North America Radar Security Market Research: Advanced Radar Innovation Strengthens Regional Growth

Technology |

2026-06-25 11:51:35

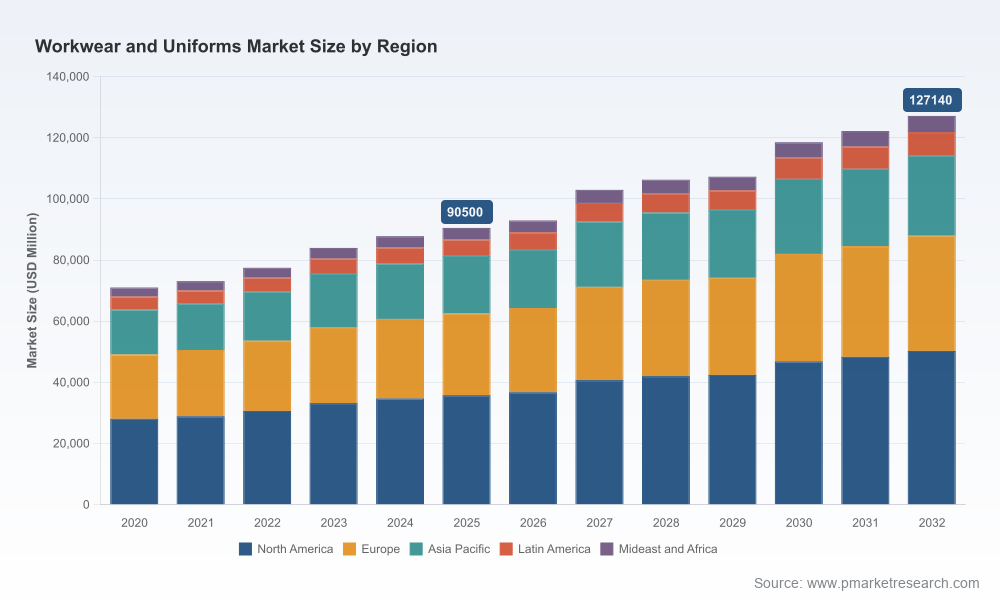

PW Consulting’s latest Workwear and Uniforms Market research (base year 2025) surfaces the strategic imperatives procurement, operations, and investor teams must confront as they set budgets and partnerships for 2026. Our long‑range modelling—anchored in rigorous historical series (2020–2025) and forward projections through 2032—shows a stable expansion trajectory with a compound annual growth rate (CAGR) of 5.0% over the forecast window. The global market is estimated at USD 90,500 Million in 2025 and is projected to approach USD 127,140 Million by 2032, underscoring meaningful scale and continued commercial opportunity across manufacturing, rental/laundering services, PPE, and specialty apparel lines.

Workwear and Uniforms Market

Budgeting and CAPEX: The market’s steady 5.0% CAGR signals predictability but masks near‑term volatility in input costs. Organizations must balance longer‑term contract commitments against short‑term supply shocks and inflationary pressures.

Workwear and Uniforms Market

Sourcing strategy: Recent policy actions and tariff shifts have materially increased the cost risk of imported professional clothing. Procurement leaders need scenario tools to evaluate onshore manufacturing, nearshoring, or strategic inventory buffers.

Workwear and Uniforms Market

Vendor selection: Market concentration remains meaningful—top three players account for roughly 49% of industry revenue and the top five about 61%—which alters negotiation power, service availability, and the calculus for in‑house versus outsourced solutions.

Workforce and compliance: Regulatory changes affecting uniform allowances and minimum wage frameworks are already impacting operating cost for employers and service providers alike; compliance‑aware contracts will be a 2026 priority.

Our analysis identifies three converging dynamics that will define winning strategies next year:

Cost‑push shocks from trade policy: A new U.S. tariff framework adopted in 2025 is expected to raise short‑term costs for imported professional clothing substantially. Buyers must assess contract clauses and price‑escalation mechanisms now to avoid sudden margin compression.

Service model bifurcation: The market continues to bifurcate between asset‑light rental and laundering ecosystems (service platforms that emphasize uptime, hygiene, and compliance) and branded, durable manufacturers that compete on durability, brand equity, and specialty PPE features. Each model attracts different buyer segments and margin profiles.

Regulatory and labor pressure: Policy moves such as uniform allowance ceilings and wage increases for service workers are directly influencing pricing and service design. Employers will need to reexamine allowance policies, tax treatment, and vendor SLAs to preserve worker welfare while controlling costs.

The industry is anchored by a mix of large service integrators, pure‑play manufacturers, and regional specialists. Key incumbent profiles we cover in the report include:

Cintas Corporation (Mason, Ohio): A dominant service integrator specializing in uniform rental, laundering, and logistics programs. Its scale and recurring revenue model make it a bellwether for service pricing and contract norms.

UniFirst Corporation (Wilmington, Massachusetts): A competitor focused on rental and facility services with a strong presence in safety clothing and PPE—an important supplier for regulated industries.

Carhartt, Inc. (Dearborn, Michigan) and Williamson‑Dickie (Fort Worth, Texas): Large manufacturers with deep brand recognition in heavy‑duty workwear and industrial apparel. Their manufacturing footprint and product durability set the standard in segments where longevity and protection matter most.

Engelbert Strauss (Germany), Alsico Group (Belgium), and Fristads Group (Sweden): European players that combine high‑performance product engineering with growing sustainability claims—relevant to buyers seeking certified PPE and low‑life‑cycle‑impact solutions.

Across these archetypes we identify strategic fault lines—rental versus ownership, global scale versus local specialization, and platform‑enabled supply chains versus vertically integrated manufacturing—that will shape partnership choices in 2026. Our report benchmarks these players across capability matrices (service reliability, compliance coverage, cost pass‑through mechanisms, innovation in materials, and ESG credentials) and maps potential partner fit for nine buyer archetypes.

PW Consulting’s full research is intentionally operational rather than academic. Key deliverables that procurement and C‑suite teams can apply immediately include:

Scenario modelling toolkit: Pre‑built models that stress test supplier contracts under tariff shocks, wage increases, and allowance policy changes—allowing teams to quantify total cost of ownership across sourcing options.

Supplier scorecards and negotiation playbooks: Standardized templates to evaluate incumbent vendors across safety certification, delivery reliability, price indexation, and transition risk—accelerating vendor consolidation or diversification decisions.

Go‑to‑market and commercial models: Playbooks for launching in‑house rental services, adopting hybrid ownership‑rental approaches, or renegotiating branded supply agreements with manufacturers.

M&A and partnership heatmap: A prioritized list of acquisition or alliance themes—regional manufacturing consolidation, laundry network scale, and digital inventory platforms—with recommended financial metrics and integration KPIs.

Compliance and HR checklists: Ready‑to‑use templates that align uniform allowances, tax reporting, and minimum wage adjustments with procurement contracts and payroll systems.

Innovation radar: Assessment of material science advancements (comfort, flame resistance, antimicrobial finishes) and digital interventions (RFID tracking, automated wash analytics) with likely adoption timelines.

We recommend a three‑pronged approach for organizations preparing budgets and supply‑chain strategies for 2026:

Short‑term resilience: Immediately review contracts with indexation clauses and rerun supplier cost‑pass‑through scenarios in light of the 2025 tariff framework. Lock in strategic buffer inventories where economically justified and consider temporary nearshoring for critical PPE items.

Medium‑term flexibility: For 2026 RFP cycles, require modular contract terms that allow shifts between rental and purchase models, include clear hygiene and compliance SLAs, and embed ESG reporting obligations. Prioritize suppliers that can demonstrate multi‑modal fulfillment (manufacture + rental + laundering).

Longer‑term transformation: Invest in digital inventory tracking and predictive replacement algorithms that reduce waste and total cost of ownership. Target M&A or partnerships that fill capability gaps, particularly in sustainable textiles and scalable laundry/logistics footprints.

To make the recommendations concrete, the full report walks through applied scenarios such as:

A hospital chain optimizing scrubs and clinical apparel procurement under rising labor costs and tighter infection‑control mandates.

A multinational construction firm balancing on‑site PPE durability with the economics of centralized laundering and rental services across multiple jurisdictions.

A food‑service operator redesigning uniform allowance policies to comply with recent government ceilings while shifting to a hygiene‑certified rental program that lowers administrative overhead.

In line with our “trailer” approach, this release highlights the high‑level trends, practical frameworks, and strategic recommendations you need to pre‑position for 2026. To preserve the competitive value of the research and to encourage direct engagement, we have intentionally omitted detailed segment‑level quantitative tables and region/application‑specific breakdowns in this summary. The full report contains granular segmentation, regional and application forecasting, supplier market shares, and downloadable models that readers can use as inputs for internal business cases.

Leaders planning 2026 procurement, supply‑chain investments, or M&A should treat this preview as an early warning system. PW Consulting’s full Workwear and Uniforms Market report delivers the datasets, scenario models, and contract templates referenced above—paired with a strategic briefing session to translate findings into a tailored road map for your organization.

For procurement teams: request the supplier scorecards and the scenario modelling workbook.

For operations and HR: request the compliance checklists and allowance redesign playbook.

For investors and corporate strategy teams: request the M&A heatmap and risk‑adjusted valuation models.

The Workwear and Uniforms sector in 2026 will reward organizations that combine resilient sourcing, smart contracting, and targeted investment in service and digital capabilities. With the global market having expanded materially since 2020 and a clear trajectory to 2032, the decisions made next year about supplier partnerships, inventory strategy, and capital allocation will determine who captures the efficiency gains—and who absorbs the cost shocks. PW Consulting’s full report supplies the operational tools and strategic road maps to convert market visibility into competitive advantage.

For detailed analysis of this topic, please visit the official page:Workwear and Uniforms Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com