Windshield Wiper Blades Market — Strategic Outlook for 2026: PW Consulting Executive Brief

PW Consulting’s latest Windshield Wiper Blades Market report (base year 2025, forecast 2026–2032) equips senior executives with the actionable intelligence needed to make high‑stakes product, sourcing, channel and M&A decisions during 2026. Our top‑line model shows a resilient market trajectory — recovering from the early‑decade fluctuations and expanding at a compound annual growth rate (CAGR) of approximately 5.2% through 2032. The market grew steadily from the early 2020s, reached a decisive inflection by 2025, and is projected to continue its upward path to the end of the forecast period. This brief explains where to focus resources this year, what competitive moves will matter, and which operational levers will protect margin and market share as the industry modernizes.

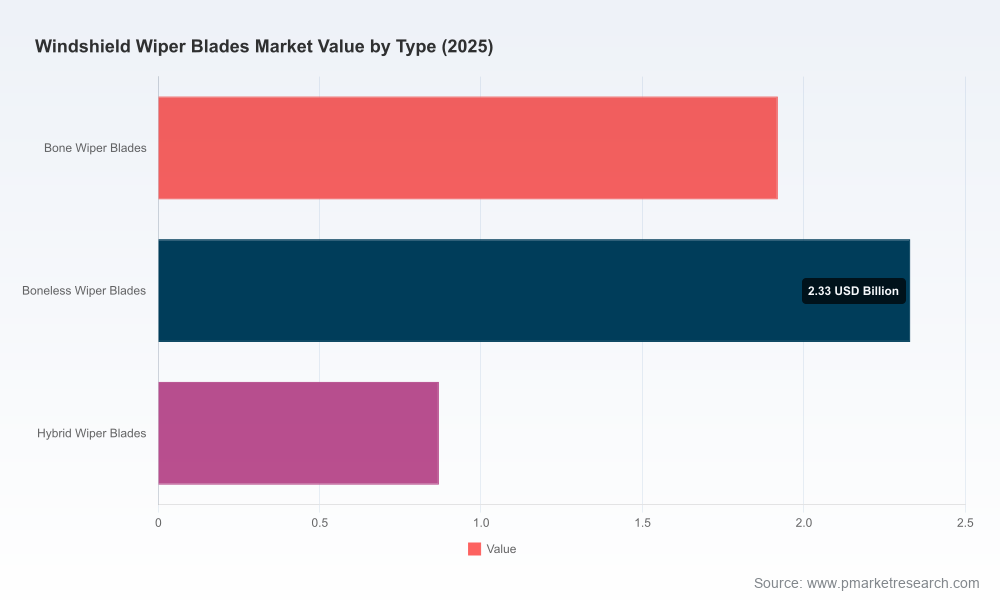

Windshield Wiper Blades Market

Why this report matters to 2026 decision‑makers

- Timing of strategic bets: 2026 is a pivot year for wiper manufacturers and component buyers — technological adoption (beam and hybrid formats, silicone formulations), tightened regulatory expectations on safety and sustainability, and pronounced aftermarket vs. OEM mix shifts create asymmetric opportunities for first movers.

- Risk mitigation vs. value capture: recent high‑visibility product quality events have spotlighted warranty, recall and reputational exposure; simultaneously, premiumization trends (longer‑life materials and performance variants) offer margin expansion if supported by supply chain resilience.

- Resource allocation: a clear, quantified scenario framework enables CFOs to allocate R&D, inventory and M&A capital to maximize IRR in a market growing mid‑single digits annually.

What’s inside the PW Consulting report (practical outputs)

- Integrated market model (2020–2032) with downloadable assumptions and sensitivity levers — demand drivers, replacement cycles, vehicle parc and replacement penetration rates.

- Scenario analysis (base, upside, downside) calibrated to material price shocks, regulatory shifts, and recall events — with P&L and cashflow impact for a typical supplier portfolio.

- Competitive benchmarking and capability scorecards for leading OEM and aftermarket suppliers (product breadth, IP, channel strength, manufacturing footprint, quality certifications).

- Go‑to‑market playbooks — differentiated strategies for incumbents, challengers and component specialists across OEM, professional workshop and DIY channels.

- Supplier risk register and sourcing playbook covering raw material concentration, alternative feedstocks (silicone vs. natural/synthetic rubber), and nearshoring implications.

- Commercial tools — pricing ladders, promotional elasticity matrices, channel margin models and inventory turnover targets designed for 2026 execution.

- M&A and partnership playbook — target screen, valuation templates, integration pitfalls and sample earn‑out structures for consolidation or bolt‑on technology acquisitions.

Selected analytical highlights (what you’ll use immediately)

Macro momentum: The market’s mid‑single‑digit CAGR to 2032 reflects a combination of steady replacement demand, incremental OEM content growth (beam and hybrid fitments), and premiumization as consumers and fleets trade up to longer‑life materials. Management teams should plan portfolios accordingly — balancing high‑margin premium SKUs with efficient core offerings to defend share in price‑sensitive channels.

Windshield Wiper Blades Market

Concentration and competitive dynamics: Market concentration is meaningful but not monopolistic. The three largest suppliers control a substantial minority of the market, and the five largest consolidate a clear majority of commercial influence. That structure creates room for scale‑focused incumbents to sustain margins while offering well‑executed challengers tactical entry opportunities through product differentiation or geographic focus.

Windshield Wiper Blades Market

Technology and materials: Beam‑style blades continue to gain share due to uniform pressure distribution and aesthetic integration with modern vehicle designs. Silicone formulations are increasingly marketed as a premium, longer‑life option — with industry claims of materially longer service life versus traditional rubber. These material shifts have implications for BOM costs, supplier selection, and warranty exposure.

Quality, regulation and safety: High‑profile safety events have elevated regulatory and procurement scrutiny. A major automaker recall in 2026 related to defective wiper components underscores that supplier quality and traceability are now strategic defenses, not just compliance items. ISO‑class quality certifications remain table stakes for suppliers targeting OEM and professional channels.

Competitive positioning: reading the field

Our competitor analysis synthesizes product portfolios, innovation pipelines and channel strategies to create entrant and incumbent archetypes. Key observations include:

- Aftermarket specialists who combine cost efficiency with targeted premium SKUs can capture DIY and professional channels by emphasizing availability, ease of fit and clear warranty propositions.

- Legacy innovators with strong patent portfolios and OEM relationships retain a technical lead in hybrid and bespoke applications, making them natural consolidation anchors for buyers seeking IP and manufacturing scale.

- Automotive OEM parts brands and large tier suppliers leverage brand trust and OE fitment to command price premiums in the replacement segment; this advantage strengthens with quality certifications and demonstrated safety performance.

- Newermarket entrants and regional OEM suppliers from Asia are competitive on cost and increasingly on tech — making selective partnerships (co‑development, licensing) attractive for incumbents seeking rapid capability augmentation.

Notable market movements in 2026 reinforce these dynamics: a prominent aftermarket supplier launched a premium line positioned on durability and streak‑free visibility, while a major recall highlighted both commercial tailwinds for replacement demand and regulatory risks for suppliers failing to demonstrate robust quality systems.

Actionable recommendations (90‑day, 12‑month, 36‑month)

- 90 days

- Conduct an immediate supplier quality and recall exposure audit (including spare part traceability for critical fitments).

- Run a pilot SKU rationalization to reallocate merchandising real estate to premium long‑life formulations in professional channels.

- Begin a commercial test of silicone variants in selected fleet accounts to measure perceived value and lifecycle economics.

- 12 months

- Qualify for industry quality certifications and publish a warranty policy aligned with OEM expectations to reduce procurement friction.

- Implement a two‑speed product architecture: defensive core SKUs for volume channels and a premium family for margin expansion supported by a targeted marketing campaign.

- Pursue one strategic partnership or bolt‑on acquisition that accelerates access to silicone compounding or aerodynamic beam technology.

- 36 months

- Deploy vertical integration options for critical feedstocks where price volatility materially affects gross margin.

- Scale digital direct‑to‑consumer channels and integrative aftercare services (subscription replacement, fleet maintenance contracts) to lock recurring revenue.

- Consider M&A plays to consolidate regional fragmentation and secure IP assets from specialized beam/hybrid innovators.

Implications for budgeting, KPIs and risk management in 2026

With the market expanding at a mid‑single‑digit rate, companies should reframe KPIs to capture lifetime value shifts driven by premiumization and longevity claims. Suggested shifts include:

- Move from unit sales to value metrics: emphasize revenue per SKU, aftermarket margin mix and recurring revenue from fleet contracts.

- Allocate R&D spend to materials science (silicone compounding, UV resistance) and aerodynamics; measure success by lifecycle extension rather than unit performance alone.

- Increase capex for flexible manufacturing cells that can switch between beam, hybrid and conventional geometries to respond quickly to OEM design changes.

- Embed recall readiness into the enterprise risk framework with defined playbooks and insurance structures to contain brand and financial exposure.

How to use the full report

This executive brief highlights the strategic contours and immediate moves that will matter in 2026. The full PW Consulting report contains the complete market model, granular scenario outputs, downloadable competitor scorecards and a prioritized action plan tailored to three corporate archetypes (OEM supplier, aftermarket consolidator, focused specialist). Importantly, sub‑segment datasets (product type, region, application splits), proprietary price‑elasticity matrices and target acquisition screens are reserved for report subscribers — a deliberate design to protect the analytical core while enabling clients to act decisively.

To obtain the full dataset, interactive model and bespoke advisory options (workshops, transaction support, implementation sprints), visit PW Consulting’s Windshield Wiper Blades Market report page or contact our industry team. For 2026, firms that balance disciplined quality controls, selective premiumization, and nimble supply‑chain strategies will capture disproportionate value in a market growing predictably but changing technically and commercially.

For detailed analysis of this topic, please visit the official page:Windshield Wiper Blades Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com