LED Display Market 2026: Strategic Preview — PW Consulting Releases Action-Oriented Industry Intelligence

Executive summary

PW Consulting today publishes a strategic companion to its full LED Display Market report, offering senior leaders an executive preview of the forces shaping investment, sourcing, and product strategies in 2026. Built on a base year of 2025 (historical window 2020–2025 and forecast horizon 2026–2032), the study maps an industry moving from recovery-driven expansion into steady, technology-led growth. At the macro level, the market recorded steady growth during the historical period and is forecast to expand at a compound annual growth rate (CAGR) of 5.41% across 2026–2032. PW Consulting’s proprietary model projects the market size rising from USD 179.0 Million in 2025 to approximately USD 257.6 Million by 2032, validating both near-term demand opportunities and long-term structural tailwinds.

LED Display Market

Why this matters for 2026 decision-makers

- Capital allocation and timing: The projected mid-single-digit CAGR signals a market that rewards selective investment rather than indiscriminate scale plays. Companies must target high-return pockets and time capacity investments to avoid margin compression from cyclical supply surges.

- Supply chain resilience: The report quantifies how recent tariff actions and metal-sensitive duty schedules materially change landed costs. Procurement strategies that succeed in 2026 will blend diversified sourcing, proactive hedging, and modular contract terms to preserve margins.

- Product roadmap and technology adoption: Continued adoption of fine-pitch and microLED innovations, coupled with better integration of system-level software, creates differentiation opportunities. Price mix and feature-led roadmaps will determine winners in both commercial and premium residential segments.

- M&A and partnership playbooks: With the market showing a moderate level of concentration (CR3 and CR5 metrics indicate that the top-tier vendors control a substantial but not monopolistic share), 2026 is a window for bolt-on acquisitions and strategic alliances to accelerate capability buildouts.

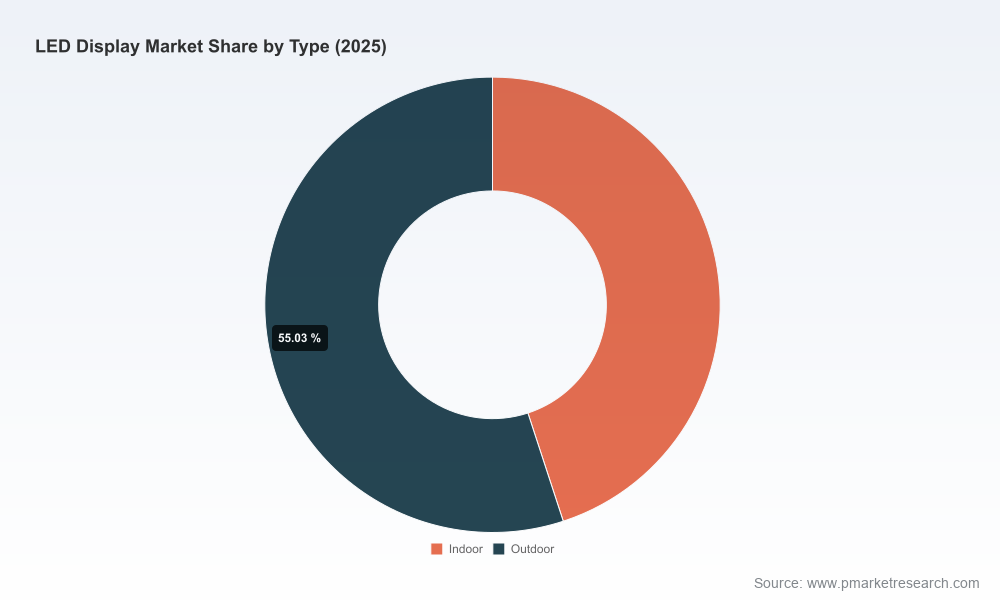

Market trajectory — what the numbers tell us (high level)

PW Consulting’s macro accounting shows a market that expanded steadily through 2020–2025 and continues to grow through the forecast window. The trajectory is characterized by:

LED Display Market

- Measured demand growth across core use cases — advertising, live events, corporate and retail signage, as well as specialized verticals such as broadcast and control-room displays.

- Upgrading cycles driven by higher resolution requirements, lower pixel pitch capabilities, and new form-factors such as MicroLED for premium installations.

- Profitability pressure stemming from component cost volatility and tariff-driven distribution of sourcing footprints.

These aggregate dynamics produce an industry environment where strategic discipline, rather than scale alone, is the most reliable route to sustainable margins.

LED Display Market

Operationally actionable content in the full report

While this release provides strategic direction and tested frameworks, the full PW Consulting LED Display Market report includes practitioner-oriented deliverables designed for immediate use in planning cycles and vendor negotiations. Highlights include:

- A validated forecasting model (scenario-based) that allows CFOs and product planners to stress-test revenue sensitivity to price, mix, and installation-service expansion.

- Go-to-market playbooks tailored to enterprise, retail, and rental/event segments, including channel economics, recommended margin structures, and SaaS-enabled service offerings.

- Vendor selection and RFP templates mapped to technical specifications (pixel pitch, brightness, refresh rates), total cost of ownership (TCO) calculators, and lifecycle replacement schedules.

- A supply-chain risk matrix highlighting input-cost exposure (semiconductors, specialty metals, packaging), lead-time shock simulations, and mitigation measures such as contract clauses and dual-sourcing strategies.

- Regulatory impact assessments with pragmatic compliance checklists that commercial leaders can use to quantify tariff-driven cost impacts and redesign sourcing strategies accordingly.

- Playbooks for M&A diligence and integration, including target-screening criteria, synergy estimation templates, and cultural-integration checkpoints specific to display hardware and software businesses.

To preserve the report’s proprietary value for subscribers and to honor competitive sensitivities, detailed segment-level tables, regional and application breakouts, and company-level financials are available in the paid report.

Competitive landscape — who matters and why

The LED display industry is shaped by a mix of legacy manufacturers, electronics conglomerates, and specialized display houses. Market concentration metrics show a moderate concentration: the top three players account for a meaningful share of industry revenues, and the top five further consolidate market power, but the landscape still leaves openings for innovative entrants and regional champions.

- Cree LED (Basingstoke, UK): Known for high-intensity LEDs and RGB platforms, Cree’s product expansions into ultra-compact packages with extended color gamuts strengthen their position in high-brightness and outdoor signage markets. Their recent XE-B family demonstrates a push toward higher-density, color-rich luminaires that are appealing for premium outdoor applications and specialty signage.

- Neoti (Bluffton, Indiana, USA): Specializes in direct-view LED (dvLED) panels and video wall systems tailored to broadcast, control rooms, and mission-critical environments. Their focus on reliability and fine-tuned calibration positions them well where uptime and color fidelity are non-negotiable.

- Daktronics (Brookings, South Dakota, USA): Remains a leader in large-format displays, scoreboards, and stadium signage. Daktronics’ integration of AV systems and managed services continues to be a differentiator for venue owners seeking turnkey solutions and long-term service contracts.

- LG Electronics & Samsung Electronics (Seoul/Suwon, South Korea): The large electronics OEMs compete at the premium end with microLED and ultra HD solutions, leveraging global distribution, brand power, and integration capabilities. Product launches in 2026 from both companies underscore an escalation in premium, plug-and-play offerings aimed at retail, corporate, and luxury residential deployments.

- Leyard, Unilumin, Absen (China): These firms continue to push fine-pitch indoor solutions and rental/event systems, benefitting from manufacturing scale and rapid product iteration cycles. Their combined product portfolios span entry-level to high-resolution indoor and outdoor applications, and they play a central role in price-point competition.

Recent product introductions and certifications signal shifts in competitive advantage: component-level innovation (smaller LED packages and extended color capabilities), systems-level reliability enhancements, and third-party recognition are all accelerating buyer expectations. Leaders will need to harmonize product excellence with service models to defend share.

Regulatory and geopolitical dynamics to factor into 2026 planning

- Tariff and trade policy volatility: Recent U.S. proclamations have raised effective tariff rates and introduced reciprocal trade measures across a range of imports. These elevated duties materially alter landed cost calculations and shift the calculus for localization versus global sourcing.

- Section 232 and metal-sensitive tariffs: Modifications to tariffs on steel and aluminum through 2027 increase capital-equipment and enclosure costs for outdoor and structural installations, thereby inflating installation TCO in specific use cases.

- Broader tariff pressure: Higher average effective tariff rates across core consumer and industrial goods require CFOs to re-evaluate supplier contracts and to model region-specific procurement scenarios in capital planning.

PW Consulting’s full report models these policy scenarios quantitatively and provides play-by-play mitigation strategies — from negotiated trade clauses to regional assembly hubs — enabling procurement and strategy teams to build robust, compliant plans.

Key strategic actions for 2026

- Embed scenario-based forecasting into annual planning cycles and link CAPEX approvals to upside/downside case triggers.

- Prioritize modular product families that can be localized or reconfigured to mitigate tariff exposure while preserving gross margins.

- Shift part of the procurement mix toward value-added services (installation, warranty, calibration) to increase recurring revenue and reduce reliance on component-margin alone.

- Pursue selective partnerships or bolt-on M&A that add software integration or vertical-market expertise rather than broad horizontal scale.

- Accelerate testing and early deployments of premium microLED solutions where higher ASPs and differentiated user experience justify investment.

How to access the full intelligence

This release is an executive preview designed to guide strategic dialogue. The full PW Consulting LED Display Market report contains the granular tables, regional and application breakouts, vendor financial profiles, and downloadable models that boards, strategy teams, and investors need to execute on the opportunities and guard against the risks outlined above. Detailed segment data and model inputs are intentionally reserved for report subscribers. To obtain the full report and interactive forecasting workbook, please visit PW Consulting’s report page listed in our newsroom.

PW Consulting remains available to brief executive teams, support scenario workshops, and provide custom deep-dive modules for procurement, product, and M&A due diligence needs. In an industry where product innovation and policy shifts move quickly, disciplined, data-driven strategy will separate winners from followers in 2026 and beyond.

For detailed analysis of this topic, please visit the official page:LED Display Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com