Email logins associated with PayPal

Gardening |

2026-05-31 11:47:30

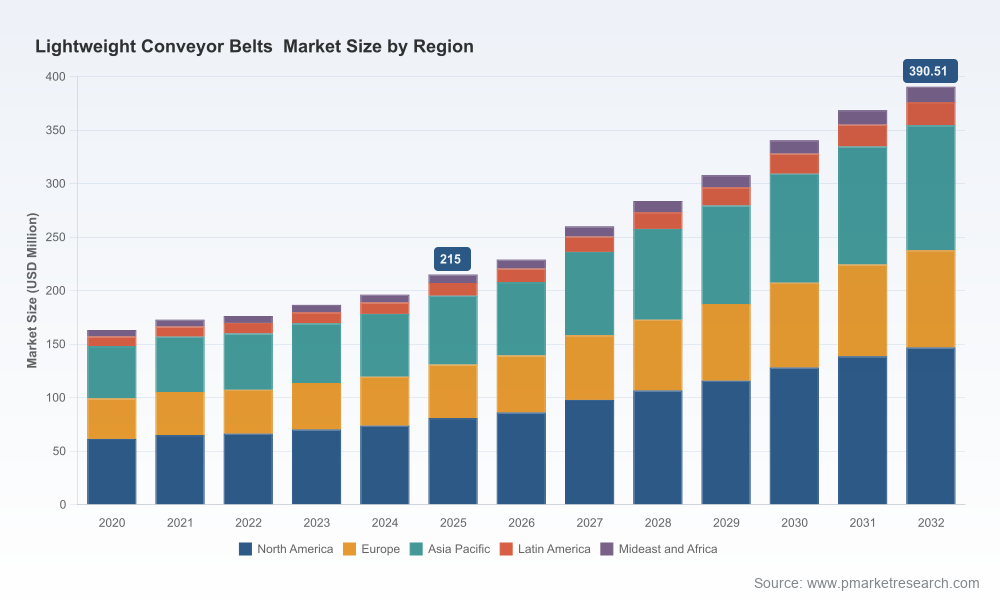

PW Consulting’s latest market research on Lightweight Conveyor Belts positions procurement leaders, OEM strategists and private-equity investors to make decisive moves in 2026. Built on a 2025 base and covering historical performance from 2020–2025 with a validated forecast through 2032, the study models a sector expanding at a sustained compound annual growth rate (CAGR) of 8.9%. Our market model projects robust expansion across the forecast window, reflecting accelerating automation, higher hygiene standards in food and life‑science processing, and broader logistics modernization.

Lightweight Conveyor Belts Market

The report synthesizes a multi-year time series (2020–2025) and a detailed scenario forecast (2026–2032) so that commercial leaders can translate industry momentum into capital and operating plans. The aggregate market size grows materially over the forecast period, reflecting both unit demand growth and a steady premiumization of product portfolios as buyers prioritize hygienic materials, modularity and service-enabled products.

Lightweight Conveyor Belts Market

From a strategic planning standpoint, the implications are clear:

Lightweight Conveyor Belts Market

Three demand vectors are shaping the market’s rhythm: regulatory and food-safety requirements that favor certified thermoplastics and polyurethane solutions; the rapid expansion of automated logistics where modular and snag‑resistant belting is preferred; and sustainability and circularity pressures that push manufacturers toward water‑based chemistries and recyclable constructions.

On the cost side, specific raw‑material dynamics are exerting pressure on polyurethane-based products. Regional price movements in isocyanate feedstocks have increased input costs meaningfully in recent quarters, forcing producers to revisit sourcing strategies and pass-through mechanisms. The result is a two-speed market where suppliers with vertically integrated feedstock access or water‑based formulations enjoy margin resilience.

Food-contact and hygiene requirements are not optional. Compliance with FDA and EU food contact regulations has become table-stakes for suppliers targeting processing and retail food chains. Concurrently, adherence to international standards for conveyor safety and ergonomics (including recently emphasized design guidance) is reshaping product specifications; ergonomics and operator-safety features are increasingly factored into procurement KPIs.

These regulatory constraints create both risk and opportunity:

The market remains moderately concentrated: the top three players account for a significant portion of industry revenue and the top five collectively represent a majority. That concentration accelerates supplier benchmarking and strategic sourcing programs among end users.

Our analysis of leading suppliers highlights distinct go‑to‑market archetypes and near‑term moves:

Recent product launches and capacity moves observed in 2026 — including modular belting extensions, new hygienic material introductions, tooling for consistent installation, and selective capacity increases for water‑based polyurethane — underscore an industry focused on hygiene, uptime and supply security.

Our market study is intentionally operational. It equips leadership teams with the analytical tools needed to translate insight into action across sourcing, product development, M&A and regulatory compliance:

Importantly, the report couples quantitative forecasting (historical 2020–2025 and forward‑looking 2026–2032 scenarios) with templates and checklists designed for immediate application in tendering, RFP evaluation and plant‑level specification updates.

In the spirit of providing high‑impact, decision‑ready intelligence while protecting the full commercial utility of our primary research, this release highlights the study’s strategic conclusions and actionable frameworks. The full report contains granular datasets — including segmented regional and application-level demand tables, vendor-level financial metrics, and downloadable procurement templates — which are reserved for subscribers and clients. These proprietary tables and the accompanying sensitivity calculators are essential for executing the tactical moves described above.

Leaders who must translate the 2026 outlook into procurement plans, product roadmaps or diligence workstreams should schedule a briefing with PW Consulting. Our analyst team can walk through the report’s quantitative scenarios, the supplier scorecards and the implementation templates, and provide a tailored impact assessment for your business unit or portfolio.

PW Consulting’s Lightweight Conveyor Belts Market study is timed to inform 2026 CapEx cycles and supplier negotiations. For organizations that require a fast, executable plan to capture upside or mitigate risk in the year ahead, the report provides the playbook — and our advisory team will operationalize it with you.

For detailed analysis of this topic, please visit the official page:Lightweight Conveyor Belts Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com