Cervical Retractors Market Size, Share, Driving Trends, and Industry Forecast by 2033

Other |

2026-06-26 09:45:20

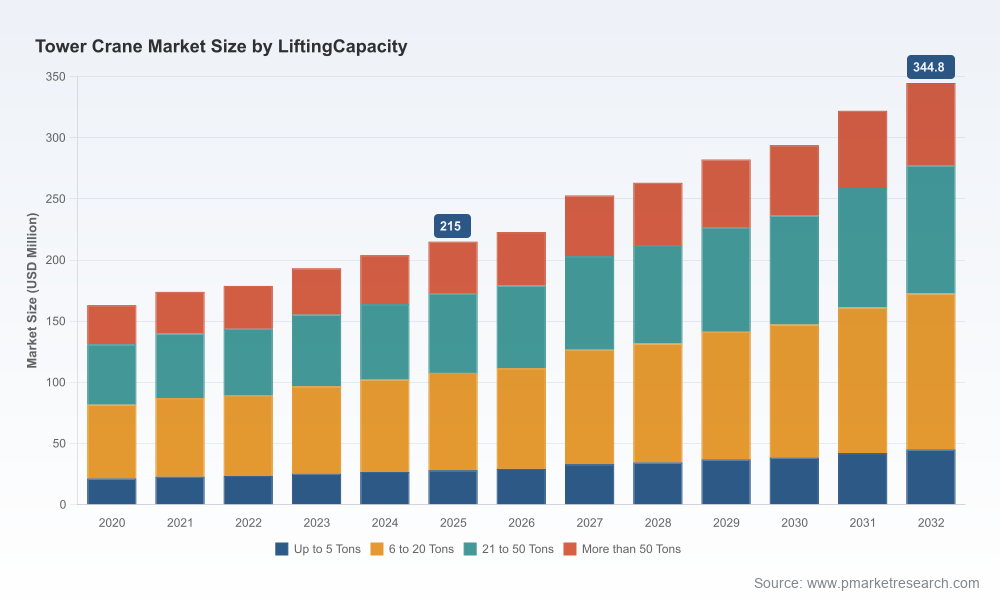

PW Consulting’s latest Tower Crane Market report—based on a 2025 base year and projecting through 2032—translates complex market signals into a pragmatic playbook for executives, investors and project leaders. The global market, having expanded steadily through the early 2020s, is forecast to grow at a compound annual growth rate (CAGR) of 6.1% over the 2026–2032 horizon. From a strategic standpoint, this pace of growth creates both runway and urgency: it supports expansion and product investment, but also compresses the time window for suppliers and contractors to capture share before competitive advantages become table stakes.

Tower Crane Market

Momentum and inflection: After a multi-year recovery phase, the market entered 2026 on a structurally stronger footing. Macro-driven construction activity, coupled with a trend toward taller and more complex builds, is accelerating demand for higher-performance tower crane platforms.

Tower Crane Market

Consolidation and concentration: Market concentration is meaningful—our CR3 and CR5 metrics underline that leading OEMs control a dominant portion of global supply, and top-tier vendors continue to widen capability gaps through product innovation and channel investments.

Tower Crane Market

Regulatory and raw-material variability: New permitting regimes and volatile steel input costs are reshaping procurement, inventory and risk strategies for both owners and manufacturers.

Actionable market sizing and growth scenarios: We provide scenario-based forecasts anchored to the 2025 baseline and run stress-tests across demand shocks, tariff/regulatory shifts and input-cost movements so you can pressure-test investment cases.

Competitive benchmarking: Multi-dimensional vendor scorecards that compare offerings on lifting capacity architecture, modularity, erection/destruction time, digital assistance suites, and total cost of ownership—designed for procurement negotiation and OEM selection.

Commercial playbooks: Tender-winning configurations, leasing vs. ownership decision frameworks, and go-to-market strategies for manufacturers seeking to expand channel footprint or for investors evaluating aftermarket plays.

Supply chain and procurement safeguards: Line-item sensitivity models that quantify margin exposure to steel price movement and logistics disruptions, together with mitigation pathways for contract drafting and supplier diversification.

Regulatory monitoring and compliance maps: Early-warning trackers for type-approval trends and jurisdictional permitting, enabling compliance-first deployment planning and equipment certification strategies.

Executive dashboards and data annexes: Gated model sheets, regional and application splits, and model-level pricing arrays (note: the granular segment tables are reserved for report subscribers).

Performance differentiation through modularity and intelligence: Our field work and OEM interviews confirm that buyers increasingly prize cranes that reduce site erection time, lower crew requirements, and integrate telematics for preventive maintenance. OEMs that package mechanical robustness with software-driven uptime tools will win contract preference and rental longevity.

Aftermarket margins as a strategic lever: Given the elevated concentration in OEM supply, spare-parts, retrofit kits and service contracts offer outsized margin opportunity—and are a key retention tool for fleet operators and rental companies.

Regulatory tightening raises barriers and creates windows: New permitting rules in certain jurisdictions are increasing compliance costs but also creating first-mover advantages for vendors that secure type-approvals and establish local service footprints early.

Input cost pressure: Steel and other commodity movements have a direct pass-through effect on manufacturing margins and lead times. Companies should adopt indexed procurement clauses and strategic forward buying to stabilize quoting and delivery reliability.

The sector’s top vendors span legacy European engineering houses and high-scale Asian manufacturers. Each competitor pursues a distinct value proposition that shapes procurement and partnership choices.

Liebherr Group (Biberach an der Riß, Germany) — Strengths: advanced HC-L luffing-jib and flat-top series with intelligent assistance systems. Strategic implication: Liebherr’s focus on reduced erection time and high-capacity models positions it well for premium project segments and public-sector infrastructure deployments where uptime and safety credentials are prioritized.

The Manitowoc Company / Potain (Manitowoc, USA) — Strengths: modular tower cranes and self-erecting models that emphasize site versatility. Strategic implication: Potain’s modularity is advantageous for rental fleets and projects with mixed-use or constrained urban footprints.

Terex Corporation (Norwalk, USA) — Strengths: CTL luffing-jib series with advanced controls and safety features. Strategic implication: Terex’s strong controls suite makes it a front-runner for clients seeking integrated digital safety and operator-assist functionality.

Zoomlion & XCMG (Changsha and Xuzhou, China) — Strengths: European-model and heavy-duty flat-top and XGT series for high-rise and export markets. Strategic implication: These manufacturers combine scale economics with rapid type-approval efforts to challenge incumbents on price/performance in fast-growing regions.

SANY Group (Changsha, China) — Strengths: SFT/STT modular designs and high safety standards. Strategic implication: Rapid certification wins in targeted jurisdictions point to an aggressive expansion strategy focused on regulatory legitimacy and local partnerships.

European specialists (Raimondi, Wolffkran, Comansa, JASO, Favelle) — Strengths: niche engineering, compact and heavy-duty models, and regional service excellence. Strategic implication: These players win where project-specific customization, local support, and premium engineering are decisive procurement criteria.

Collectively, the top three firms account for a material share of market shipments, while the top five capture roughly three quarters of industry revenue—illustrating a market where scale and product breadth materially affect competitive dynamics.

Product showcases and integration: Recent exhibitions and product integrations are not mere marketing—suppliers are committing capital to extend lifting envelopes and reduce out-of-service time, forcing buyers to reassess lifecycle cost models.

Type-approval momentum: An uptick in jurisdictional approvals is accelerating equipment turnover in certain metropolitan markets; vendors who secured approvals early are translating that into channel wins.

Partnerships and distributor expansion: New distributor appointments and dealer events indicate a shift toward localized service networks—critical for compliance-driven procurements and for capturing rental-market share.

Commodity exposure: Steel price volatility remains a chief sensitivity. Management teams should stress-test bid models to a range of steel-price scenarios and adopt hedging or contractual mechanisms where possible.

Permitting complexity: New permit requirements in select U.S. states and accelerated type-approval activity in major city-states mean that route-to-market timelines can vary materially by jurisdiction—affecting delivery schedules and contract acceptance.

Concentration risk: High market concentration increases counterparty risk for buyers dependent on a narrow set of OEMs for critical parts. Diversification strategies and aftermarket partnerships can mitigate single-source exposures.

For OEMs: Prioritize modular platforms with integrated telematics, accelerate type-approval pipelines in key urban and export markets, and lock strategic channel partnerships to shorten time-to-deployment.

For rental companies and contractors: Rebalance fleets toward high-uptime, fast-erection units; negotiate service-inclusive contracts; and implement inventory strategies that insulate against short-term steel shocks.

For investors and M&A teams: Target aftermarket-service providers and regional dealers for consolidation plays—these businesses often deliver stable margins and gateways into end-user accounts.

For procurement teams: Require OEMs to demonstrate certified local compliance and service KPIs, embed material-price pass-through clauses, and demand visibility into lead-time assurance measures.

Our report combines rigorous market-sizing grounded on the 2025 baseline, scenario-based forecasting through 2032, and practical models that map directly to procurement, engineering and capital-allocation decisions. It surfaces tactical moves you can implement in quarters, and strategic options to position for the 2030+ market environment.

To preserve commercial value and confidentiality for subscribers, detailed regional and application splits, model-level pricing matrices, and fully itemized competitive scorecards are provided exclusively in the full report. These gated assets include downloadable dashboards and vendor contract-play templates designed to accelerate decision-making.

Download the executive brief to access the headline forecasts and scenario summaries.

Contact a PW Consulting analyst to arrange a tailored briefing, including vendor scorecards and procurement playbooks for your region or fleet profile.

Subscribe to receive our monthly regulatory and parts-availability watch—essential for firms operating across multiple jurisdictions.

PW Consulting’s Tower Crane Market report is built to translate market complexity into executable strategy. In a market growing at a mid-single-digit CAGR with concentrated market power and accelerating technical differentiation, the right intelligence in 2026 will determine who leads in 2028—and who is left negotiating commoditized bids.

For detailed analysis of this topic, please visit the official page:Tower Crane Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com