Smart (Intelligent) Toilet Seats Market — Strategic Preview for 2026 Decision‑Makers

PW Consulting presents a focused strategic preview of our forthcoming Smart (Intelligent) Toilet Seats Market report. This primer is crafted for executives, product strategists, investor relations teams, and category managers who must make high‑stakes decisions in 2026. It highlights the market’s trajectory, the levers that will determine competitive advantage, and the pragmatic analyses included in the full report — while intentionally withholding core segmentation tables and granular figures to encourage direct download of the full study.

Smart (Intelligent) Toilet Seats Market

Why this market matters to enterprise strategy in 2026

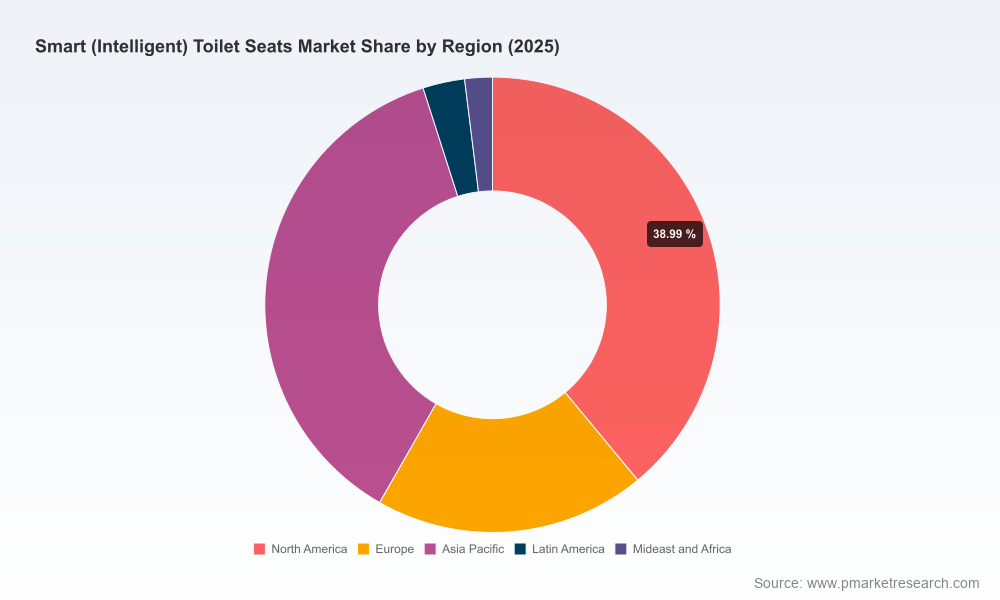

Smart toilet seats have moved from novelty to a mainstream category within connected bathroom ecosystems. After five years of rapid adoption, the global market size expanded from a modest base in 2020 to an established multi‑hundred million dollar market by 2025, and is projected to breach the billion‑dollar threshold by the end of the 2026–2032 forecast window. Our model indicates a compound annual growth rate (CAGR) of 7.85% across the forecast period, reflecting steady demand driven by home retrofit cycles, new residential construction, commercial washroom upgrades, and a growing emphasis on hygiene and accessibility.

Smart (Intelligent) Toilet Seats Market

For 2026 planning cycles, that trajectory means two strategic realities: (1) the category is large enough to justify dedicated product investments and channel strategies, and (2) growth is broad‑based rather than hyper‑concentrated, so competitive positioning, manufacturing efficiency, and go‑to‑market partnerships will determine winners and losers.

Smart (Intelligent) Toilet Seats Market

What PW Consulting’s full report delivers (practical highlights)

- Concise market sizing and validated time series (2020–2025 historical; 2026–2032 forecast) that you can integrate into business planning and investor materials.

- Scenario‑based demand forecasts with sensitivity to price erosion, component shortages, and regulatory shock events — each scenario calibrated to a realistic set of supply‑chain and macro assumptions.

- Go‑to‑market playbooks for three archetypal vendors: premium incumbent(s), value‑oriented disruptor(s), and OEM/ODM suppliers targeting private‑label channels.

- Product roadmap guidance: which features drive willingness‑to‑pay today (e.g., heated seats, bidet functions, water temperature control, autonomous cleaning) versus which features are becoming table stakes (connectivity, app pairing, RoHS compliance).

- Channel and pricing matrixes that map expected margin profiles across retail, professional trade, and B2B procurement routes — actionable for procurement and commercial teams.

- Regulatory and certification checklist for major markets, including compliance steps and typical timelines for CE, WaterSense/UPC, and RoHS pathways.

- Supplier and component risk heatmaps with mitigation options for electronics, heaters, and sensor modules — including alternative sourcing strategies and design for manufacturability (DFM) recommendations.

Market dynamics and near‑term catalysts

Three dynamics will dominate boardroom discussions in 2026:

- Feature commoditization vs. differentiation: Core hygiene and comfort features have migrated toward commoditization in several product lines. Vendors that differentiate through superior UX (app integration, personalized presets), reliable hygiene subsystems (self‑cleaning nozzles, antimicrobial materials), or compelling service models (longer warranties, on‑site installation) will capture premium segments.

- Supply‑side pressures: High‑end components (heating elements, sensors, microcontrollers) continue to command margin influence. The market already supports high‑ticket products due to electronics and sensor content; however, materials and logistics cost volatility can compress returns if pricing strategies are not agile.

- Regulatory and certification friction: Entry or scale‑up into major regions requires CE marking, RoHS compliance, and, for the U.S., WaterSense/UPC considerations. Our report maps the typical certification workflows and lead times to avoid costly go‑to‑market delays.

Competitive landscape — who to watch and why

The market shows moderate concentration, with the top three players accounting for a majority share and the top five consolidating well over half the market — a structure that favors scale economies in R&D, certification, and distribution. Key competitive attributes we analyzed include product breadth, channel strength, brand equity, and innovation pipelines.

- TOTO (Tokyo, Japan) — A global leader recognized for flagship electronic bidet systems and high‑end integrated units. TOTO’s emphasis on hygiene engineering and branded product families creates a durable moat in premium residential and hospitality segments. Their continued investments in product refinement and international distribution make them the archetypal incumbent to benchmark against.

- Kohler (Kohler, Wisconsin, United States) — Combines design credibility with showroom distribution and specification relationships in commercial projects. Recent product showcases emphasize convergence of design and intelligence, signaling a strategy to capture both aesthetic‑driven premium buyers and specification channels.

- American Standard (Florham Park, New Jersey, United States) — Focused on mainstream residential offerings with recognizable brand trust. Their product positioning is attractive for channel partners serving replacement markets in North America.

- Woodbridge (United States), BioBidet (United States), Bemis (Sheboygan Falls, Wisconsin, United States) — Competitive players in value and mid‑tier segments, often leveraging retail distribution and promotional placements to drive volume.

- China‑based players such as Casta‑Diva and Wealwell — More aggressive on price and rapid product iteration, these firms increasingly serve both domestic and exported demand. Their strength is in nimble development cycles and competitive manufacturing economics.

Recent market moves reinforce competitive dynamics: in early 2026 Kohler showcased new smart toilet platforms underscoring product convergence; 2025 saw targeted retail launches and next‑generation hardware announcements from Bemis, Topseat International, and Wealwell. These actions point to a market where incumbents refresh portfolios while new entrants press on cost and feature parity.

Regulatory, reimbursement, and sustainability considerations

- Certification burden: CE, RoHS, and the U.S. WaterSense/UPC pathways are non‑negotiable for credible access to major markets. Certification timelines and testing costs must be budgeted into product development cycles.

- Reimbursement reality: There are currently no dedicated CPT/DRG reimbursement codes for smart toilet seats — an important consideration for players targeting healthcare procurement. Commercial viability in healthcare settings depends on demonstrating operational benefits (infection control, fall mitigation, staff time savings) rather than relying on device reimbursement.

- Sustainability and materials: Material restrictions and end‑of‑life electronics handling are increasingly relevant for corporate procurement policies. Compliance with hazardous substance restrictions and transparent materials sourcing can be differentiators for B2B deals.

Strategic implications and recommended actions for 2026

To convert market growth into profitable share, PW Consulting recommends the following priority actions tailored by role:

- Manufacturers and OEMs: Prioritize modular architecture that separates commoditized subsystems (seat, heater, water delivery) from software and service layers that yield higher margins. Invest in certification early to avoid go‑to‑market friction.

- Product teams: Focus R&D on user‑facing reliability (robust nozzles, anti‑microbial surfaces) and software features that create stickiness (profiles, remote diagnostics). Consider tiered product lines to protect premium ASPs while competing on cost in retrofit channels.

- Commercial teams and retailers: Design bundled propositions that include installation and extended service to increase share of wallet. Leverage showroom experiences and integrated bathroom displays to translate features into perceived value.

- Private equity and investors: Look for targets with defensible IP in hygiene engineering, scalable manufacturing, and validated channel partnerships. Pay particular attention to firms with demonstrated ability to manage certification workflows and reduce component concentration risk.

How the full PW Consulting report supports implementation

The full report transforms insights into executable plans. Clients will receive downloadable datasets, supplier scorecards, and a ready‑to‑use board deck summarizing scenario outcomes and recommended capital allocation. We also provide a short engagement option — a two‑week rapid advisory package to align product roadmaps, pricing, and channel strategies to 2026 corporate goals.

Conclusion — what to do next

Smart toilet seats are a mature growth category with clear margins for strategic moves. The market’s solid CAGR and projected scale create a window for expansion — but only for companies that align product architecture, certification planning, and channel strategy. PW Consulting’s full report offers the granular segmentation, quantitative benchmarks, and tactical playbooks necessary to convert the category’s momentum into sustained, defendable commercial advantage.

To access the complete dataset, regional and application breakdowns, and downloadable strategic assets, please visit our report page. The preview above is intentionally high‑level; the full study contains the granular segmentation and scenario tables your 2026 planning teams will rely on.

For detailed analysis of this topic, please visit the official page:Smart (Intelligent) Toilet Seats Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com