How Telemedicine Collaboration Is Expanding the At‑Home Drug of Abuse Testing Market

Health |

2026-05-11 10:13:28

PW Consulting’s latest industry brief on the Aluminum Composite Panels (ACP) market delivers a forward-looking synthesis crafted for boardrooms, strategy teams, procurement leaders and product innovators preparing plans for 2026 and beyond. Built on a base year of 2025 and a consolidated historical dataset (2020–2025), our forecast model projects the global ACP market to expand from an estimated USD 5.83 Billion in 2025 to approximately USD 8.81 Billion by 2032, driven by a compounded annual growth rate (CAGR) of 6.16% across the 2026–2032 horizon. This preview outlines where the most consequential strategic inflection points sit — while reserving the granular sub-segment tables and regional splits for the full report to preserve the commercial value of that intelligence.

Aluminum Composite Panels Market

2026 is a year of consolidation for ACP market strategy. Companies that move beyond product-centric playbooks to integrate raw-material risk management, regulatory certification roadmaps, and targeted end-market go-to-market strategies will gain outsized share. Our analysis equips executives to:

Aluminum Composite Panels Market

The ACP market’s historical trajectory shows steady expansion from the market entry point in 2020 through 2025, with accelerating adoption in façade, signage and specialty transport segments. Our baseline model anticipates a resumption of mid-single-digit growth beginning in 2026, consistent with a 6.16% CAGR through 2032. For strategy teams this means predictable demand growth large enough to justify targeted capital expenditures — but not so rapid as to eliminate the need for careful capacity planning and product differentiation.

Aluminum Composite Panels Market

Two practical implications flow from this trajectory. First, firms should prioritize investments that improve margin resilience (material substitution, higher-value specialty cores, and differentiated finishing) rather than chasing broad commodity volume. Second, scenario planning should incorporate regulatory-driven step-changes that materially alter product mixes (for example, new fire-safety codes or expanded CE/North American code approvals).

Three dynamics dominate the 2026 decision landscape:

The ACP market shows moderate concentration: the top three players account for a meaningful minority of market value, and the top five extend that reach further — indicating a market that rewards both scale and differentiation. Consolidation is selective; buyers continue to prize validated performance and regional service capabilities.

Key strategic profiles from our competitive analysis:

Notable recent industry moves that validate our strategic theses include the introduction of an A2 Fire Retardant Core production facility (2025), ultra-lightweight ACP launches aimed at transport OEMs (2025), expanded certification of specialty systems (2026), and multiple launches of fire-resistant and durability-enhanced ACP sheets. These milestones accelerate product adoption cycles and raise the technical bar for market entry.

The full PW Consulting report is intentionally pragmatic. It combines a transparent, auditable market-sizing model with a series of executable tools and strategic diagnostics:

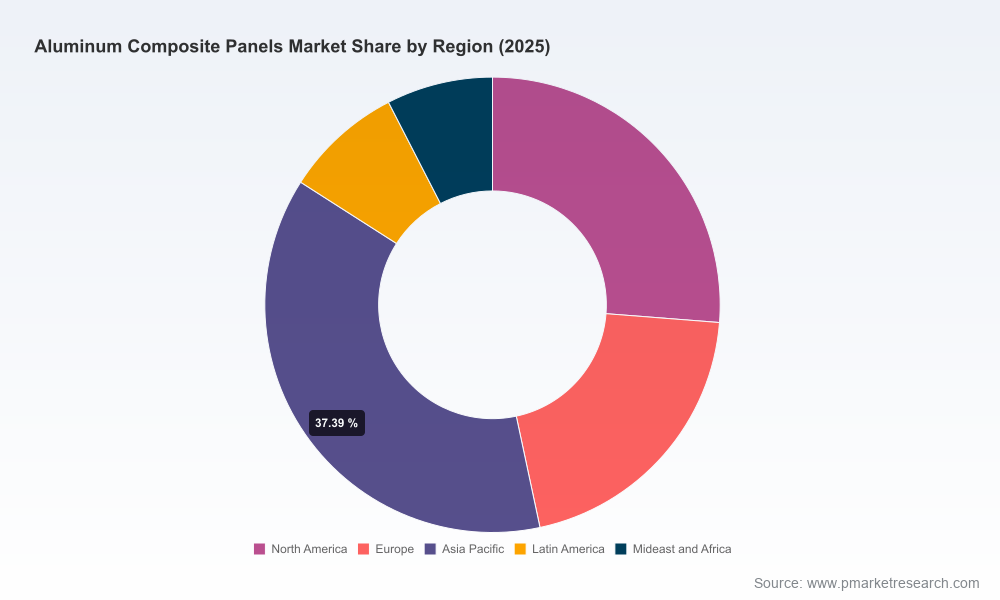

To preserve the commercial utility of the report’s segmentation intelligence, this preview intentionally omits the granular regional, type and application-level splits. The full dataset — including supplier-level shares and regional demand profiles — is available through PW Consulting’s client portal and subscription channels.

For management teams building 2026 plans, we recommend a three‑pronged approach:

Additionally, procurement and corporate development teams should use the next 12 months to build optionality: vendor scorecards reflecting certification status, small strategic equity stakes in upstream recycled-aluminum suppliers, and pilot partnerships with façade design houses to accelerate specification adoption.

This preview demonstrates the strategic depth of PW Consulting’s ACP market work: robust market sizing, a clear line of sight into the drivers of 2026 demand and a set of practical tools to convert insight into action. We deliberately withhold detailed sub‑segment tables and supplier share cards here — those elements form the core commercial value of the full report and are made available to subscribers and clients.

For executive teams planning capital allocation, certification roadmaps, supplier consolidation or M&A activity in 2026, the full PW Consulting report provides the auditable models, playbooks and supplier intelligence to de‑risk those decisions and capture upside. Visit our publication page to access the complete report, interactive models and client briefing options.

For detailed analysis of this topic, please visit the official page:Aluminum Composite Panels Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com