Barrier Systems Market Trends, Insights and Future Outlook

Other |

2026-04-13 06:57:49

PW Consulting’s latest Formwork Market study (base year 2025; historical coverage 2020–2025; forecasting window 2026–2032) distills the operational intelligence that construction executives, private equity investors, and equipment suppliers need to set winning strategies for 2026. Our consolidated market model indicates a steady expansion trajectory from the 2025 baseline through 2032 at a compound annual growth rate (CAGR) of 5.95%. By 2032 the market is expected to approach the upper end of the industry’s multi‑year cycle, underscoring a window of opportunity for focused investment and operational optimization.

Formwork Market

Capital allocation and timing: The forecast cadence and scenario overlays in this study convert macro demand trends into near‑term capital schedules for plant upgrades, rental fleet expansion, and inventory management. Finance teams can use the report’s cash‑flow and capex simulations to time purchases and leasing decisions that maximize return on invested capital under different demand scenarios.

Formwork Market

Procurement and input‑cost playbooks: With raw material volatility an active force in 2026, procurement leaders will benefit from the report’s forward price‑deck scenarios and supplier risk matrices to negotiate long‑term purchase agreements and indexed contracts.

Formwork Market

Product and R&D prioritization: The analysis highlights where modular, aluminum, and digitally enabled formwork systems deliver the greatest operational uplift. R&D roadmaps and product roadmaps built from the report’s ROI cases enable manufacturers to accelerate development where adoption curves are steepest.

M&A and partnership screening: A concentrated supplier landscape and clearly articulated capability maps allow corporate development teams to prioritize tuck‑ins, geographic entries, or technology purchases that close capability gaps fast.

Our baseline estimates show the industry expanding from the 2025 reference point and growing at an approximate 5.95% CAGR through 2032 in the base scenario. This is a structural growth profile rather than a volatile rebound—driven by steady construction activity, sustained urban housing programmes in multiple macro regions, and ongoing infrastructure investment. For incumbents that convert long‑lead demand signals into capacity and asset management plans, the forecast provides a reliable foundation for multi‑year resource allocation.

Market concentration is meaningful: the three largest players account for a significant portion of market revenues, and the top five together command a large majority share. That concentration reinforces the strategic logic of scale—both in manufacturing and global rental networks—while leaving niches open for specialist innovators and regional challengers.

Regulatory tightening and safety enforcement: New and updated OSHA guidance continues to raise the bar for formwork design and on‑site practices. The continued emphasis on fall protection, scaffolding inspections, and expanded recordkeeping (including the 2026 Heat Illness Prevention Standard and updated citations for formwork‑related hazards) increases compliance costs and favours suppliers that bundle safety‑certified systems and training services.

Raw material inflation and supply constraints: Input markets are noisy. For instance, polypropylene price movements in mid‑2026 reflected continued sensitivity to global supply patterns, while steel mill product prices rose materially—industry sources indicate increases in the mid‑teens to mid‑thirties percent range in 2026 due to tariffs and constrained supply. These dynamics pressure margins for commodity‑heavy product lines and accelerate the case for higher‑value, repeatable aluminum and modular offerings.

Digital adoption and productivity: Digital planning tools and data‑driven layout systems are moving from ‘nice‑to‑have’ to essential. Vendors that pair hardware with planning software—reducing cycle times, lowering labor risk, and improving concrete throughput—are winning specification on large projects and in markets where labor scarcity is acute.

Rental and asset‑light models: Contractors under margin pressure increasingly prefer rental or managed‑service formwork models. Rental economics reduce upfront capex needs, improve cash flow, and create recurring revenue streams for equipment owners—an important strategic pivot for manufacturers and distributors.

The market features a blend of global platform players and regional specialists. The concentration metrics noted earlier mean that scale, integrated services (engineering, training, planning), and product breadth are differentiators. Below we summarize the strategic positioning of core providers covered in our study; full vendor scorecards and capability matrices are available in the complete report.

PERI Group (Weißenhorn, Germany): A leader in modular grid beam systems and climbing forms, PERI’s recent product introductions aim to shorten site cycle times and improve safety margins, making them a key reference for high‑rise and infrastructure projects.

Doka GmbH (Amstetten, Austria): Strong in wall and slab systems with increasing investment in digital planning tools; their integrated offering is capturing projects where planning accuracy and productivity uplift are prioritized.

ULMA Construction (Oñati, Spain): With a renewed focus on aluminium systems for mass housing, ULMA is positioning to capture scale demand in emerging markets that prioritize speed and repeatability.

MEVA Formwork Systems (Haiterbach, Germany): Known for lightweight aluminium and reusable systems paired with customer‑facing content; their communication and service programs support adoption by builders seeking lower lifecycle costs.

Other notable names (regional and specialty players): RMD Kwikform, PASCHAL, NOE‑Schaltechnik, Faresin, Altrad Group, EFCO, BrandSafway, Alsina, Intek, Condor, Waco International, MFE, Zulin, Pilosio—each brings differentiated strengths in segments such as precast, heavy shoring, and industrial projects.

Recent vendor activity in 2025–mid‑2026 underscores these strategic moves: PERI’s SKYFLEX and LEVO launches, Doka’s new products and digital tool suite launches and exhibition programmes, ULMA’s aluminum product expansion targeting mass housing, and MEVA’s customer‑engagement content releases all signal intensified competition around productivity and modularisation.

For manufacturers: Prioritise modular aluminum platforms and integrated digital services. Transition commodity lines toward higher‑value reusables and offer rental/managed solutions to stabilise revenue cycles.

For contractors and rental firms: Reassess asset mix using utilization analytics—prioritise equipment that drives cycle‑time reductions and reduces labor intensity. Negotiate index‑linked supply contracts to share raw‑material risk with vendors.

For investors and M&A teams: Screen targets for proprietary system integration (hardware + planning software), strong rental economics, and demonstrated capacity to scale regionally. Use vendor scorecards to fast‑track diligence.

For procurement: Implement layered hedging on steel and polymer inputs and accelerate local supplier qualification to reduce tariff exposure and lead‑time risk.

For policy and safety officers: Build compliance into product offerings—documented safety credentials and site‑training packages are increasingly part of spec requirements and can be monetised.

This report is designed for executables, not just executives. Highlights include:

A detailed historical baseline (2020–2025) and transparent forecasting methodology for 2026–2032, including sensitivity runs and upside/downside scenarios tied to demand and input‑cost shocks.

Vendor scorecards and competitive maps that evaluate product breadth, service capability, geographic reach, and digital maturity.

Operations playbooks: procurement templates, rental fleet optimisation models, maintenance schedules, and labour‑productivity calculators for benchmarking on‑site performance.

Regulatory and safety matrix that translates new OSHA guidance and enforcement trends into required product and site changes, with implementation checklists.

Raw‑material decks and price scenarios, with suggested contracting clauses and hedging strategies to protect margins under the 2026 cost environment.

M&A and partnership pipeline: curated targets, valuation checklists, and integration roadmaps tailored to buyers seeking inorganic growth in formwork.

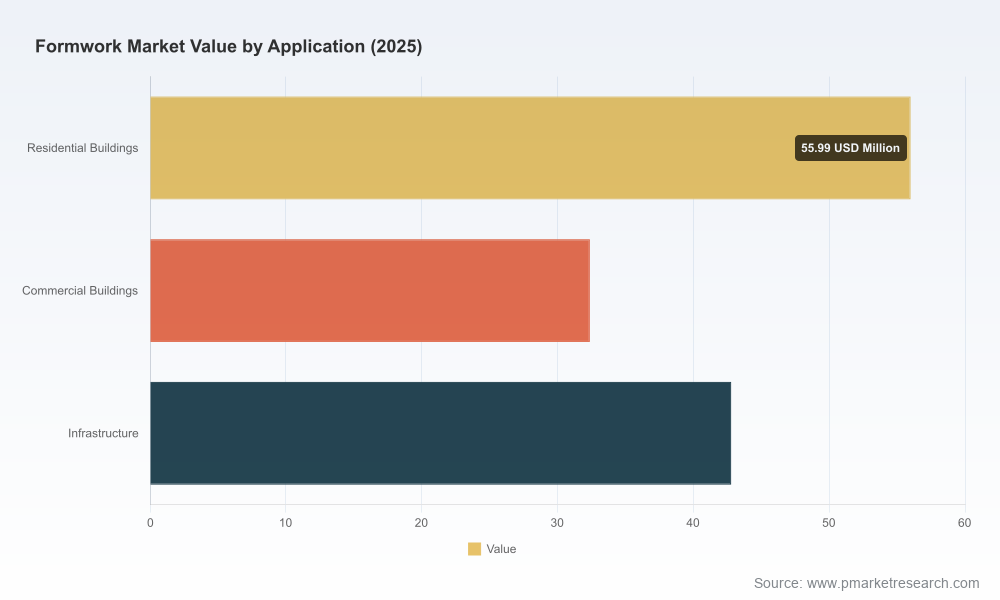

Note: In keeping with our “trailer” approach we have intentionally constrained granular regional, type and application splits from this release. The full dataset includes exhaustive regional and application‑level forecasts, unit economics by formwork type, and downloadable financial models available through the PW Consulting portal.

Use this brief as a rapid diagnostic to align 2026 planning cycles: incorporate the cost and regulatory signals, prioritise investments that remove labor and cycle‑time risk, and treat the rental economy as a strategic channel. For operators and financiers, the decisive actions for 2026 are practical—lock sensible price protection for steel and polymer inputs, accelerate digital planning adoption, and pursue scale in rental and managed offerings where possible.

For a full copy of PW Consulting’s Formwork Market report, including the region/type/application level tables, vendor scorecards, and downloadable scenario models, please visit the PW Consulting report page or contact our industry desk for an executive briefing and data licence.

For detailed analysis of this topic, please visit the official page:Formwork Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com