Medical Device Tray Market Size, Share, and Growth Opportunities

Party |

2026-06-04 07:56:12

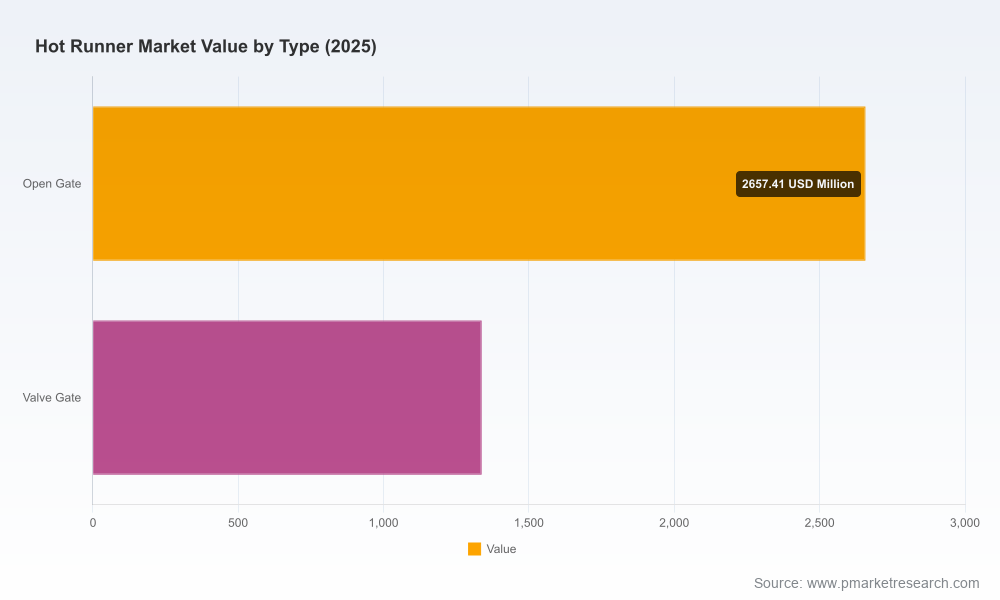

PW Consulting’s latest Hot Runner Market report (base year 2025, historical coverage 2020–2025, forecast 2026–2032) equips executives and investors with the strategic intelligence they need to make high-impact decisions in 2026. The global market, which expanded steadily through the first half of the decade, reached approximately USD 3.995 billion in 2025 and is modeled to grow at a compound annual growth rate (CAGR) of 7.2% across the 2026–2032 forecast window—reaching an estimated USD 6.505 billion by 2032. These headline dynamics frame a near-term opportunity set shaped by automation, energy-efficiency innovation, and shifting trade and input-cost pressures.

Hot Runner Market

Timing: 2026 will be the inflection year in which several industry forces converge—rising automation adoption, stricter regulatory demands for medical and automotive components, and renewed investment in energy-saving hot runner technologies. Our report translates these convergence effects into actionable scenarios for procurement, operations and M&A planning.

Hot Runner Market

Clarity on growth trajectory: With a 7.2% CAGR through 2032, budget holders can use our topline forecasts to stress-test three- to five-year capital allocation plans without overcommitting to narrow sub-segments—PW Consulting’s modelling shows robust aggregate expansion even under conservative assumptions.

Hot Runner Market

Competitive posture: The market exhibits a relatively high concentration among leading providers (CR3 ~65%, CR5 ~78%). That structure amplifies the commercial impact of supplier selection, alliance formation and aftermarket-service strategies. Our analysis shows where scale matters, and where niche technical capabilities deliver disproportionate margin upside.

Energy intensity and efficiency become a procurement battleground. Proven heater innovations can cut energy consumption meaningfully—benchmarks in the market indicate device-level improvements that translate directly into lower cycle costs and reduced carbon footprint; energy-savings claims should be verified through lifecycle and in-situ measurements before procurement commitments.

Automation and labour dynamics. Labor shortages and rising labor costs are accelerating adoption of hot runner systems that reduce manual intervention. Buyers must balance unit cost with total cost of ownership (TCO), including setup time, maintenance cadence, and spare-parts logistics.

Supply-chain and input-cost volatility. Fluctuations in petrochemical feedstocks and anticipated tariffs on steel and aluminum elevate supplier risk. Our scenario analysis models tariff shock impacts and raw-material price volatility across a range of sourcing strategies.

Regulatory and quality compliance. Medical and automotive segments increasingly require alignment with ISO and other industry-specific safety standards. Compliance upstream (component sourcing) and downstream (process validation) is now a prerequisite for participation in high-growth segments.

Re-evaluate CapEx frameworks: Move from a purely unit-cost procurement metric to a TCO model that includes energy, downtime, spare-parts lead times and tooling lifecycle. Our report provides a tailored CapEx calculator to model five procurement scenarios.

Prioritize modularity and serviceability: Systems that enable rapid nozzle swaps, remote diagnostics and incremental upgrades reduce downtime risk and protect margins. Contract language should capture service-level metrics and parts-availability clauses.

Build hedged supply strategies: Combine long-term agreements with geographically diversified suppliers and selective local sourcing to mitigate tariff and shipping shocks. We outline hedging levers and decision trees aligned to different risk appetites.

Invest in energy intelligence: Commission in-line energy audits and require supplier-provided energy benchmarking. Technologies that demonstrate substantiated reductions in heating energy—when validated—are prime candidates for pilot programs that can be scaled rapidly.

Scan for consolidation targets: Given the market’s concentration profile, 2026 offers opportunities for bolt-on acquisitions that expand footprint, aftermarket capability, or technical IP. We map valuation corridors and integration risk profiles for strategic buyers.

The market is populated by a mix of global system houses, regional specialists and component-focused suppliers. Leading players combine product innovation with service networks that support sophisticated production environments. Below we summarize the strategic postures of core vendors evaluated in the report—these profiles are designed to inform supplier-selection and partner-screening processes.

Oerlikon HRSflow — Known for advanced nozzle and gate technologies, the company has emphasized STARgate and Glow HRS innovations and demonstrated investment in manufacturing capacity at recent industry shows. Their roadmap focuses on precision molding for high-value segments.

Husky Injection Molding Systems — Husky couples hot runner platforms with controllers and broad energy-efficiency messaging. Recent trade show activity in Asia confirms a push to support medical and precision molding opportunities with localized engagement.

GÜNTHER Hot Runner Technology — The vendor markets energy-saving heaters and connectivity-enabled systems. Demonstrated heater-level savings are a compelling commercial narrative for buyers who must justify energy-related capital investments.

Synventive Molding Solutions — Positions itself with gate control technologies and a focus on automotive and lighting applications; product differentiation centers on precision gating and integrated controller solutions.

Mold-Masters — Emphasizes standardized, cost-oriented platforms for commodity applications; a sensible option where throughput and predictable economics outweigh customization needs.

Polyshot, INCOE, DME — These organizations deliver a range of customized systems, strong North American service footprints, and comprehensive mold-component ecosystems—suited for buyers that need rapid localized support and engineering partnership.

Market activity through 2025–2026—trade-show unveilings, distributor appointments and widened product portfolios—signals that vendors are competing on both product performance and go-to-market scale. Examples of recent activity include regional exhibitions by multiple suppliers and strategic distributor partnerships that broaden North American reach. PW Consulting’s vendor scorecards capture these dynamics, benchmarking R&D momentum, aftermarket capability and channel strategy.

Topline market sizing and growth drivers (historical 2020–2025; forecast 2026–2032) with scenario analysis and sensitivity testing to raw-material and tariff shocks.

Technology roadmaps and energy-efficiency benchmarking—including device-level and system-level TCO models—to prioritize pilot investments.

Vendor benchmarking and competitive scorecards with capabilities matrices, go-to-market assessment and integration risk profiles for acquisition targets.

Buyer’s playbook: procurement templates, SLA clauses, and a step-by-step validation protocol for supplier energy claims and performance guarantees.

Operational toolkits: CapEx calculator, spare-parts optimization model, and a regulatory-compliance checklist for medical and automotive applications.

Strategic scenarios: three distinct market paths and recommended actions tailored for OEMs, tier-1 injection molders, and contract manufacturers.

Our analysis synthesizes a bottom-up revenue model, supplier financial disclosures, primary interviews with buyers and vendors, and trade-show intelligence collected through 2025 and into mid-2026. The report’s base-year calibration uses audited industry datapoints and reconciles market shares to generate high-confidence forecasts. Where granular segment-level data materially affects commercial strategy, PW Consulting surfaces directional guidance in the executive summary while preserving detailed sub-segment tables for report subscribers.

For senior leaders preparing 2026 plans, the report functions as a decision accelerant: it converts macro growth expectations into investment priorities, supplier strategies and risk-mitigation playbooks. Executives using the PW Consulting framework can reduce procurement cycle time, defend margin against energy and tariff shocks, and identify focused M&A targets that fill capability gaps.

PW Consulting’s Hot Runner Market report is designed as a working tool for procurement, operations, and corporate strategy teams. To access the complete segment-level tables, vendor models and downloadable decision-support tools, please refer to the full report on our website. The public summary above highlights strategic conclusions and practical levers; the full subscription includes the detailed inputs required for transactional decision-making.

For detailed analysis of this topic, please visit the official page:Hot Runner Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com