PW Consulting Releases Strategic Preview: Navigating the TPMS Market Through 2026 and Beyond

Executive summary

As vehicle design and fleet management converge with connectivity and sustainability imperatives, Tire Pressure Monitoring Systems (TPMS) have moved from regulatory compliance items to strategic enablers of safety, efficiency and data-driven services. PW Consulting’s new market study — anchored on a 2025 base year and spanning historical analysis (2020–2025) with a forward-looking horizon to 2032 — provides a decision-ready playbook for senior executives planning investments, partnerships and product roadmaps in 2026.

Tire Pressure Monitoring System (TPMS) Market

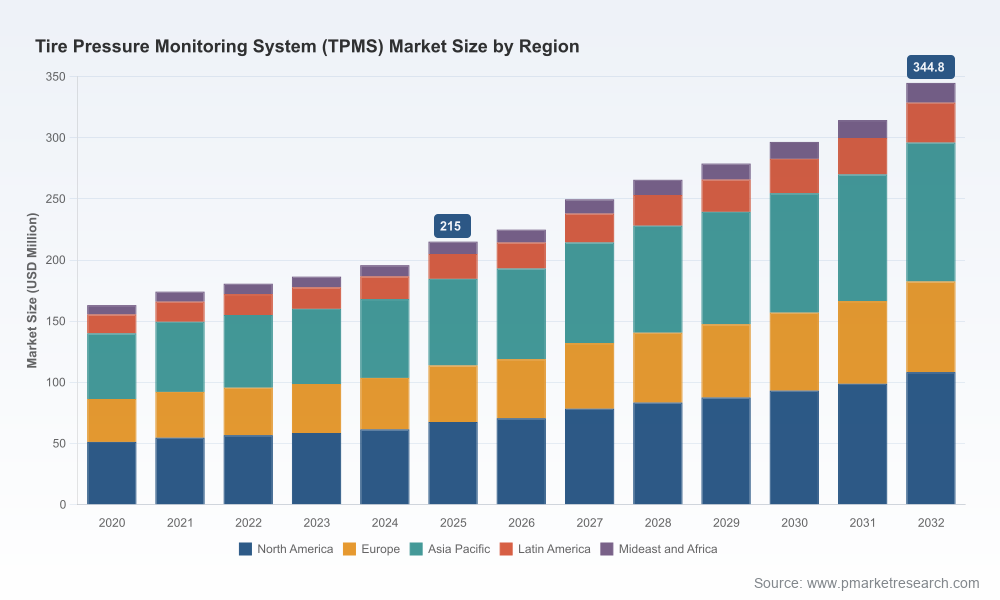

Our headline finding: the global TPMS market is transitioning from a hardware-dominated segment into a hybrid ecosystem of sensors, edge microcontrollers, wireless services and cloud analytics. After growing steadily from 2020 to 2025, the market is forecast to expand at a compound annual growth rate (CAGR) of 8.59% during the 2026–2032 forecast window, reflecting broad adoption across OEM, aftermarket and emerging telematics applications.

Tire Pressure Monitoring System (TPMS) Market

Market trajectory: what the numbers tell us

PW Consulting’s topline series documents a clear growth arc: the TPMS market advanced meaningfully during 2020–2025 and reached a notable inflection point in our base year, reflecting accelerated OEM fitment, regulatory reinforcement and an uptick in retrofit activity. Our model projects continued momentum throughout the 2026–2032 forecast period, driven by higher value-add (sensor + connectivity + analytics) offerings and rising fleet telematics integration.

Tire Pressure Monitoring System (TPMS) Market

- Historical baseline (2020–2025) provided the calibration to identify structural drivers and short-cycle demand shocks.

- Base year 2025 is the anchoring year for scenario and sensitivity testing in the forecast (2026–2032).

- Projected CAGR of 8.59% (2026–2032) signals a market where software-enabled differentiation and aftermarket service models unlock incremental revenue beyond hardware sales.

Why this matters for 2026 strategic decisions

Executives preparing capital plans, product roadmaps or M&A strategies in 2026 will find three practical implications:

- From component to system revenue: Margins will increasingly accrue to players who combine sensors with data platforms, predictive maintenance services and fleet-level dashboards. Pure-play hardware suppliers must decide whether to vertically integrate or partner for software capabilities.

- Regulation remains a floor, not a ceiling: Mandatory fitment rules established in major markets deliver a baseline market, but competitive differentiation comes from energy efficiency, sensor lifetime, recyclability and connectivity options (BLE, proprietary RF, integrated telematics).

- Fleet and commercial use cases scale differently: Fleet owners prioritize uptime, centralized telemetry and integrable APIs; passenger-vehicle OEMs emphasize compact designs, safety certifications and user experience integration. Each requires distinct GTM motions, channel strategies and warranty structures.

Competitive landscape: a concise strategic read

The TPMS vendor set is a mix of Tier‑1 automotive systems integrators, semiconductor specialists and focused sensor manufacturers. The market is competitive but not fragmented: a group of established suppliers dominate core OEM channels while innovative entrants pursue software-driven models and aftermarket niches.

- Incumbent systems integrators (examples include major European and Japanese engineering-led firms) continue to leverage scale, OEM relationships and integrated platforms that combine sensors with control units and vehicle bus integration.

- Semiconductor and microcontroller providers are pushing differentiation via low‑power MCUs and advanced radio front-ends that enable secure wireless telemetry and edge analytics—critical enablers for next‑generation TPMS offerings.

- Software-first challengers are emerging with sensorless or software-augmented approaches that reduce hardware bill-of-materials and target aftermarket retrofit with lower service cost.

PW Consulting’s full report includes detailed vendor profiles and strategic assessments for leading players, examining capabilities such as AI-enabled fleet analytics, MEMS-based sensing, BLE connectivity, recyclable materials integration and long-life battery solutions. For executives evaluating partners or acquisition targets, the report maps capabilities to OEM and fleet buying criteria, and highlights potential white-space for fast followers.

Recent industry activity shaping 2024–2025

2024 and 2025 were active years for product introductions, capacity moves and capability expansions—signals that incumbents anticipate sustained demand and are repositioning for higher-value solutions.

- Major sensor manufacturers launched new MEMS-based TPMS units with Bluetooth Low Energy to enable direct mobile and telematics integration, reflecting industry demand for lower-power, higher-fidelity data streams.

- Some suppliers expanded production capacity in strategic low-cost locations while launching second-generation platforms focused on recyclability and modular integration for both passenger and commercial vehicles.

- Software-driven alternatives reached market maturity, offering algorithmic tire-pressure indicators that challenge traditional sensor-only value propositions—an emerging disrupter for retrofit channels.

- System integrators introduced trailer telematics packages that natively integrate TPMS data into fleet management back-ends, pointing to cross-sell opportunities for telematics providers and OEMs targeting logistics customers.

At the same time, recall events and regulatory scrutiny have kept product integrity and compliance top of mind for manufacturers and OEMs, underscoring the need for robust quality programs and compliant system design.

What PW Consulting’s TPMS report delivers — practical contents for 2026 action

We designed this study to be a working tool for strategy teams, product managers and corporate development groups. Key deliverables include:

- Market sizing and segmentation (historical and forecast), with scenario-based sensitivity to raw material costs, wireless module pricing and regulatory shifts.

- Technology roadmaps covering sensor architectures (MEMS, valve‑stem designs), wireless protocols (BLE, proprietary RF), microcontroller evolution and the emergence of software-only TPI alternatives.

- Competitive benchmark matrix: technology capabilities, production footprint, OEM relationships and aftermarket distribution reach—actionable for supplier selection and M&A screening.

- Commercial models and pricing playbooks for OEM, aftermarket and fleet channels, including recommended warranty structures and service pricing for connected TPMS offerings.

- Go-to-market templates: partnership archetypes, integration checklists for vehicle platforms and OEM procurement playbooks suitable for 2026 contract cycles.

- Regulatory and compliance tracker: timelines for key markets, interpretation of FMVSS and EU regulations, and recall risk scenarios linked to non-compliance.

To preserve the strategic advantage for subscribers, the report withholds granular regional and sub-segment revenue tables from this preview; those datasets and the full company market-share analysis are available via the PW Consulting publication portal.

Top strategic actions for 2026 (prioritized)

- Prioritize sensor-to-cloud partnerships: Lock in data ingestion and analytics partners now to accelerate commercial pilots with fleet customers in 2026.

- Invest selectively in low‑power communications and MCU platforms to extend battery life and reduce service costs—this is a differentiation lever with direct ROI in warranty and aftermarket service economics.

- Pursue modular product families: offer basic safety-compliant units and upgrade paths to connected services; this supports OEM flexibility and aftermarket monetization.

- Establish quality and recall mitigation programs: strengthen field-testing, over-the-air diagnostic capabilities and traceability to reduce recall risk and associated brand impact.

- Screen acquisition targets by capability gap: consider buying software-led TPMS challengers or semiconductor-enabled sensing startups to accelerate time-to-market for integrated solutions.

Methodology snapshot — trust but verify

PW Consulting’s market model combines bottom-up sell-in data, supplier capacity analyses and primary interviews with OEM procurement leads, telematics providers and aftermarket distributors. The forecast uses a base year of 2025 with historical calibration across 2020–2025 and scenario analysis through 2032. Revenue is expressed in USD (Million) and the forecast embeds sensitivity bands for material and logistics volatility as well as adoption curves for software-enabled services.

Conclusion and next steps

For 2026 planning cycles, TPMS is no longer simply a compliance checkbox; it is a platform for safety, operational efficiency and recurring revenue. PW Consulting’s TPMS market study equips decision-makers with the strategic context, scenarios and execution templates required to capture the upside while mitigating recall and regulatory risks.

To access the full dataset, vendor matrices and proprietary segment tables — including the granular regional and channel breakdowns that informed our recommendations — please visit the PW Consulting reports page and request the TPMS Market report package. The full report contains the actionable details you’ll need to finalize sourcing, R&D prioritization and M&A screening in 2026.

For detailed analysis of this topic, please visit the official page:Tire Pressure Monitoring System (TPMS) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com