking demonstrate stickiness with EMS and OEM customers even where basic alloys are commoditized.

- M&A and asset plays: Strategic acquisitions and asset purchases are active levers for portfolio completion and scale in targeted geographies. Recent deals and asset transfers highlight the dual priority of expanding product breadth while shoring up supply continuity.

Representative company vignettes (covered with depth in the report):

- Indium Corporation — A U.S.-based leader in high-reliability pastes and alloys, investing in NPI-certified products and trade-show engagement to secure design wins in advanced electronics. Recent product recognition and trade-show participation underline a market-facing push on both technology and brand.

- Senju Metal Industry — A Japan-headquartered specialist in lead-free alloys, now being recognized by tier-one OEMs for supplier performance; supplier awards underscore strong qualification momentum in high-demand programs.

- Kester — A global supplier blending assembly materials with distribution relationships that are critical to rapid ramp programs in electronics manufacturing.

- Heraeus Electronics, Balver Zinn, Stannol, Duksan Hi-Metal — European and Asian players that offer differentiated capabilities across paste, wire, preform, and solder-ball technologies; these firms compete on materials science depth and local-market responsiveness.

- Smaller scale consolidators and asset buyers — There is an active secondary market where assets and niche capabilities are traded to accelerate technological coverage or to secure capacity.

Dynamics shaping the next 12–24 months

- Raw-material forces: Tin-based solders remain the primary driver of tin demand across metals markets. Elevated costs for lead-free formulations—meaningfully higher than traditional solders—are reshaping procurement and pricing strategies. Our report models both direct material-cost pass-throughs and indirect impacts on yield/rework costs.

- Regulation and compliance: Regulatory frameworks worldwide are tightening hazardous substances rules, accelerating adoption of lead-free alternatives in many product classes. Beyond compliance, regulatory timelines create windows for premium product introductions and service agreements that help suppliers maintain margins.

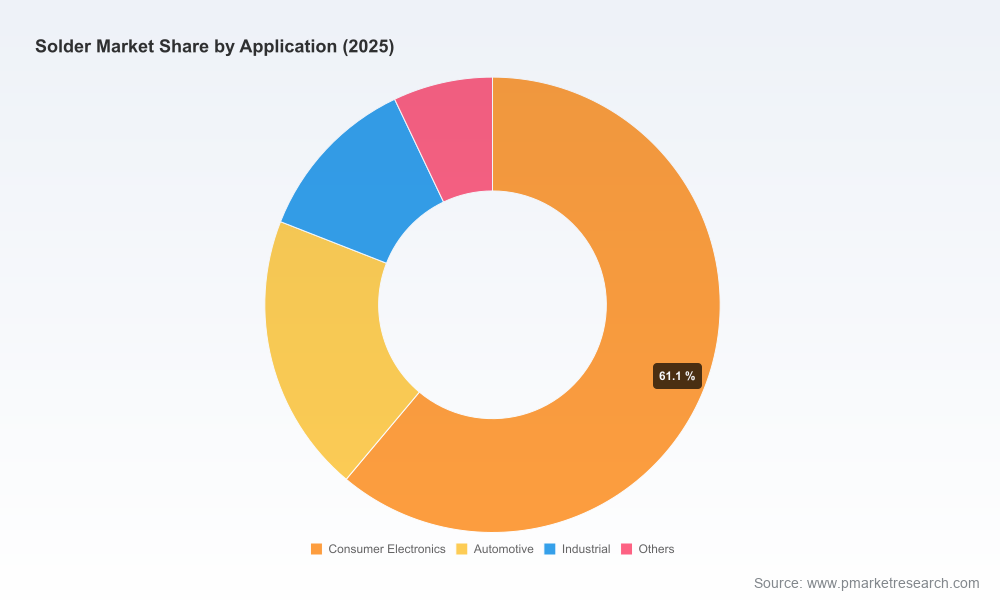

- End-market substitution and technology shifts: Automotive electrification, miniaturization in consumer devices, and heterogeneous semiconductor packaging are changing solder specification requirements—driving demand for specialized pastes, low-void alloys, and solder-ball technologies.

- Cost and margin pressure: With lead-free alternatives carrying a notable price premium, OEMs and EMS providers must balance performance gains against materially different cost structures; our TCO frameworks enable transparent, board-level decision analysis.

How to translate this intelligence into 2026 actions

PW Consulting recommends a three-track operational response for firms looking to convert insight into advantage during 2026:

- Procurement & Operations (Short-term, 3–9 months): Implement hedging strategies for key metal inputs, negotiate flexible take-or-pay clauses with tier-one suppliers, and introduce dual-sourcing pilot programs for the most critical alloy families. Use our supplier heatmaps to prioritize contingency suppliers.

- Product & Quality (Medium-term, 6–15 months): Invest in test-programs to qualify lead-free and low-void formulations across representative assemblies. Prioritize alloys that lower rework risk in high-mix/low-volume lines and secure long-term supply agreements for validated materials.

- Corporate Strategy & M&A (12–24 months): Evaluate bolt-on acquisitions for capacity or specialty alloys that fill capability gaps. Use our M&A playbook to size targets and stress-test integration scenarios against regulatory acceleration and raw-material volatility.

Methodology and confidence

The report’s forecasts rest on three pillars: historical demand analytics (2020–2025), supplier shipment and qualification signals, and scenario-based macro modeling through 2032. We use probabilistic scenario ranges to capture upside from accelerated electric vehicle content and downside from potential macro slowdowns. Confidence bands are explicitly modeled; the report includes sensitivity tables and recommended monitoring triggers to keep strategy aligned with market reality.

Why PW Consulting’s perspective is actionable

Our work transcends a static market-size narrative. We pair quantitative modeling with field-tested playbooks: sample supplier contracts, procurement scorecards, lab qualification roadmaps, and commercial negotiation checklists. The report is designed for cross-functional teams—procurement leads, VP-level operations, R&D heads, and corporate development—to convert insight into measurable outcomes in 2026.

Next steps and accessing the full intelligence

This article is a strategic preview: it outlines the market arc, competitive dynamics, and recommended actions that should inform board-level and operational planning in 2026. To access the full dataset, segment-level analytics, and the tactical toolkits referenced here, visit our report page and download the complete Solder Market report. The full document contains the granular segmentation, supplier scorecards, and downloadable modeling templates that clients use to build executable plans.

For bespoke briefings, scenario workshops, or support integrating the report’s outputs into your planning cycles, PW Consulting’s sector team is available to conduct customized deep-dives that align the findings to your organization’s strategic priorities.

For detailed analysis of this topic, please visit the official page:Solder Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com