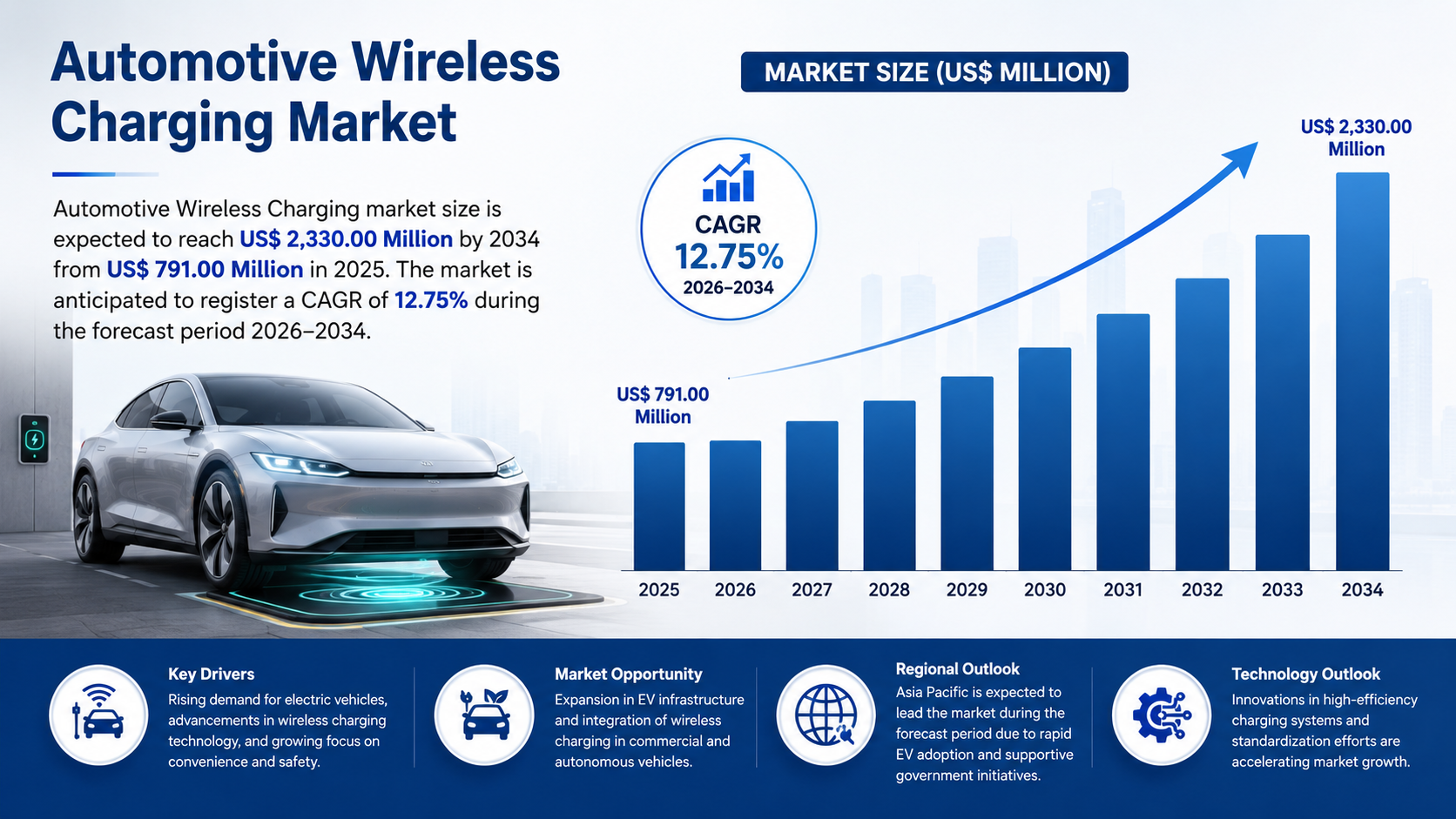

Infertility Testing and Treatment Market to Reach US$ 3.22 Billion

Other |

2026-02-17 12:24:07

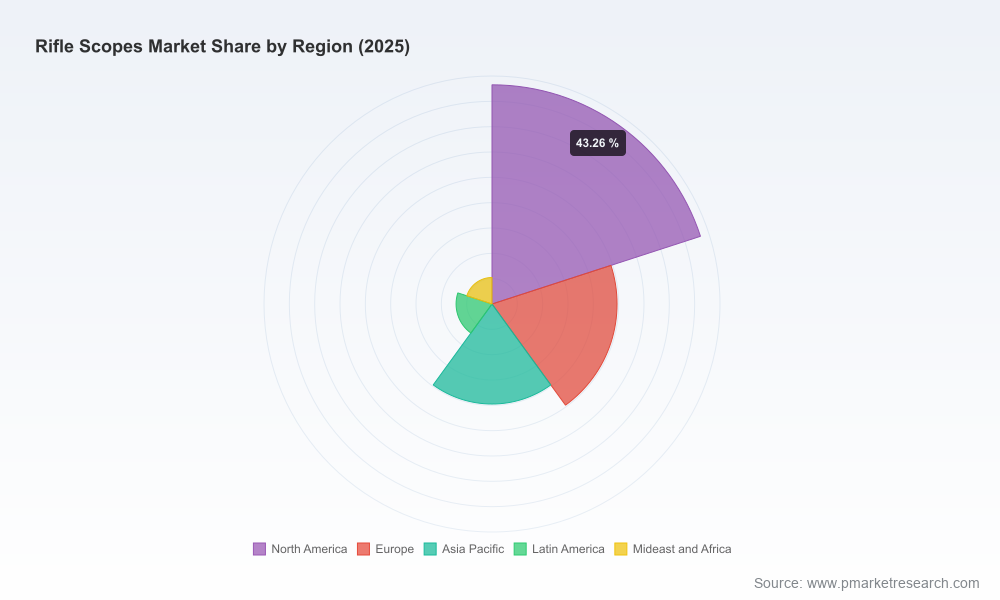

PW Consulting’s latest Rifle Scopes Market report (base year 2025) delivers a focused, decision-grade intelligence package for executives planning product, commercial, and capital strategies in 2026. Drawing on a systematic historical analysis (2020–2025) and a forward-looking forecast window (2026–2032), the study projects the market growing at a compound annual growth rate (CAGR) of 5.2% (USD, revenue unit: Million). The global market is estimated at USD 215.0 Million in 2025, progressing to an anticipated USD 226.9 Million in 2026 and reaching roughly USD 344.8 Million by 2032 — a trajectory that implies predictable expansion alongside shifting product and channel dynamics.

Rifle Scopes Market

Prioritization under uncertainty — the report translates macro growth into calibrated choices for portfolio investment, capacity allocation, and pricing strategy that are robust to near-term volatility.

Rifle Scopes Market

Actionable go-to-market playbooks — tailored recommendations for premium vs. value-tier positioning, channel mix (distributor, OEM, retail, direct-to-consumer), and aftermarket monetization to improve top-line capture.

Rifle Scopes Market

M&A and partnership signals — an evidence-based framework to identify consolidation opportunities, bolt-on niches, and strategic alliances that accelerate access to optics, thermal imaging, and digital targeting technologies.

Supply chain resilience planning — operational prescriptions to mitigate raw-material, optics-glass, and electronics sourcing risks that typically surface during product ramp-up phases.

Market sizing and demand modeling (historical series and forward projections across 2026–2032), including scenario variants calibrated to macroeconomic sensitivity and defense procurement cycles.

Competitive benchmarking and capability maps that compare product portfolios, technology stacks, and channel footprints — enabling side-by-side evaluation for product rationalization and feature prioritization.

Pricing and margin analytics, with cost-to-serve buckets by channel and margin leakage diagnostics suited for 2026 fiscal planning.

Technology and product roadmaps — assessment of optics, electronic reticles, thermal imaging, and ballistic integration paths, with R&D prioritization matrices for fastest time-to-value.

Commercial playbooks for key demand segments (recreational hunting, shooting sports, and defense/tactical applications) that translate buyer behavior into SKU rationalization and marketing spend allocation.

Supply-chain action plans covering dual-sourcing, inventory buffers, and nearshoring scenarios to secure critical components and sustain product launch timelines.

M&A screening tools and valuation comparables, integrated with post-deal integration checklists to accelerate synergies in procurement, distribution, and engineering.

Regulatory and export compliance checklists relevant to cross-border sales of advanced electro-optics and thermal devices.

Premiumization remains a profitable axis. With steady CAGR and rising buyer willingness to pay for proven optical clarity and ruggedization, premium product lines continue to outperform on margin, but require demonstrable feature differentiation (glass, coatings, reticle tech, warranty).

Thermal and integrated digital features are accelerating adoption in both hunting and tactical segments. Expect technology-driven product tiers to compress lifecycles and demand higher R&D-to-revenue ratios.

Channel bifurcation — while traditional retail and OEM channels remain core, direct-to-consumer (D2C) and digital demonstration tools (AR-enabled product trials, ballistic calculators integrated into product pages) are becoming decisive for conversion and margin recovery.

Supply-chain pressure points center on specialty glass, precision manufacturing capacity, and sensor electronics. Firms that lock visibility and contractual priority on critical inputs will secure launch windows and protect margin.

Defense procurement cycles create episodic demand uplifts; companies with validated defense capabilities and compliance readiness can convert short-term funnel spikes into long-term platform relationships.

Service and aftermarket present meaningful recurring revenue opportunities — extended warranties, recalibration services, and accessory ecosystems can increase lifetime value and dampen new-product acquisition pressures.

Mid-market competition intensifies from manufacturers offering feature-rich optics at aggressive price points. Incumbents must choose between margin defense via innovation and scale plays via distribution and cost optimization.

The industry shows moderate concentration (CR3 ≈ 52%, CR5 ≈ 68%), indicating substantial market share held by a few global incumbents while leaving space for challengers and niche specialists. Our competitive analysis synthesizes strategic intent across premium optics manufacturers, mass-market brands, and specialized thermal/electro-optics suppliers:

Nightforce Optics (Orofino, Idaho) — doubling down on tactical performance and durability. Recent launch activity underscores a shift to modular tactical platforms; peers should anticipate higher engineering thresholds for tactical claims.

Schmidt & Bender (Germany) — continues to trade on heritage, precision engineering, and military pedigree. Their strategy pressures others to defend advanced manufacturing and service quality credentials.

Vortex Optics (Colorado) — broad portfolio reach and channel depth; their mix of consumer and higher-end offerings makes them a formidable scale competitor in price-sensitive segments.

Burris Optics (South Carolina) — product redesigns focused on optical improvements and ergonomics reflect a play for share among performance-minded hunting customers.

Leupold & Stevens (Oregon) — sustained emphasis on reliability and field-proven performance positions them well with traditional hunting markets and specialist OEMs.

Trijicon (Michigan) — expanding hunting-oriented configurations while maintaining tactical credentials; new product extensions indicate a balanced dual-market strategy.

Sig Sauer Electro Optics, Steiner, Athlon, Primary Arms, Pulsar Vision, Holosun, Aimpoint, Hensoldt, Swampfox — these firms represent a mix of specialized thermal/night vision providers, red-dot innovators, and value-driven optics brands. Their activities signal continued segmentation by technology and channel, creating both collaboration and competitive risks for incumbents.

Notable product moves in early 2026 — such as the introduction of Nightforce’s NX6 family, Trijicon’s Credo HX line extensions, Burris’s Veracity redesign, and March Scopes’ 2026 tracking scope release at IWA — illustrate an industry accelerating refresh cycles and product differentiation around optics quality, reticle functionality, and tracking/targeting capabilities.

Moderate concentration paired with technological specialization increases the strategic value of targeted M&A to secure capability gaps (thermal sensors, digital reticles, manufacturing capacity).

Firms without distinctive IP or scale advantages will face margin pressure unless they create defensible niches (e.g., rapid service support, unique thermal algorithms, or platform-certified integrations with ballistic solutions).

Partnerships between optics manufacturers and electronics/sensor firms will become more common — winning plays will combine optics excellence with software-enabled features.

0–3 months: Rebase product-roadmap priorities using the report’s scenario outputs; accelerate critical component dual-sourcing and validate pricing floors to sustain margins through 2026 seasonality.

3–12 months: Launch pilot SKUs that bundle optical upgrades with software-enabled features; test D2C channels and AR product demos in priority markets to measure conversion lift and margin improvement.

12–36 months: Pursue targeted acquisitions or partnerships to close gaps in thermal imaging, digital reticles, or sensor fusion; embed aftermarket and service offerings to increase lifetime customer value.

For executives preparing budgets, product roadmaps, or M&A pipelines in 2026, this report is designed to convert market momentum into executable plans. It balances high-confidence market level projections (historical 2020–2025; base year 2025; forecast 2026–2032), competitor intelligence, and practical operating checklists that reduce execution risk. To review the full segment-level modeling, granular regional and application analytics, and the dataset that underpins our scenarios, please consult the full report on PW Consulting’s release page — the detailed tables and downloadable models are intentionally housed there to support confidential strategic workflows.

For detailed analysis of this topic, please visit the official page:Rifle Scopes Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com