Shampoo Market Size, Share, Trends, Key Drivers, Demand and Opportunity Analysis

Other |

2026-03-22 05:35:44

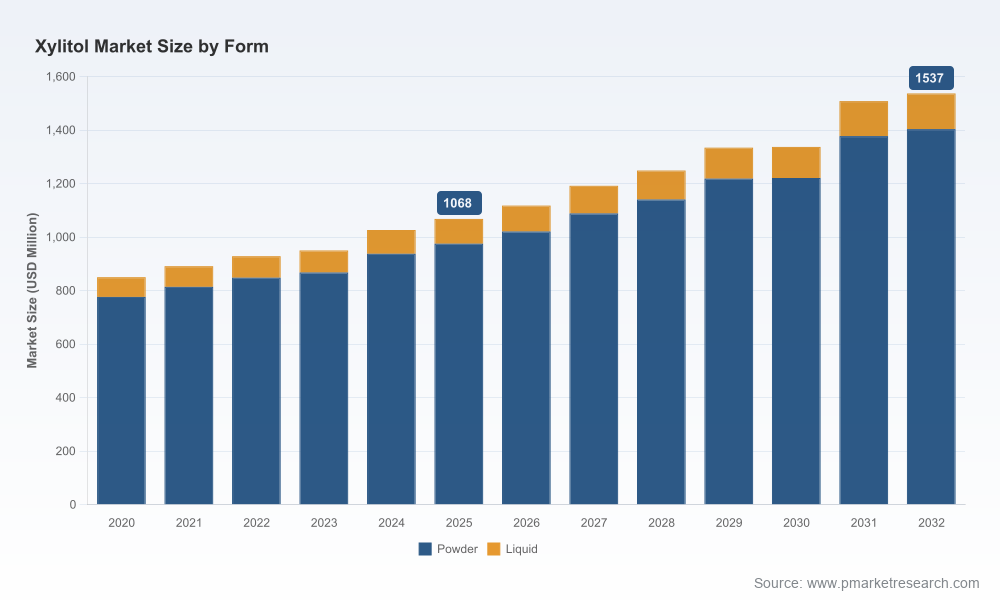

PW Consulting today releases a focused industry brief designed as the definitive strategic primer for executives making xylitol-related decisions in 2026. Drawing on a base-year assessment of 2025 (historical window 2020–2025) and a forward-looking forecast to 2032, the report translates market movements into clear options for product, supply chain and M&A strategies without exposing proprietary segmentation detail in this public notice. The headline metrics set the frame: global market value expanded from USD 850 Million in 2020 to USD 1,068 Million in 2025, and is projected to reach approximately USD 1,537 Million by 2032 under a central-case compound annual growth rate of 5.25% for the 2026–2032 forecast period.

Xylitol Market

Timing of capacity and partnerships: The market is evolving steadily rather than explosively—growth is mid-single digits CAGR—so 2026 is a window for value-accretive capacity investments and selective commercial partnerships rather than broad, high-risk greenfield programs.

Xylitol Market

Regulatory and demand tailwinds are aligned: Policy incentives and public health endorsements in key jurisdictions are accelerating adoption in targeted end-markets, making regulatory intelligence and fast-to-market product formulations decisive competitive levers.

Xylitol Market

Consolidation optics: Market concentration is material—our analysis shows the top three firms control a majority share and the top five an even larger share—so M&A and supply agreements should be evaluated against incumbent scale and route-to-market advantages.

From a macro standpoint, the market’s progression between 2020 and 2025 proves steady, and the forecast through 2032 signals continued, sustainable expansion. For corporate strategists that translates into three practical conclusions: optimize existing portfolios for margin resilience, build selective partnerships to secure offtake and specialty formulations, and prioritize regulatory and channel intelligence to accelerate new product launches. While we publish aggregate market trajectory and concentration indicators publicly, the full econometric tables, demand-by-application scenarios and segmented pricing curves are available only via the full report.

Methodology and transparent market sizing: detailed base assumptions, data sources, and sensitivity tests used to reconcile supply-side production statistics with downstream demand indicators for 2020–2025 and projected through 2032.

Scenario analysis and price outlooks: three pricing and volume scenarios (base, upside, downside) with triggers tied to feedstock availability, energy cost shocks and regulatory adoption timelines—delivered as decision-support charts and breakpoint tables.

Supply chain mapping: origin-to-consumer flow diagrams, bottleneck heatmaps, and a supplier risk index—designed to help procurement teams prioritize hedging and sourcing strategies.

Commercial playbooks: go-to-market modules for food & beverage formulators, oral care producers and pharmaceutical ingredient buyers, including sample commercial terms and co-development frameworks.

M&A and partnership toolkit: target-screening criteria, synergies capture playbooks, and integration checklists tailored for xylitol assets—especially useful given the market’s existing concentration dynamics.

Regulatory tracker and use-case briefs: jurisdiction-by-jurisdiction regulatory implications—including the accelerating EU policy environment around reduced-sugar products and recognized dental health endorsements that meaningfully lower market-entry friction for certain applications.

Cargill, Incorporated — As a leader in industrial polyols, Cargill has been actively expanding production footprint and commercial supply agreements. Recent capacity openings and multi-year supply contracts underscore a strategy focused on securing major food and beverage customers and integrating upstream logistics to protect margins.

Roquette Frères SA — Roquette remains an innovation and scale player in polyols with application-led product variants supporting food, pharmaceutical and health uses. Their emphasis on application-specific ingredients positions them as an incumbent partner for premium formulations.

Ingredion Incorporated — Positioned to serve clean-label and sugar-reduction trends, Ingredion’s recent product introductions targeting confectionery and snack manufacturers signal a commercial offensive toward formulators seeking natural-sweetener alternatives.

Merck KGaA (Sigma-Aldrich) — Serving research and selective industrial segments, Merck’s role is often as a qualification partner for specialty and regulated applications where consistent analytical supply and documentation matter.

International Flavors & Fragrances (IFF / Danisco) — A pioneer in commercial xylitol production, IFF continues to focus on sustainable feedstock routes and industrial-scale product variants, particularly where sustainability claims are a commercial differentiator.

Recent notable moves—facility capacity additions in Europe, product launches targeting reduced-sugar confectionery, regulatory approvals enabling regional scale-up, and long-term supply accords—are high-signal indicators of how incumbents are converting demand certainty into commercial advantage. These moves create both barriers to entry and partnership opportunities for mid-market players.

Feedstock and input price volatility: Raw-material sourcing remains a key margin determinant. Corn-derived feedstocks and woody biomass dominate production pathways; availability and energy-price movements materially influence unit economics. Procurement teams must therefore model feedstock scenarios and secure blended sourcing to reduce exposure.

Regulatory environment: Pro-innovation regulatory stances in some jurisdictions—alongside public-health endorsements for certain oral-care benefits—accelerate adoption in target segments. However, differing rules across geographies require tailored commercialization timelines.

Concentration and market structure: High concentration among leading suppliers means pricing power shifts with capacity changes. Buyers should expect periodic supply tightness following major capacity disruptions or rapid demand increases in adjacent categories.

Sustainability and feedstock sourcing: Claims around sustainable production (e.g., wood-based versus agricultural residues) increasingly influence retailer and brand procurement choices, raising the premium for traceable, low-impact supply chains.

Implement a dual-sourcing strategy: Hedge feedstock risk by qualifying both agricultural-residue and woody-biomass suppliers and use indexed contracts to mitigate short-run price shocks.

Pursue selective co-development deals with formulation leaders: Fast-track product validation by partnering with established taste and application specialists rather than building all capabilities in-house.

Prioritize regulatory and clinical evidence generation: Where oral-care or dental-benefit claims accelerate uptake, invest in clinical or real-world studies to secure label claims and procurement preference.

Target bolt-on M&A with integration playbooks: Given the market concentration, small to mid-sized assets with complementary routes-to-market or specialty applications are the most accretive acquisition candidates.

Differentiate on sustainability credentials: Build traceability and low-carbon narratives into commercial propositions to capture premium channels and retail programs.

Adopt dynamic pricing and contract models: Use flexible pricing mechanisms tied to feedstock indices and capacity utilization to protect margins while remaining competitive in tender processes.

Our xylitol industry brief is structured to convert market intelligence into executable initiatives. We combine quantitative scenario models with qualitative commercial frameworks so that R&D leaders, procurement heads, and corporate development teams can align decisions quickly in 2026. The public summary above signals our rigor—full diagnostics, segmented forecasts, supplier scorecards, and proprietary valuation templates are compiled into the full report for subscribers and private clients.

This release intentionally highlights strategic insights while conserving the granular segmentation and financial schedules that underpin transaction and operational decisions. For the complete data tables, regional and application breakdowns, supplier-by-supplier benchmarking, and downloadable decision-support tools, please consult the full PW Consulting Xylitol Market report available through our research portal or contact your PW Consulting account lead. The full deliverable is the operational reference that corporates and investors will use to finalize 2026 strategies.

For decision-makers who need a rapid executive briefing, PW Consulting also offers bespoke workshops that map the report’s scenarios directly onto your commercial and supply-chain plans—helping firms turn the 5.25% CAGR environment into defensible growth and margin expansion strategies.

For detailed analysis of this topic, please visit the official page:Xylitol Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com