PW Consulting: Strategic Brief — LPG Cylinder Market Outlook and Decision Playbook for 2026

As governments, utilities, manufacturers and strategic buyers prepare their plans for 2026, the LPG cylinder market is entering a phase where measured, data-driven actions will sharply differentiate winners from laggards. PW Consulting’s latest LPG Cylinder Market report (base year 2025) distills the near-term trajectory, risk vectors and commercial playbooks that matter for capital allocation, sourcing and product strategy decisions. This release summarizes the report’s strategic value and highlights the tactical guidance executives will need — while reserving the granular segment tables and proprietary scorecards for the full report.

LPG Cylinder Market

Market trajectory at a glance

After steady expansion from 2020 through 2025, the total LPG cylinder market reached an estimated USD 227 million in 2025. Our forecast through 2032 projects a return to stronger expansion, with a 2026–2032 compound annual growth rate (CAGR) of 5.5%, taking the market to a projected ~USD 326 million by 2032. The near term (2026–2028) shows measured momentum as supply chain normalization, regulatory shifts and selective infrastructure investments interplay — producing both opportunities for scale players and entry points for differentiated technology providers.

LPG Cylinder Market

Why this report matters for 2026 decision-making

- Actionable horizon: We align analysis to the 18–36 month decision window most procurement, plant-deployment and M&A teams operate within. The base year (2025) benchmarking plus scenario outputs pinpoint when to accelerate procurement, hedge exposures, or defer investments.

- Risk-to-reward mapping: The report translates macro drivers — raw-material volatility, trade-policy shocks, and regulatory compliance demands — into decision-ready triggers (e.g., when to switch sourcing lanes, when to localize production, when to pursue JV alternatives).

- Practical deliverables: Beyond narrative, the report includes procurement playbooks, supplier scorecards, site-selection checklists, CAPEX sensitivity matrices, and three prioritized value-capture initiatives tailored to OEMs, distributors and large-scale end users.

Drivers shaping 2026 outcomes

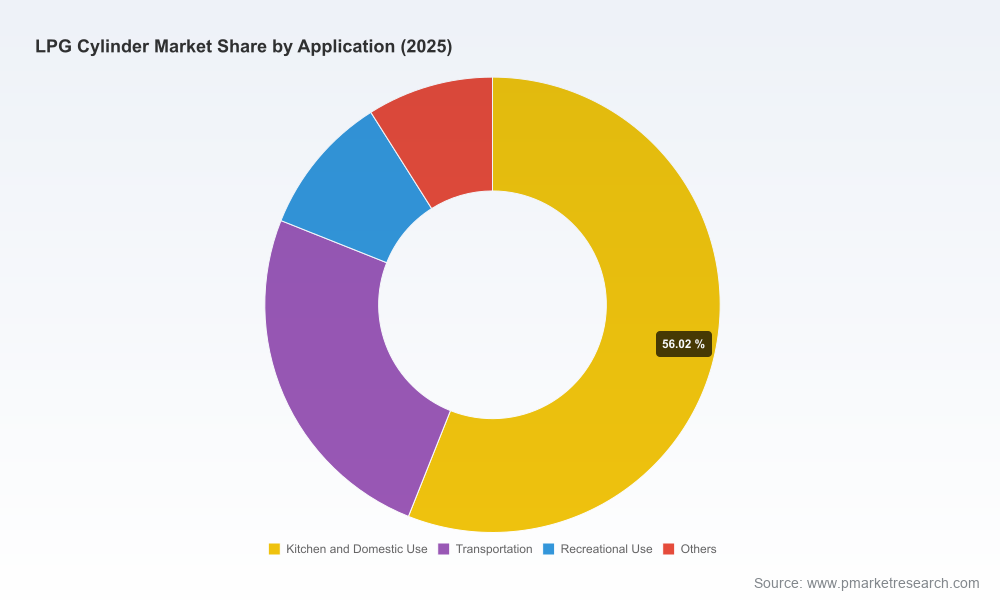

- End-use demand dynamics: Household energy access programs, transport-fleet retrofits and leisure/recreational segment growth are sustaining baseline demand. The compositional shift toward lighter-weight, higher-safety solutions is also accelerating product replacement cycles in select markets.

- Technology and product differentiation: Composite cylinders and modular integrated systems are gaining traction where higher unit economics and differentiated service models (e.g., rental, refilling networks) justify premium pricing. Steel cylinders remain dominant where cost and ruggedness are primary decision criteria.

- Supply-side concentration and competition: Market concentration remains moderate — CR3 ~26.8% and CR5 ~37.9% — indicating a market where global-scale producers coexist with many regional manufacturers. This structure produces localized pricing power in some markets while leaving room for consolidation and strategic partnerships.

- Trade policy and regulatory risk: Recent determinations to continue antidumping and countervailing duties on certain imports have immediate implications for sourcing cost curves and supplier selection. Regulation of steel inputs and certification requirements (ISO/DOT/CE) continue to be decisive factors in cross-border procurement.

Competitive landscape — who matters and why

The competitive field is a mix of high-volume steel producers, specialized composite innovators, and strong regional manufacturers. Key archetypes emerge:

LPG Cylinder Market

- High-volume Chinese manufacturers: Several Chinese producers operate multi-line, high-throughput plants supplying global markets. Their strengths are scale, integrated supply chains and competitive pricing — coupled with increasing export-focused footprints and international certifications. These players are strategically important for buyers prioritizing cost and delivery scale but should be evaluated for trade-policy exposure and long-term supply risk.

- Western and regional steel producers: Established firms in North America, Europe and Asia maintain positions through quality credentials, service networks and downstream integration. They are preferred suppliers where contract terms, product liability frameworks and total cost of ownership (TCO) are primary procurement criteria.

- Composite and technology leaders: Specialist providers of composite cylinders and integrated systems are winning in premium niches — leisure, marine, specialty industrial applications and safety-obsessed procurement channels. Their value proposition is product differentiation, lower weight and rapid urban adoption where regulators and users reward safety and convenience.

Representative names that feature in our competitive analysis include manufacturers with substantial production footprints and export certifications, established regional exporters, and composites specialists whose technology roadmaps are reshaping use-cases. Recent market moves — such as a leading manufacturer launching a facility in South Africa in late 2025 and active trade-policy proceedings involving imports from key producing countries — underscore the geographic and policy vectors executives must account for.

Supply-chain and trade-policy implications

- Tariffs and antidumping actions: The continuation of certain duties affecting steel cylinder imports is more than a tariff story; it alters supplier economics, short-term availability and investment calculus for regional manufacturing. Companies sourcing from jurisdictions subject to orders should model three scenarios (status quo, escalation, revocation) and pre-qualify alternative sources for critical months.

- Raw material exposure: Steel remains the dominant raw input for traditional cylinders. Price volatility and sourcing constraints can quickly erode margin, particularly for commodity-focused manufacturers. Hedging strategies, long-term supply contracts and vertical integration options should be prioritized in procurement planning.

- Localization vs. centralized production: New facilities in targeted regions indicate a trend toward localized capacity to avoid trade friction and to meet on-the-ground service expectations. Our site-selection framework in the report scores locations on labor, logistics, duty exposure and certifiability to inform whether to greenfield, brownfield or partner.

Strategic playbook — recommended actions for 2026

Based on scenario-led analysis, PW Consulting recommends corporate teams calibrate actions across six priority tracks. The full report operationalizes each track with checklists, timelines and estimated ROI windows.

- Sourcing resilience: Establish a dual-sourcing mandate for critical SKUs and fast-track qualification of geographically diverse suppliers. Where antidumping duties are in force, model landed-cost parity and inventory build strategies for a 6–12 month protection horizon.

- Product portfolio optimization: Reassess SKU rationalization to prioritize higher-margin, differentiated cylinders (e.g., composite or value-added assemblies) while standardizing steel offerings to reduce manufacturing complexity.

- Commercial and channel innovation: Move beyond unit sales to service models (rental, subscription, managed refill) in markets with mature distribution. These models reduce customer churn and increase lifetime value.

- Capex and footprint decisions: Use our site-selection and ROI calculator before committing to new plants. In many cases, partnering with established regional producers or contracting toll-manufacturing yields superior capital efficiency versus immediate greenfield build-out.

- M&A and partnerships: Prioritize targets that close distribution gaps, add certified production lines or bring composite capability. Our M&A scorecard ranks targets along strategic fit, integration complexity and near-term synergies.

- Regulatory and compliance readiness: Implement a regulatory-watch program tied to procurement triggers. Certifications (ISO/DOT/CE) and compliance pathways are non-negotiable prerequisites for export and institutional contracts.

What’s inside the full PW Consulting report (high-level)

- Market sizing and forecast models (base year 2025; detailed outputs to 2032) and a scenario engine for regulatory and raw-material shocks.

- Supplier scorecards and a shortlist of strategically relevant manufacturers by archetype, with operational profiles and risk assessments.

- Procurement playbooks: template RFPs, contract clauses for duty contingencies, and service-level KPIs for cylinder-as-a-service models.

- Site-selection and CAPEX-vs-contract manufacturing decision matrices, plus phased investment roadmaps tied to demand breakpoints.

- Three M&A/investment case studies with modeled IRR sensitivities and integration checklists.

- Regulatory watchlist and trade-policy impact scenarios, including the operational implications of sustained antidumping and countervailing measures.

Executive caveat — what we intentionally withhold here

In line with PW Consulting’s “prequel” approach, this communication surfaces strategic conclusions and operational implications while withholding granular segment-by-segment tables, raw dataset downloads, proprietary supplier rankings and specific regional share figures. Those exhibits are integral to executing the playbook and are available in the full report package to qualified subscribers and clients. The reason: these datasets are decision-grade inputs and must be evaluated alongside client-specific constraints (contract maturities, existing inventory, certification status) to produce executable plans.

Final assessment

For executives preparing 2026 budgets and strategic initiatives, the LPG cylinder market offers a mix of steady baseline demand and pockets of higher-growth, higher-margin opportunity — particularly for firms that move beyond commoditized supply and adopt differentiated product-and-service models. Trade-policy continuity and raw-material dynamics create both risks and arbitrage opportunities: those who prepare contingency sourcing strategies, validate alternative supply channels and selectively invest in differentiated product lines will capture disproportionate value.

Next steps

- Download the full PW Consulting LPG Cylinder Market report for the base-year datasets, detailed segment analysis and supplier scorecards (the full dataset enables deployment of the procurement playbook and CAPEX decision tools).

- Schedule a briefing with our sector lead to review bespoke scenarios for your supply footprint, certification gaps and M&A priorities for 2026.

PW Consulting’s LPG Cylinder Market report turns market intelligence into executable steps. For leadership teams preparing for 2026, it provides the calibrated mix of risk assessment, tactical playbooks and investment-grade modelling required to convert uncertainty into advantage.

For detailed analysis of this topic, please visit the official page:LPG Cylinder Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com