Hydrotalcite (CAS 11097-59-9) Market: Strategic Outlook for 2026 Decision-Makers

As global manufacturers and materials strategists prepare their 2026 playbooks, the hydrotalcite market has entered a distinct phase of maturation and selective expansion. PW Consulting’s latest market study — anchored on historical performance through 2025 and forward-looking projections to 2032 — provides the precise, operational intelligence that procurement, R&D, and corporate development teams need to convert market signals into defensible strategy.

Hydrotalcite (CAS 11097-59-9) Market

Why this report matters for 2026 strategies

- Macro momentum is clear: Total global revenues for hydrotalcite grew from USD 139.86 million in 2020 to USD 185.24 million in 2025, and our modeling shows a continued rise to USD 273.72 million by 2032 — an implied compound annual growth rate of 5.8% across the forecast horizon. These figures evidence steady demand expansion rather than speculative spikes, which changes the nature of strategic choices available to incumbents and new entrants alike.

- Concentration provides both stability and opportunity: Industry concentration metrics (CR3 ~35%, CR5 ~50%) indicate a market where a small set of suppliers hold meaningful share but significant volume remains accessible to agile competitors. That structural profile favors targeted investments — capacity additions, differentiated grades, or downstream partnerships — over broad, capital-intensive horizontal expansion.

- Regulatory and technical tailwinds are reshaping demand composition: Evolving REACH standards in the EU and updated FDA excipient guidance in the U.S. are raising the bar on purity and traceability. Meanwhile, environmental policy and customer sustainability commitments are accelerating substitution toward non-toxic, heavy‑metal-free stabilizers. For 2026, these dynamics make regulatory readiness and documented supply-chain integrity commercial differentiators.

Data-driven signals every executive should prioritize

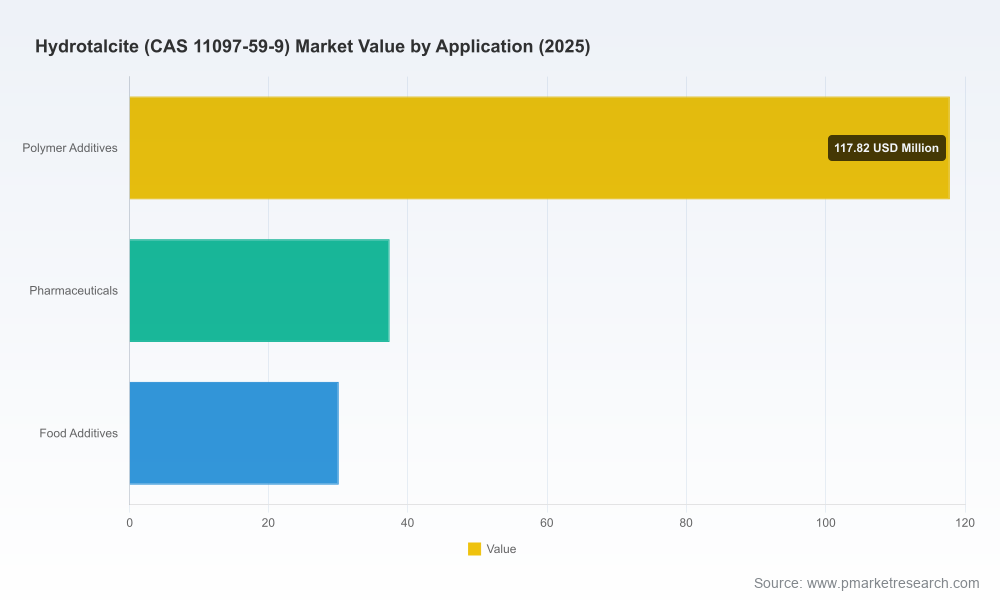

- Demand durability in polymer additives and pharmaceuticals: Our historical-to-forecast series shows consistent uptake across core applications. Buyers of hydrotalcite are increasingly segmenting requirements by technical specification (e.g., thermal stability, halogen scavenging, pharmaceutical-grade purity), which increases average selling prices for premium grades even as large-volume stabilizer demand remains the base growth engine.

- Price and margin sensitivity to grade complexity: Advanced nano- and surface-treated hydrotalcite deliver performance benefits but carry higher raw-material and processing costs. Adoption in price-sensitive territories lags, so suppliers that can engineer cost-to-performance advantages will win the mid-market. Procurement teams should therefore develop multi-tier sourcing strategies to capture upside without overpaying for premium attributes where they are not required.

- Capacity shifts are signaling strategic plays: Recent capacity expansions by major producers are not random supply increases; they represent commitments to serve electrification (EV wiring and insulation), automotive interior materials, and pharmaceutical excipient markets. Corporates negotiating long-term supply in 2026 should map these capacity moves to their application roadmaps and lock in clauses that reflect evolving purity and lead-time requirements.

What the PW Consulting report delivers (practical chapter highlights)

Our study is designed as a decision-support toolkit for commercial, technical, and corporate strategy teams. Highlights include:

Hydrotalcite (CAS 11097-59-9) Market

- Market sizing and rigorous methodology notes — transparent assumptions, scenario variants, and sensitivity analysis tailored to raw-material price and regulatory shocks.

- Supply-side diagnostics — plant-by-plant capacity trends, recent capital projects, and utilization profiles that expose short-to-medium-term supply tightness and where pricing pressure may emerge.

- Application intelligence — performance requirements mapped to grade families, substitution risk matrices, and specification checklists for procurement and quality teams.

- Regulatory and compliance playbook — compliance gap assessment (REACH, FDA excipient guidelines), documentation templates, and recommended certification roadmaps to accelerate market entry for certified grades.

- Commercial playbooks — go-to-market options (direct sales vs. distributor-led), recommended commercial terms for 12–36 month supply contracts, and a supplier scorecard for strategic sourcing.

- M&A and partnership screening — valuation markers, strategic fit criteria, and integration risk checklists for bolt-on acquisitions or JV structures focused on capacity, geography, or specialty grades.

- Technology and product roadmap — R&D focus areas with highest commercial leverage (surface modification, dispersion technologies, and pharmaceutical-grade synthesis) and an R&D investment prioritization model.

To respect the “trailer” principle of this release, we intentionally limit disclosure of granular regional and application-level shares here; the full report contains the complete segmentation matrices and proprietary concentration overlays used to generate our recommendations.

Hydrotalcite (CAS 11097-59-9) Market

Competitive landscape — who matters and why

The hydrotalcite market blends legacy producers with regional champions and specialty chemical multinational initiatives. Our competitor profiling focuses on strategic posture, capability differentiators, and recent moves that change supplier economics.

- Kyowa Chemical Industry Co., Ltd. (Japan) — An industrial pioneer with a well-established synthetic hydrotalcite portfolio. Kyowa’s DHT series and investments in European capacity signal a dual strategy: protect core PVC stabilizer franchises while growing medical- and specialty-grade volumes. Their focus on high-purity grades positions them well for customers who require certified excipient suppliers.

- Sakai Chemical Industry Co., Ltd. (Japan) — A specialist in heat-stabilizing grades optimized for thermal performance and color retention. Recent capacity enhancements target flame-retardant applications in EV wire insulation, suggesting Sakai is aligning with electrification-driven materials demand.

- Clariant AG (Switzerland) — Leveraging scale and regulatory expertise to promote heavy-metal-free formulations across automotive and cable markets. Clariant’s new European capacity and recent high-purity grade launch underscore a strategy of combining product innovation with regional manufacturing proximity.

- SINWON CHEMICAL (South Korea) and Doobon Inc. (Korea) — Focused on non-toxic stabilizers and surface-modified grades, emphasizing dispersion performance in filled polyolefin systems. Their product breadth makes them important partners for compounds and masterbatch producers.

- GCH TECHNOLOGY (China) and Heubach India — Regional leaders that combine cost-competitive manufacturing with strong downstream relationships in cable and PVC masterbatch markets. Their presence guarantees supply diversity for global buyers and creates competitive pricing pressure in volume segments.

- Sasol Germany GmbH — Brings a differentiated sol‑gel manufacturing route with tunable Mg/Al ratios, opening adjacent chemical applications in catalysis and alkaline processes.

These profiles are augmented in the full PW Consulting package by supplier scorecards, commercial benchmark tables, and contract negotiation playbooks.

Recent industry developments that will shape 2026

- Capacity investments by European and Japanese players in 2025 — notably new production lines and unit commissioning — have altered the near-term supply map and reduced spot-market volatility for certified grades.

- Product launches aimed at pharmaceutical excipients and high-purity antacid grades reflect a strategic pivot by some incumbents toward specialty, higher-margin segments.

- Regulatory tightening and customer sustainability programs have pushed roughly two-thirds of industrial adoption toward eco-conscious formulations, creating a premium window for compliant suppliers.

Strategic plays for corporates and investors in 2026

Our strategic recommendations are organized by time horizon and function:

- Short-term (0–12 months)

- Secure multi-year supply agreements with clause structures that address purity upgrades and traceability requirements to mitigate regulatory risk.

- Prioritize partners with local or regional capacity if your application requires certified grades with low lead-time risk.

- Implement a two-tier sourcing framework: certified high-purity suppliers for regulated applications and cost-effective producers for commodity stabilization needs.

- Medium-term (12–36 months)

- Consider targeted JVs or minority investments in specialty-grade capacity to secure margins and co-develop next-gen surface-treated products.

- Invest in application-specific testing (dispersion, thermal aging, halogen capture) to validate substitutes and reduce reliance on legacy formulations.

- Build regulatory dossiers proactively — REACH pre-registration or FDA excipient master files — to expedite market access for premium grades.

- Long-term (36+ months)

- Assess full vertical integration only when capture of downstream value is demonstrable; otherwise pursue strategic partnerships to balance capital exposure and market access.

- Monitor technological convergence with nano-additives and synergistic stabilizers; be prepared to pivot R&D investment as performance thresholds evolve.

How PW Consulting supports your 2026 decisions

We built this report to be immediately operational: from actionable procurement clauses and supplier scorecards to an M&A screening model that flags targets by strategic fit rather than headline valuation. For strategy teams facing constrained capital or aggressive sustainability targets, the analysis identifies where to concentrate scarce resources for the highest return on investment.

For executives preparing budgets and roadmaps for 2026, the core takeaways are unambiguous: hydrotalcite is a steadily growing specialty-chemicals market (USD 139.86 million in 2020 → USD 185.24 million in 2025 → USD 273.72 million by 2032, CAGR 5.8%), regulatory and product-differentiation forces will determine who captures premium value, and selective, capability-driven investment will outperform broadscale capacity bets.

Next step

The summary above is designed to demonstrate the depth and utility of the full PW Consulting study while preserving proprietary segmentation insights that underpin tactical recommendations. Access to the complete report provides the detailed regional and application matrices, supplier benchmarking datasets, and executable playbooks you need to operationalize 2026 strategy. Contact PW Consulting to request the full intelligence package and arrange a briefing tailored to your company’s risk profile and strategic priorities.

For detailed analysis of this topic, please visit the official page:Hydrotalcite (CAS 11097-59-9) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com