Why Is the U.S. Algae-Based Aquafeed Market Growing in Sustainable Aquaculture?

Networking |

2026-05-07 07:53:05

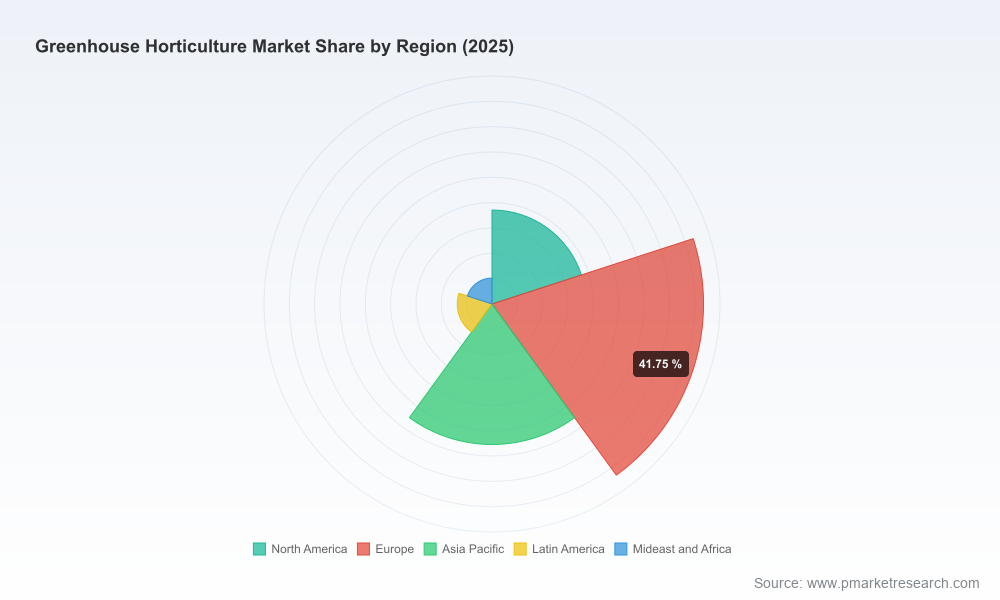

PW Consulting’s newest market study — Greenhouse Horticulture Market (base year 2025, forecast 2026–2032) — translates rising demand dynamics, technology inflection points, and evolving regulatory pressure into actionable strategic guidance for executives planning capital allocation, partnerships, and product roadmaps in 2026. The global market is expanding at a compound annual growth rate (CAGR) of 7.9% through the forecast window. After a period of steady expansion from 2020 to 2025, our model projects sustained growth through 2032, underscoring a multi-year investment horizon for hardware suppliers, automation vendors, and vertically integrated growers.

Greenhouse Horticulture Market

Policy and standards are converging on energy use and emissions metrics. Public comment processes and national pilots launched over 2024–2025 mean that 2026 will be the year many growers and vendors either adapt or face a more constrained operating environment. Early movers who align operations and product specifications with the forthcoming metrics will gain cost and compliance advantages.

Greenhouse Horticulture Market

Technology validation is accelerating. Recent field trials and product innovations — from dynamic LED lighting experiments to new software that quantifies photosynthetically active radiation — are moving from demonstration to commercial pilots. These developments compress the time to ROI for systems investments and change procurement risk profiles for growers and integrators.

Greenhouse Horticulture Market

Market structure is maturing. Market concentration metrics show a mid-level consolidation: a handful of global suppliers capture a significant share of industry revenue while numerous regional specialists maintain local competitive advantages. This structure favors both strategic partnerships and selective M&A to secure distribution and capability footprints.

CapEx prioritization: With a clear market growth trajectory and demonstrable improvements in yield-per-square-meter from automation and precision systems, capital deployment should shift toward systems that shorten payback periods under the new regulatory baselines. That means favoring modular, upgradeable installations and performance-linked contracts.

Product and service bundling: Buyers increasingly seek integrated solutions that de-risk energy and crop outcomes. Vendors who can combine physical infrastructure with software-driven control and financing options will create higher switching costs and capture larger lifetime value.

M&A and partnerships: For mid-size suppliers, alliance strategies that combine engineering, local installation capacity, and digital platforms will beat organic growth in speed and scale. For corporate buyers, bolt-on acquisitions that expand automation, irrigation, or lighting portfolios are the fastest route to meet new performance standards and customer expectations.

Geographic go-to-market choices: Though growth is broad-based, winners will be those who tailor offerings to local regulatory regimes, power cost realities, and crop mixes. Local partnerships and pilot projects are preferred to large-scale rollouts until regulatory baselines stabilize.

Our competitive assessment layers firm capabilities, global reach, and product differentiation to highlight strategic opportunities and risks. Several established players stand out as ecosystem anchors:

Texas Greenhouse Company Inc. (Fort Worth, TX) — a legacy manufacturer with deep roots in both residential and commercial greenhouse structures. Their long-standing brand recognition and installation experience make them an attractive partner for projects that require proven, customizable structures and after-sales support.

Certhon (Poeldijk, Netherlands) — a leader in large-scale, high-tech turnkey greenhouses. Their strength lies in systems integration for commercial-scale growers aiming to maximize throughput under controlled conditions; they are a natural counterparty for institutional farms and export-oriented growers.

Gakon Netafim (Israel, global operations) — a recognized name for precision irrigation and controlled-environment technologies. Their irrigation and fertigation competence remains a critical lever for yield optimization and resource efficiency, and it pairs effectively with automation platforms.

Stuppy Greenhouse (Missouri, USA) — a commercial-structure specialist with emphasis on rugged, high-quality builds for professional growers. Their regional installation network and project management skills reduce implementation risk for scale-up projects.

Hoogendoorn (Vlaardingen, Netherlands) — focused on horticultural automation and intelligent control systems. As software and sensor stacks become central to meeting new energy and emissions metrics, firms like Hoogendoorn that offer closed-loop control will find growing demand.

Richel Group (France, global) — known for design, manufacturing, and turnkey project delivery. Their end-to-end capability makes them a preferred integrator for projects where a single accountable supplier reduces delivery complexity.

Haygrove Limited (UK) — specialist in polytunnels and greenhouse systems for berry and soft fruit producers. Their crop-specific know-how and modular systems are well-suited to growers seeking rapid deployment and flexible crop rotation options.

Collectively, the industry’s top three to five suppliers account for a sizeable share of revenue, but remaining market share is distributed among regional specialists and technology-focused entrants. This balance creates opportunity for both consolidation and niche differentiation.

Product and platform launches continue to shift the competitive set toward software-enabled solutions; one vendor released a light-management analytics tool this year that promises to help growers optimize light budgets in real time.

Recognition of innovation via industry awards and demonstrations highlights where investor and buyer interest is concentrating — particularly around material handling and propagation trays that improve labor productivity and automation compatibility.

Field trials between research institutions and major lighting vendors are validating year-round production models for higher-value crops under dynamic lighting regimes, reducing seasonal revenue variability for adopters.

Three regulatory developments warrant explicit scenario planning in 2026:

Energy and greenhouse gas metric revisions under public consultation are likely to alter allowable energy use baselines and reporting requirements. Companies must model cost-to-comply scenarios and the potential for incentivized upgrades.

Regulated demonstration trials of biological and crop-protection innovations create both risk and opportunity — early engagement in trials can accelerate approval pathways but requires risk-managed investment strategies.

Calls for rule changes to reduce the cost of organic greenhouse produce indicate potential market segmentation shifts — producers and suppliers should model premium vs. cost-competitive channels under alternative regulatory outcomes.

This study is structured to support executable decisions in 2026. Deliverables include:

Scenario-based financial models that translate regulatory and technology adoption pathways into P&L and cash-flow outcomes for growers and suppliers.

An M&A and partnership radar highlighting strategic targets by capability and geography, plus integration playbooks for accelerating time-to-value from acquisitions.

Supplier and technology maps that cross-reference capability (e.g., automation, irrigation, lighting) against implementation risk and typical deployment timelines.

Operational checklists and procurement specifications to standardize tenders, tighten warranties, and implement performance-linked contracts.

Regulatory impact matrices that quantify cost and compliance pathways under alternative policy scenarios.

Executive dashboards that synthesize the report’s quantitative backbone (market growth trajectory, concentration metrics) into decision-ready KPIs for board-level review.

PW Consulting combines primary interviews with growers, integrators, and policy stakeholders, a bottom-up sizing of installed base and equipment replacement cycles, and scenario-driven forecasting to produce a defensible market view. The report integrates a historic series through 2025 and projects through 2032 using a 7.9% CAGR under our central case. Concentration indicators are included to help bidders and strategists assess competitive intensity and bargaining dynamics.

CEOs and CFOs: Use the financial scenario suite to stress-test investment proposals and to structure performance-linked financing that transfers adoption risk to vendors.

Business development and M&A teams: Employ the supplier maps and acquisition radar to prioritize targets that expand technology stacks or geographic coverage in line with projected demand corridors.

Product and R&D leaders: Align roadmaps to the technology maturity curves in the report — prioritize upgrades that reduce energy intensity and simplify compliance reporting.

Policy and sustainability teams: Leverage the regulatory matrices to model future compliance costs and to design advocacy strategies or pilot partnerships that shape implementation timelines.

This release is intentionally a strategic “trailer”: it demonstrates the depth, structure, and immediate applicability of PW Consulting’s Greenhouse Horticulture Market study while preserving the report’s detailed segment-level data and proprietary models for subscribers. If your organization faces capital allocation, M&A, product roadmap, or regulatory-compliance choices in 2026, this report converts high-level market momentum into executable next steps — with tools, templates, and a prioritized action plan you can implement this year.

To access the full dataset, regional and crop-level segmentation, detailed supplier profiles, and downloadable decision-support models, please visit the PW Consulting report page for the Greenhouse Horticulture Market. Our team is also available for tailored briefings and custom scenario workshops to ensure your 2026 strategy is both resilient and opportunistic.

For detailed analysis of this topic, please visit the official page:Greenhouse Horticulture Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com