PW Consulting: Strategic Imperatives from our Autonomous Mobile Robotic Machine Market Report (Base Year 2025)

Executive snapshot

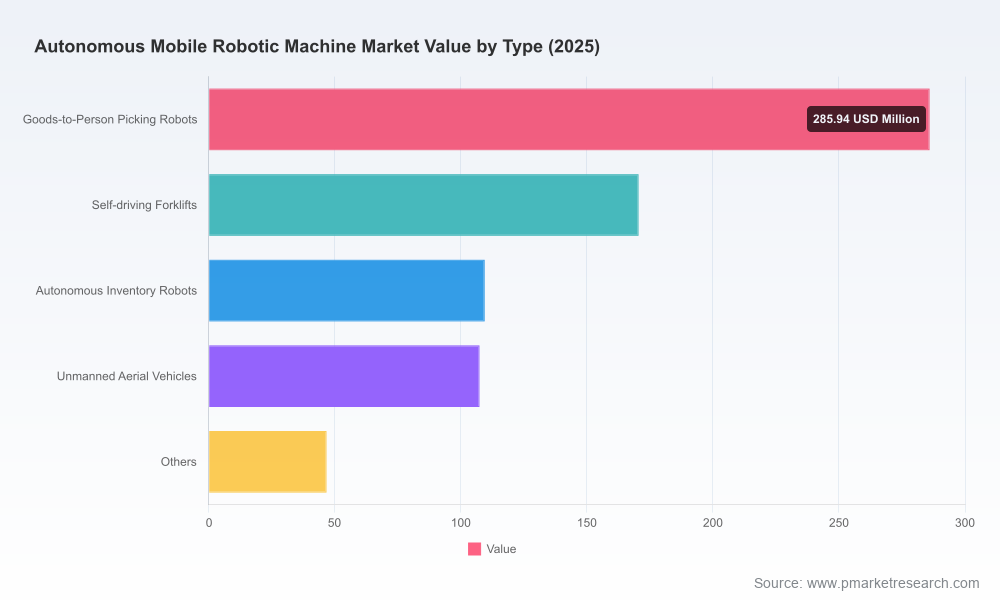

As organizations plan capital allocation and operational transformation for 2026, Autonomous Mobile Robotic (AMR) solutions are shifting from pilot-stage curiosity to a core lever for workforce productivity, resilience and cost containment. PW Consulting’s newest market study — with base year 2025 and a detailed forecast through 2032 — quantifies this transition and translates it into practical decision frameworks. The global AMR machine market, which PW tracks across 2020–2025 historicals and 2026–2032 forecasts, reached approximately USD 720 million in 2025 and is projected to expand at a compound annual growth rate (CAGR) of roughly 16.7% over the forecast horizon.

Autonomous Mobile Robotic Machine Market

Why this matters for 2026 enterprise decision-makers

Three converging forces make 2026 a strategic inflection point for AMR investments:

Autonomous Mobile Robotic Machine Market

- Resilient market growth: After robust historical expansion, our model forecasts an accelerating installed base and recurring software/service revenue, with market size more than doubling by the end of the forecast period. That growth trajectory signals expanding supplier maturity and a widening ecosystem of integrators, sensors and AI toolchains.

- Economics and labor dynamics: Persistent shortages of skilled labor combined with rising turnover and wage pressure are creating a quantifiable economic case for automation. The report provides ROI templates calibrated to regional labor cost curves and throughput uplift scenarios so procurement and operations leaders can build investment-grade business cases.

- Regulatory and supply-chain headwinds: New EU AI rules and evolving safety standards raise compliance costs and certification timelines — especially for navigation and decision-making stacks that rely on opaque models. At the same time, raw-material normalization (notably battery materials) is reducing cost volatility versus the spikes experienced earlier in the decade. PW’s analysis shows how these factors change deployment timing and vendor selection priorities.

What the report delivers — operational, boardroom-ready guidance

Rather than theoretical forecasting alone, this study is intentionally prescriptive for executives and deployment teams. Key actionable deliverables include:

Autonomous Mobile Robotic Machine Market

- Investment playbooks: step-by-step roadmaps for pilot-to-scale programs, with defined KPIs for cycle time, uptime, safety incidents and total landed cost per pick or transport task.

- TCO and ROI models: customizable templates that combine CAPEX, software subscription, integration, maintenance and labor-offset assumptions; scenarios show payback horizons under conservative, base and aggressive adoption cases.

- Vendor selection framework: a scoring matrix that weighs fleet orchestration software maturity, SLAs, system openness (APIs and ROS compatibility), certified safety features, and post-sale support footprints — designed for RFP and procurement use.

- Integration and change-management checklists: pragmatic items for facilities teams, IT, legal and HR to accelerate cross-functional adoption while minimizing operational disruption.

- Deployment playbooks by use-case archetype: pick-to-light and goods-to-person in high-throughput warehousing, autonomous forklifts in heavy-payload plants, inventory-scanning AMRs for cycle counts, and last-mile delivery pilots. For each archetype we map typical ROI levers, integration complexity and risk mitigations.

- Regulatory and compliance toolkit: an executive brief on EU AI Regulation implications, recommended documentation standards for explainability, and a compliance timeline to align product roadmaps with market access constraints.

Market dynamics and macro indicators

PW’s historical series from 2020 through 2025 shows steady adoption as product reliability and fleet orchestration matured. The modeled forecast through 2032 points to a more than twofold expansion from the 2025 base, reflecting a combination of recurring software/service revenue, replacement cycles and incremental adoption across adjacent verticals such as healthcare and manufacturing.

Importantly for strategic planners, concentration at the supplier level remains material but not prohibitive. The leading three vendors account for a significant share of market value, while the top five increase that concentration margin modestly — creating an environment where platform specialization and regional service footprints matter as much as headline features.

Competitive landscape — who matters and why

Our competitive analysis emphasizes vendor strategy, go-to-market moats and partnership ecosystems rather than raw shipment figures. Among the firms we profile in depth:

- Amazon Robotics: Operates at scale and combines proprietary hardware with a tightly integrated fleet and software stack. Their deployments illustrate end-to-end throughput engineering at very large fulfillment sites.

- Mobile Industrial Robots (MiR): Specialist in collaborative AMRs designed for mixed-fleet environments and fast-deployment scenarios. Their fleet software and focus on ease-of-integration make them a frequent choice for manufacturing conversions.

- Geek+: A major global player with cloud-first scheduling and goods-to-person leadership in select categories. Their approach shows how verticalized control software can improve utilization.

- Locus Robotics, KUKA, ABB, OMRON and others: These incumbents balance hardware depth, industrial certifications, and global service capabilities. Their offerings span from compact AMRs optimized for dynamic warehouses to heavy-payload AGV solutions for factories.

- Emerging specialists (Agility Robotics, GrayOrange, inVia Robotics and others): Focused on niche applications such as bipedal mobility, cloud-native orchestration or modular fleet services; these vendors often provide integration-friendly alternatives for unique site constraints.

Recent product and go-to-market activity in early 2026 underscores the rapid iteration in both hardware and software. Several vendors unveiled next-generation mobile manipulators, fleet managers and delivery robots at trade shows and launch events, signaling tightening competition on performance, developer ecosystems and integration speed.

Regulatory, materials and labor considerations

- Regulation: EU AI and safety regimes have already increased the cost of development and time-to-market for navigation and decisioning systems. Our regulatory scenario mapping shows which product attributes — transparency, auditability and safety certification — will determine access to the largest European customers.

- Raw materials: After earlier volatility, key battery material prices have stabilized relative to prior peaks. PW’s cost models reflect a reduced battery-cost tail risk but still emphasize design choices that mitigate long-term exposure to raw-material shifts.

- Labor: A global shortage of skilled operational technicians and warehouse workers is a primary demand driver. Our sensitivity analysis quantifies how varying labor-replacement rates materially change payback periods across geographies and verticals.

Decision framework for 2026 — what leaders should do now

For leadership teams planning AMR investments in 2026, PW recommends a three-track approach:

- De-risk with staged pilots: Start with high-frequency, low-complexity workflows to demonstrate throughput gains and collect telemetry. Use pilot data to validate vendor SLAs and refine site-specific simulation inputs for scale design.

- Prioritize openness and orchestration: Select solutions that expose APIs, support mixed-fleet orchestration and integrate with WMS/ERP. The true value accrues to operations that can orchestrate AMRs alongside conveyors, PLCs and manual workstations.

- Embed compliance into procurement: Require explainability and safety documentation as contractual deliverables. For firms targeting EU operations, demand roadmaps for regulatory alignment before procurement awards.

How PW’s report supports boardroom and program teams

Executives will find the report valuable as a single source that converts market-level growth projections into executable steps for procurement, operations and IT. The study equips teams to:

- Build defensible, investor-ready business cases that reflect both technology and regulatory risk.

- Shortlist vendors using a transparent scoring model and evidence-based integration timelines.

- Create governance structures for capacity planning, fleet lifecycle management and continuous improvement.

About the research and next steps

PW Consulting’s AMR Market Report synthesizes primary interviews, vendor benchmarking, deployment telemetry and an integrated market model. The study’s base year is 2025, with historical data back to 2020 and a forecast spanning 2026–2032. While this press release surfaces high-level growth trajectories and strategic implications, the full report contains detailed segmentation, scenario-model inputs, vendor scorecards and downloadable ROI calculators — content we intentionally reserve for report subscribers and clients.

For senior leaders evaluating AMR programs in 2026, the choice is not whether to experiment but how to sequence investments to capture the productivity dividend while managing regulatory and integration risk. PW Consulting’s research offers the operational playbooks and quantitative frameworks to make those decisions with confidence.

For detailed analysis of this topic, please visit the official page:Autonomous Mobile Robotic Machine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com