Europe Laboratory Information Management Systems (LIMS) Market Size, Market Share, Emerging Trends, and Forecast by 2033

Other |

2026-06-09 10:10:43

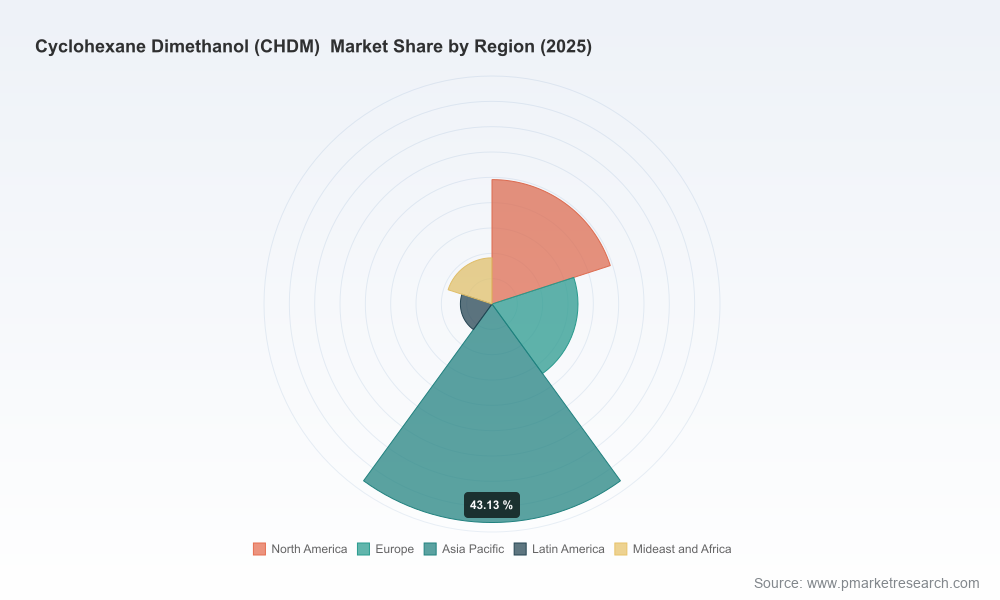

The Cyclohexane Dimethanol (CHDM) market has quietly matured into a predictable-growth specialty chemical with strategic exposures that matter to plastics, fibers, packaging, and advanced polymer value chains. Our latest market model—anchored to a 2025 base year and covering historical performance from 2020–2025 and forecasts for 2026–2032—shows the global CHDM market expanding at a compound annual growth rate (CAGR) of 4.2%. In revenue terms (USD, Million), the market rose from 128.45 in 2020 to 157.45 in 2025 and is projected to reach 209.76 by 2032. These headline figures mask important inflection points: customer specification shifts, regional capacity moves, and regulatory cost pressures that will alter margins and strategic options through the rest of the decade.

Cyclohexane Dimethanol (CHDM) Market

Steady growth but concentrated dynamics: CHDM’s steady CAGR belies pockets of supplier power and buyer dependence. Our concentration analysis shows the top three and top five suppliers collectively hold a material share of the market, creating oligopolistic dynamics that affect contract terms, spot availability, and pricing agility.

Cyclohexane Dimethanol (CHDM) Market

Supply-side normalization after capacity expansion: The industry experienced production capacity increases—notably an ~8% uplift in 2023—driven by Asia-Pacific investments targeting PETG and PCT demand. These capacity shifts have tempered short-term volatility but have also redistributed margin pools globally.

Cyclohexane Dimethanol (CHDM) Market

Rising cost of compliance: Environmental and sustainability-driven regulations have increased compliance and production costs substantially. Our synthesis of industry-source data indicates compliance costs have risen in the low double-digits (10–21%) since 2022, and production cost pressures have been amplified—near the 20% level on aggregate—changing the economics of older plants and altering investment calculus for greenfield projects.

Product differentiation is decisive: High-purity grades, specialty copolyesters, and tailor-made CHDM derivatives are where premium margins concentrate. Producers with high-purity capacity and strong formulation expertise are better positioned to capture value vs. commodity suppliers.

Demand migration across end-markets: Packaging, high-performance textiles, and engineering polymers continue to pull CHDM demand in different ways. Buyers in value-added segments (e.g., automotive coatings, PETG-based applications) are increasingly prioritizing quality consistency and traceable supply chains—favoring producers with robust quality systems and upstream integration.

Process and feedstock realities: CHDM production remains primarily based on catalytic hydrogenation routes (e.g., conversion from dimethyl terephthalate in two-stage processes). Feedstock availability and hydrogen pricing volatility are therefore non-trivial drivers of unit cost and operational risk.

Regulatory tailwinds and headwinds: Stricter emissions and process-effluent standards are raising closure and retrofit risk for older assets, while sustainability reporting and scope emissions disclosure are becoming procurement filters. The net effect: increased total cost of ownership for non-compliant suppliers and greater strategic value for low-emission profiles.

Commercial posture: Spot vs. contract balances are shifting. Buyers will prefer longer contracts for supply assurance but will demand clauses that reflect environmental compliance and decarbonization roadmaps. Suppliers that can offer value-added services (technical support, co-development of resins) will secure longer-term offtake and reduce margin erosion.

The CHDM supplier ecosystem comprises global chemical majors and regional specialists. Our report benchmarks capacity, quality positioning, and commercial strategies across leading producers. Selected profiles illustrate competitive dynamics that buyers and investors must watch in 2026:

Eastman Chemical Company (Kingsport, Tennessee) — Eastman’s CHDM-D product is positioned for saturated and unsaturated polyester resins, with clear emphasis on automotive, coatings, and packaging applications. Its portfolio advantage is technical depth in grade differentiation and established downstream relationships—an attractive model for customers seeking laddered quality and integrated supply assurances.

SK Chemicals (Seoul, South Korea) — SK has prioritized capacity and purity upgrades for high-performance copolyesters. Their recent trade show activity (Chinaplas 2026) underscores a commercial push to capture PETG and specialty resin applications. Expect SK to remain active in selective geographic and technical expansion.

Zhengzhou Meiya Chemical Products (Zhengzhou, China) — As a regional producer with broad product reach into fibers, bottles, and coatings, Meiya illustrates the competitive imperative of cost efficiency and supply responsiveness in domestic markets. Their scale in regional supply chains gives them an operational edge for local offtake agreements.

Kangheng Chemical (Zhangjiagang, China) — Kangheng’s focus on specialty polyester and tailored polymer applications highlights the niche strategy: competing on application-specific performance rather than commodity pricing alone. Such positioning reduces exposure to spot-cycle swings.

Collectively, the market concentration metrics show material clustering at the top end of the supplier base, reinforcing the importance of supplier selection, dual-sourcing strategies, and active risk management for buyers and investors alike.

Designed for strategic planners, procurement heads, and corporate development teams, the report combines proprietary modeling with primary interviews and scenario analysis. Key deliverables include:

Forward-looking demand model by end-market and polymer type from 2026–2032, stress-tested under energy and feedstock price scenarios.

Supply-side mapping with plant-level build-out timelines, commissioning risk scoring, and capacity utilization sensitivity—all calibrated to recent 2023–2025 expansions.

Cost curve and margin analysis incorporating feedstock, hydrogen, utilities, and environmental compliance load—enabling unit-cost benchmarking across suppliers and regions.

Supplier scorecards covering technical capability, quality grade breadth, sustainability credentials, and commercial flexibility (contract terms, lead times, and technical services).

Regulatory risk matrix and remediation cost estimates; scenario pathways for emissions regulation tightening and pricing implications for 2026–2030.

Actionable playbooks: negotiation frameworks for buyers, investment decision matrices for producers, and M&A screening templates for private equity and strategics targeting CHDM downstream integration.

To preserve competitive confidentiality and to align with our “preview” principle, the report highlights precise regional and application splits, detailed supplier capacity numbers, and price forecasts behind the paywall—information that materially influences negotiation positions and investment decisions.

For CHDM producers: prioritize retrofit investments to reduce emissions intensity and secure permitting; projects that lower the unit environmental cost profile will command price premiums and reduce regulatory risk.

For buyers and converters: shift procurement toward graded supplier scorecards that weigh technical support and sustainability credentials equally with price; incorporate short-term hedges to manage hydrogen/energy volatility.

For investors: target mid-cap producers with differentiated purity capabilities and contractual anchors in specialty end-markets; avoid greenfield bets in regions without clear feedstock advantages or regulatory certainty.

For M&A practitioners: use our scenario-driven valuation tool to stress-test EBITDA under tighter environmental regulation and slower demand growth—pay special attention to integration synergies in polyester and PETG downstream assets.

For product development teams: co-develop high-performance copolyesters with leading CHDM suppliers to lock in differentiation and reduce commoditization risk.

Announcements of new high-purity CHDM capacities or major upgrades, particularly in Asia-Pacific and integrated polymer complexes.

Regulatory rulings that materially increase emissions-related compliance costs or impose new effluent standards—these will change plant economics on short notice.

Feedstock and hydrogen price trajectories; persistent energy inflation will widen spreads and pressure older, less-efficient plants.

Commercial moves by leading suppliers (e.g., exclusive offtake agreements with resin makers or strategic partnerships) that could reshape access to premium segments.

CHDM will not be a headline commodity in most boardrooms, but it is a strategic lever for companies operating across polyester fibers, PET alternatives, and specialty resins. Our 2026-focused analysis converts market growth and concentration statistics into concrete decisions: where to invest, who to partner with, how to price, and when to lock supply. The public preview above is intended to surface the critical themes and near-term decision points. Our full report provides the granular, transaction-ready intelligence—regional and application breakdowns, supplier capacity sheets, and contract negotiation templates—that decision makers need to act with confidence in 2026.

Download the full PW Consulting CHDM Market Report to access the granular segmentation, supplier-level data, and downloadable models that support deal-making and procurement actions in 2026.

Contact our advisory team for a tailored briefing and scenario workshop focused on your company’s exposure to CHDM and downstream polymers.

For detailed analysis of this topic, please visit the official page:Cyclohexane Dimethanol (CHDM) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com