Terahertz Imaging Detection Industry Outlook Fueled by AI and Semiconductor Advancements

Other |

2026-05-18 11:38:42

PW Consulting’s newest Semitrailer Market report (base year 2025) delivers an evidence-based roadmap for executives making capital, product and go-to-market decisions in 2026. After tracking the sector through a dynamic 2020–2025 period and modeling multiple pathways to 2032, our core quantitative baseline shows the global semitrailer market at USD 213.0 Million in 2025, with a modeled compound annual growth rate (CAGR) of 5.6% through the 2026–2032 forecast window, bringing the market to approximately USD 311.7 Million by 2032. What follows is a strategic synthesis of the forces that will matter most next year — presented to inform boardroom tradeoffs while preserving the granular forecasts and vendor-level intelligence available in the full report.

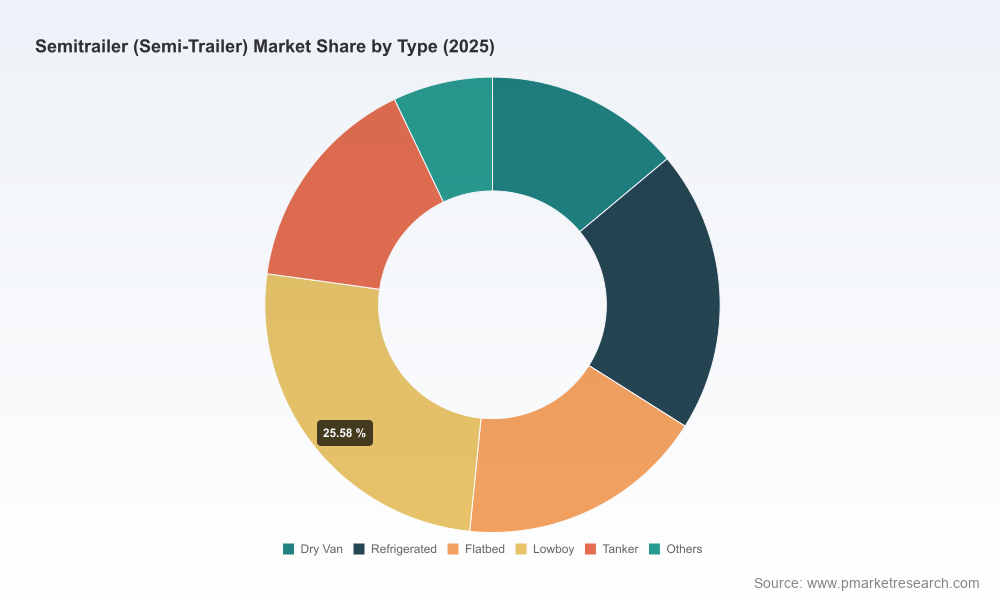

Semitrailer (Semi-Trailer) Market

Actionable foresight for capital allocation: The report translates market growth into demand profiles and unit economics under multiple cost and regulation scenarios, enabling CFOs to prioritize CAPEX and leasing strategies for 2026–2028.

Semitrailer (Semi-Trailer) Market

Risk-adjusted procurement playbooks: With raw material volatility and tariff dynamics front-of-mind, procurement leaders receive hedging frameworks and supplier segmentation to balance cost, lead time and quality trade-offs.

Semitrailer (Semi-Trailer) Market

Product and technology roadmaps tied to regulation: The analysis maps safety, emissions and automated-driving regulatory trajectories to feature adoption curves, helping product teams time investments in connectivity, active safety and lightweight materials.

M&A and partnership scouting: Given a fragmented industry structure, the report surfaces candidate acquisition and alliance types that can meaningfully shift market share or add complementary capabilities fast.

Demand trajectory and market scale: After steady expansion through 2020–2025, the market’s base scale entering 2026 positions incumbents and challengers to capture growth across freight, construction and specialized verticals. The 5.6% CAGR baseline captures a middle-path scenario where macro trade and investment conditions normalize while technology and regulation drive incremental fleet upgrades.

Input-cost pressure and margin compression: Steel price inflation (notably a pronounced year-on-year increase reported through April 2025) and ongoing tariffs on steel and aluminum imports continue to exert upward pressure on bill-of-materials and spare-parts costs. Manufacturers that lock in long-term buys, re-engineer designs for material efficiency, or secure nearshoring options will protect margins in 2026.

Regulatory inflection points: U.S. regulatory movement includes updates to rear-impact guard certification and planned standardization of automatic emergency braking on heavy trucks. These changes will accelerate retrofit and new-build demand for compliant equipment and produce winners among OEMs with rapid validation and integration capabilities.

Safety and sustainability as differentiators: Beyond compliance, commercial buyers increasingly treat safety ratings and lifecycle emissions as procurement criteria. Vendors that combine lightweight materials, validated crash performance and fuel-efficiency gains will unlock premium positioning in tender processes.

The semitrailer sector remains structurally fragmented (top-three concentration well below a simple-majority threshold), favoring nimble regional specialists and larger platform players that combine scale with targeted innovation. Key company archetypes and strategic implications are summarized below.

Material and lightweight innovators (example: Stoughton Trailers): Firms focused on aluminum and composites are leveraging weight reduction to deliver operational savings for fleets. Recent safety validation activity — including a high-profile rear-impact guard crash-test milestone in 2026 — has elevated the commercial value of validated safety claims. For 2026, OEMs that can pair material innovation with verified safety performance will gain procurement preference.

Integrated systems and connectivity leaders (example: Wabash National): Companies that embed telematics, predictive maintenance and advanced chassis designs are moving beyond hardware sales toward uptime-based commercial models. Expect pilots of subscription and performance-based pricing to proliferate next year, particularly among larger fleet customers.

Bulk and specialty carriers (example: Heil Trailer International, Polar Tank Trailer): Manufacturers specializing in tankers and bulk handling remain resilient, driven by sector-specific regulatory and hygiene requirements. Sanitary certifications and niche engineering patents translate into defensible pricing power in 2026.

High-volume assemblers and chassis specialists (example: Hyundai Translead, Fontaine): High-throughput manufacturers continue to compete on cost and delivery speed. Their advantage will hinge on supply-chain agility to mitigate raw-material swings and cross-border tariff exposure.

North American heavy-haul and forestry specialists (example: Pitts Trailers, MAC Trailer, Doepker, Reitnouer): Regional experts with customized engineering solutions will continue to capture specialized use-cases where standardization is low and service networks matter. These firms are attractive targets for partnerships with OEMs seeking quick access to niche end-markets.

Validated safety performance increases conversion velocity: High-profile crash-test validations in 2026 have shortened procurement lead times for safety-first fleets. Vendors who can present independent test results and retrofit pathways are seeing accelerated RFQ success.

Eco-product launches sharpen sustainability competition: New eco-focused trailer lines announced in recent years have set buyer expectations for lower lifecycle emissions. Expect sustainability claims to be table stakes in large RFPs for 2026.

Regulatory updates create both constraints and opportunities: Updates to rear-impact certification and impending AEB standardization will drive a wave of compliance-driven demand. Firms that pre-validate solutions and offer retrofit kits will capture aftermarket revenue.

We built the study for executives who need to convert market intelligence into executable plans. Key practical deliverables include:

Risk-adjusted demand scenarios tied to raw-material, tariff and regulatory permutations — with financial sensitivities for unit economics and total cost of ownership.

Competitive benchmarking and capability heatmaps that identify fast-to-scale differentiators (materials, safety validation, connectivity, manufacturing footprint).

Supplier risk matrix and procurement playbooks (including hedging options, nearshoring thresholds and preferred sourcing templates).

Product prioritization framework for allocating R&D and capex across lightweighting, refrigerated systems, tank/specialty platforms and active safety/telematics modules.

Aftermarket and services monetization models (maintenance-as-a-service, retrofits, extended warranties) with margin simulations.

M&A screen and partnership scorecards that identify bolt-on targets and JV structures to accelerate entry into niche end-markets.

Regulatory impact playbook mapping timing to compliance milestones and retrofit windows so legal, sales and engineering teams can synchronize go-to-market activities.

Prioritize validated safety and retrofit readiness. With regulatory headwinds and buyer risk aversion rising, proof-points (crash tests, certifications) convert into pricing power and shortened sales cycles.

Hedge material exposure while accelerating material-efficiency programs. Short-term procurement hedges should be paired with medium-term investments in design-for-low-cost-materials and recycling strategies.

Offer service-forward commercial models. Leasing, uptime guarantees and telematics-enabled preventive maintenance packages drive recurring revenue and strengthen customer stickiness.

Prepare modular, retrofitable architectures for automated-safety systems. Standardized interfaces reduce integration cost and create aftermarket cross-sell opportunities as AEB and other ADAS requirements roll out.

Assess selective M&A for capability fast-tracking. Given the sector’s fragmentation, targeted acquisitions of niche-engineering specialists or regional service networks can be a faster path to scale than organic expansion.

Align pricing strategy to total cost of ownership — not just upfront price. Fleet buyers increasingly procure with multi-year fuel, maintenance and uptime metrics in mind; vendors that can quantify and guarantee TCO improvements will win tenders.

Base case (planning anchor): Continued recovery and steady fleet renewal delivering the mid-range CAGR embedded in our baseline. Investments in lightweighting, safety, and connectivity yield incremental premium capture.

Upside: Accelerated regulatory adoption and faster electrification cycles push retrofit and replacement demand higher; connectivity-enabled service revenue scales faster, compressing payback periods for product investments.

Downside: Another cycle of raw-material spikes or escalation of trade barriers slows new-build demand and compresses margins. In this scenario, firms with nimble supply chains, local sourcing and flexible manufacturing win relative market share.

Entering 2026, semitrailer manufacturers and fleet purchasers operate in an environment where material costs, regulatory shifts and safety expectations are reshaping buyer decision criteria. The market’s baseline growth path offers attractive expansion, but the real competitive advantage will go to firms that translate product innovation into verifiable operational value, hedge supply-side risk, and adopt recurring-revenue business models. PW Consulting’s Semitrailer Market report supplies the scenario-tested quantitative backing and tactical playbooks to guide those choices — while our vendor-level benchmarking and region/application detail help you convert strategy into measurable results.

For the complete dataset, vendor-level share tables, regional and application splits, and the full suite of scenario models and procurement playbooks, access the comprehensive report on our website. PW Consulting’s team is available to brief leadership teams and support bespoke scenario modeling for board-level planning sessions in 2026.

For detailed analysis of this topic, please visit the official page:Semitrailer (Semi-Trailer) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com