Engineering Lab-as-a-Service Market Overview: Key Drivers and Challenges

Other |

2026-04-28 08:54:31

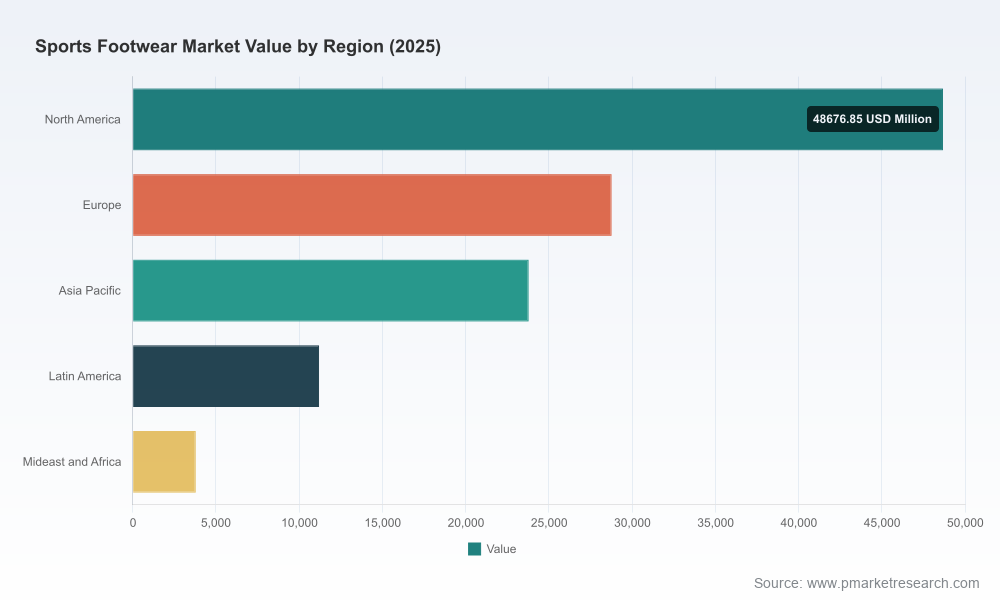

PW Consulting today releases an executive preview of our forthcoming Sports Footwear Market report, designed to inform boardroom decisions and operational plans for 2026. Built on a 2020–2025 historical base and a 2026–2032 forecast horizon, this analysis synthesizes macro demand trajectories, competitive positioning, regulatory shifts, and supply-side stress tests. At the highest level, the global sports footwear market reached approximately USD 116.2 billion in 2025 and is modeled to expand at a compound annual growth rate (CAGR) of 5.76% through 2032, when the market is expected to approach USD 171.1 billion. This release highlights the strategic value of the full report for executives who must translate trend signals into executable choices in 2026.

Sports Footwear Market

Companies entering their 2026 budgeting and product-planning cycles face simultaneous pressures: accelerating sustainability rules, volatile input costs, shifting distribution economics, and intensified competition from both global incumbents and nimble challengers. The full PW Consulting report goes beyond forecasting: it translates market trajectories into decision-grade tools—demand scenarios, margin stress tests, SKU portfolio optimization engines, and a supplier-risk heatmap—enabling leaders to prioritize investments with line-of-sight to profitability and compliance.

Sports Footwear Market

Structural growth with selective acceleration: Consumer demand for performance, wellness, and lifestyle footwear continues to expand, underpinned by broader athleisure adoption and renewed event-driven spikes in sport participation. Our baseline models show steady expansion, with pockets of faster growth tied to technology-led product launches and brand revitalization initiatives.

Sports Footwear Market

Input-cost volatility: Raw material prices remain a critical margin lever. Notably, natural rubber — a key raw material — has proven highly sensitive to weather and pest events, with intra-year price swings exceeding 40% in extreme cases. Manufacturers and procurement teams must embed scenario-driven hedging and alternative-material pathways into 2026 sourcing plans.

Regulatory tightening and circularity mandates: Regulatory timelines are compressing. The EU’s Ecodesign for Sustainable Products Regulation (ESPR) introduces firm obligations — including a prohibition on destruction of unsold textiles and footwear effective July 19, 2026 — that will affect overproduction practices and inventory strategies. Parallel developments include China’s GB 25038‑2024 footwear safety requirements (effective June 1, 2025) and updated European technical standards (EN ISO 20345:2022) coming into force in 2026. These are non-negotiable constraints that must be reflected in next-year compliance and product roadmaps.

Channel and margin dislocation: Direct-to-consumer (DTC) strength and marketplace proliferation continue to alter margin pools. Retail incumbents and digital-native brands are reallocating marketing and distribution investment toward customer lifetime value metrics, while traditional wholesale partners revise contractual terms to protect margins against returns and unsold inventory mandates.

The sports footwear market retains a moderate concentration level: the top three firms control roughly half of global market share, and the top five account for about 55%. This structure creates a dynamic where scale advantages (brand equity, global distribution, R&D budgets) coexist with opportunities for differentiation by focused players.

Nike and Adidas continue to leverage brand ecosystems and product innovation pipelines, balancing performance technology with lifestyle collaborations to defend share and pricing power.

Performance specialists such as ASICS and New Balance are reasserting relevance through focused R&D and product refreshes—an important signal that technical credibility can reaccelerate growth even in a concentrated market.

Premium and niche brands (for example, On and Hoka under Deckers) are converting design distinctiveness into durable premiums, further fragmenting the medium- to high‑end segments and pressuring incumbents to respond with sharper product segmentation.

Value and comfort-focused players—Skechers, alongside broader apparel conglomerates—compete on cost-efficient innovation, channel mix, andscale in non-premium categories.

Recent market moves underscore this mix of incumbency and momentum: Brooks expanded runner-focused assortments in early 2026, On continues brand acceleration with breakout athletic offerings, Asics is experiencing a measurable resurgence alongside New Balance, which has refreshed its running and training lines. These developments validate our thesis that brand investment and product cadence materially shift demand vectors within single seasons.

The PW Consulting report is structured for immediate operational use. Highlights include:

Scenario-based revenue and margin forecasts with sensitivity bands that reflect raw-material shocks and regulatory cost passthroughs;

SKU profitability matrices and SKU rationalization templates to reduce inventory risk while protecting sell-through and brand equity;

Supplier and country-risk heatmaps tied to sourcing cost and compliance exposure (including ESPR and GB/EN ISO testing nodes);

Go-to-market playbooks for DTC, wholesale, and marketplace channels, with margin and inventory rules of thumb for 2026;

M&A and partnership screening criteria designed to identify high-leverage tuck-in targets and capability plays (e.g., materials tech, last‑mile fulfillment, digital fit solutions);

An executive 90‑day activation plan that prioritizes quick wins around procurement contracts, promotional cadence, and compliance gap remediation.

1. Institutionalize supply‑side resilience: Move beyond single-scenario S&OP. Implement rolling, multi-scenario procurement plans that combine selective hedging, alternative-material qualification, and near-shore capacity options to reduce exposure to raw-material shocks.

2. Convert regulatory compliance into competitive advantage: Treat ESPR and new safety standards as a driver for product differentiation—labeling, take-back programs, and verified circular claims can unlock premium positioning while mitigating inventory destruction risks.

3. Recalibrate assortment for margin efficiency: Use SKU profitability and sell-through analytics to cut low-margin SKUs, reallocate working capital to high-conversion designs, and align promotional cadence to lifecycle signals.

4. Accelerate consumer‑facing innovation where it drives margin: Prioritize investments in cushioning, lightweight materials, and digitally-enabled fitting technologies that demonstrably increase ASP and loyalty rather than incremental aesthetic changes alone.

5. Pursue selective inorganic and partnership plays: Identify targets that fill capability gaps—materials science, digital sizing, regional logistic hubs—and structure deals to preserve margin contribution while scaling go-to-market rapidly.

Boards and operating teams should integrate the report’s outputs into three planning layers for 2026:

Strategic (C-suite): Update three‑year portfolio and M&A hypotheses with forecast scenarios and concentration metrics. Reprioritize R&D and capital allocation where return on innovation is highest.

Financial (CFO / FP&A): Stress-test budgets with the report’s margin shock models, and embed new compliance cost lines (ESPR testing, extended producer responsibility) into P&L forecasts.

Operational (COO / Head of Product): Implement SKU rationalization and supplier contingency playbooks, and begin pilot circularity programs to meet mid‑2026 regulatory milestones.

This strategic brief is a guided preview. The full PW Consulting Sports Footwear Market report includes detailed datasets, granular scenario outputs, proprietary supplier-risk scoring, and templated playbooks designed for rapid executive execution. To obtain the complete report, interactive dashboards, and consulting engagement options, visit our reports hub or contact your PW Consulting account representative.

PW Consulting remains available to support rapid integration of these insights into your 2026 planning cycle—from one‑day executive briefings to hands‑on implementation sprints tailored to procurement, product, or channel transformations.

For detailed analysis of this topic, please visit the official page:Sports Footwear Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com